Overseas

June 26, 2022

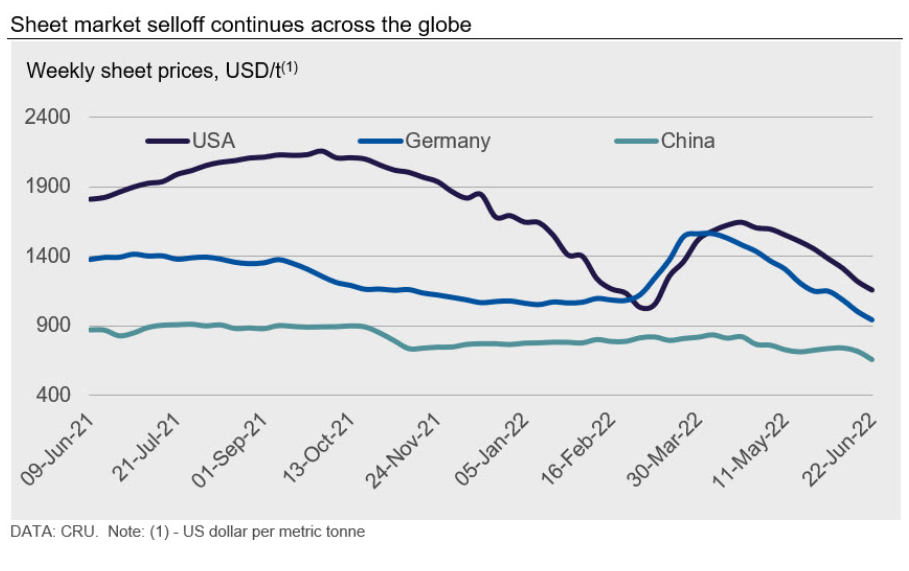

CRU: Sheet Prices Around the World Continue to Plummet

Written by Ryan McKinley

By CRU Senior Analyst Ryan McKinley, from CRU’s Steel Sheet Products Monitor

Prices for sheet products continued to fall rapidly around the globe this week. Mills in the US have become increasingly aggressive with their offers and are shifting their focus towards value-added products in order to obtain higher margins over costs. As a result, CR coil prices dropped substantially this week.

European producers are beginning to take down furnaces for maintenance as prices there continue to fall, although this drop in supply has not provided much upside support to prices in the region. In Asia, a selloff in the iron ore and steel futures markets resulted in yet more bearish market sentiment, and the few transactions that occurred in the region were at a substantial discount to prior weeks.

US

In the US, CR coil prices fell by $127 per short ton week-on-week (WoW), or a drop of 7.8%. Speculation among buyers is that mills are moving more material downstream to their value-add products in an attempt to maximize profitability on fewer tons and limit price erosion.

HR coil and HDG coil prices also decreased this week by $56 per short ton and $55 per short ton, respectively. Buyers reported they have seen an increase in communication with mill representatives, some of whom they have not spoken with since 2021. Rising costs are resulting in less disposable income for consumers, and they have begun focusing their purchases on food, fuel, and wellness products and less on steel-intensive goods.

Prices were unchanged on the US West Coast this week, but buyers reported seeing an increase in import offers with prices well below those currently being offered by domestic mills. While buyers are still dealing with ocean freight and port congestion issues, they are not enough of a problem to force buyers to give up on all foreign offers. Demand on the West Coast remains steady, although some companies have reported a slight softening in demand due to delays in supplies.

Europe

European sheet prices have fallen by €29–66 per ton WoW across both Germany and Italy as spot activity remains scarce. Stock levels in northern Europe are relatively full across the board, hence buyers continue to refrain from purchasing significant volumes. Many market participants still expect further room for prices to go down given slow demand from end-use sectors. European mills are actively engaging with buyers to generate orders, suggesting that we are still in a buyers’ market. In our latest assessment, German and Italian HR coil were assessed at €894 per ton and €872 per ton, respectively.

ArcelorMittal has announced that they will be idling a small BF at their Dunkirk facility in France because of the rapidly falling prices in Europe. One of their smaller blast furnaces at Eisenhuttenstadt has also been idled. Despite this cut capacity, we anticipate that spot prices will keep moving lower in the coming month or two.

China

Chinese domestic sheet prices plummeted after bearish sentiment dominated the market this week. Transaction volumes were minimal as participants waited on the sidelines. After bottoming in April and rising month-on-month (MoM) in May, the latest manufacturing sector statistics do not show any year-on-year (YoY) growth. In addition, market confidence is hampered by the prolonged lockdowns and weather conditions in China.

Market participants expect that the scorching weather in the north and heavy rainfalls in the south will disrupt the normal pace of recovery in both demand and logistics. Meanwhile, despite a MoM recovery in May, auto sales and the expected increase from June thanks to the 50% purchase tax cut policy, sentiment remains cautious regarding short-term sheet demand given the currently high level of car inventories.

HR coil profitability remains in negative territory at -2.7% EBITDA, which has forced some mills to carry out maintenance in an effort to prevent further price falls. Although demand is entering a seasonal lull, these expected outages will at least provide some upside prices. Views in the market are mixed, but we expect sheet prices to remain weak in the upcoming week before any significant uptick in buying activities emerges.

Asia

Prices of imported sheet products in Asia fell sharply this week in tandem with Chinese steel prices. On Monday, the Chinese steel futures market crashed after iron ore price fell by 10%. As the result, market sentiment has become even more bearish across Asia.

Formosa Ha Tinh has lowered its offers by $30 per ton to $720-725 per ton CFR Vietnam, but this is still higher than current offers received from overseas mills. A Taiwanese mill was offered rerolling grade HR coil at $710 per ton CFR Vietnam. While Chinese and Indian mills did not formalize offers, the considered selling at $700-710 per ton CFR Vietnam.

CRU assessed HR coil prices at $700 per ton CFR Far East Asia, a $40 per ton fall WoW. CR coil prices were assessed at $920 per ton CFR Far East Asia, while HDG prices were assessed at $940 per ton CFR Far East Asia, both down by $50 per ton WoW.

India

Indian sheet prices have fallen by another INR2500–4000 ($32–51) per ton WoW. Steelmakers are capitulating to lower bids by buyers due to a lack of export opportunities and rising inventory levels while sentiment continues to remain bearish due to declining Asian prices.

The latest Indian domestic HR coil price is the lowest price assessed since April 2021, as the export duty imposition coupled with Asian demand weakness has caused a freefall in sheet prices.

CRU understands that mills are currently negotiating contracts with automakers, but a sharp bid-offer mismatch is delaying these talks. Also, a switch back to quarterly contracts (from the current bi-annual contracts) is under review given the sharp volatility in steel prices.

On the export front, Indian steelmakers have been offering HR coil (boron added, to bypass the export tax) to the GCC and Southeast Asian markets for the last two weeks, but buying interest remains limited. Pipe makers in these regions find boron-added steel incompatible with their requirements, while offers from Turkey and China for non-alloyed HR coil are quite attractive. Meanwhile, European buying interest towards Indian origin sheet has weakened for their being ample stock with key buyers.

Given the continued weakness in the export market, there is a likelihood that Indian mills will undergo extended production cuts during Q3 to manage inventory, which may provide some support to prices.

This article was originally published on June 22 by CRU, SMU’s parent company.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com