Overseas

July 17, 2022

CRU: High Inventories and Output Cuts Undermine Metallics Prices

Written by CRU Americas

By CRU Senior Analyst Puneet Paliwal, from CRU’s Steel Metallics Monitor on July 14

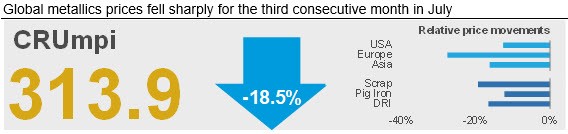

The CRU metallics price indicator (CRUmpi) registered its third consecutive double-digit percentage decline in July, falling by 18.5% month over month (MoM) to 313.9, its lowest value since February 2021.

Bearish sentiment in the metallics market, prevalent since May, has been exacerbated by rising inflation. It has also been hurt by weakening steel demand, prices, margins, and resultant steel production cuts across major economies.

Key buyers continue to report sufficiently stocked inventories, while demand destruction continues unabated in finished steel markets, forcing steelmakers to curtail BOF-based steel output alongside that of EAFs.

Making matters worse is the steady inflow of heavily discounted Russian offers for semi-finished steel and pig iron to the market, which have consistently pulled down the price floor.

Moreover, the support to prices that was anticipated by China easing pandemic controls has not materialized. And underlying demand recovery remains far below market expectation. Downward pressure is expected to remain on metallics prices until at least the end of summer. But the recent rebound in Turkish scrap prices has some suppliers saying the current price is the bottom.

Moreover, the support to prices that was anticipated by China easing pandemic controls has not materialized. And underlying demand recovery remains far below market expectation. Downward pressure is expected to remain on metallics prices until at least the end of summer. But the recent rebound in Turkish scrap prices has some suppliers saying the current price is the bottom.

Finally, in the ore-based metallics market, the ongoing war in Ukraine, rising inflation, high interest rates, and resultant lower steel demand and production cuts have caused purchases to plunge and prices to plummet. A strong divergence is being observed in pig iron prices across key regions for various reasons. For instance, Brazilian suppliers are offering pig iron to the US market at $600–620 per metric ton CFR NOLA, while the Italian import price has dropped by $80 per metric ton MoM to $480 per metric ton CFR.

In the meantime, Russian suppliers are offering pig iron to Chinese buyers (their major outlet amid western sanctions) at $375 per metric ton FOB Black Sea, which is the most competitive price offer anywhere in the world. Indian suppliers, who had turned active exporters when pig iron prices skyrocketed just after the war broke out, are now on the sidelines because global prices have crashed. Also, the Indian government has imposed a 15% export tax on pig iron that started on May 22.

An exception to all the doom and gloom in the global metallics market is the Turkish market, where scrap import prices have jumped by $85 per metric ton over the last couple of weeks to reach $406 per metric ton CFR for HMS 80:20. This upswing seems unsustainable. But it has brought in some optimism among scrap suppliers in the US and Europe. They now think the price bottom may be near. Following this scrap price upswing, pig iron export prices to Turkey have to jumped to $480 per metric ton CFR, up $95 per metric ton compared to end of June. And the increase has come despite low buying activity.

Outlook: Prices Likely to Revive at Summer’s End

We expect the downtrend in scrap prices to continue in the US and in Europe over the next couple of months, though the pace of decline will slow. These markets are sufficiently stocked at a time when steelmakers are undertaking maintenance outages and curtailing output in response to sharp declines in steel prices. Thus, underlying demand for metallics should remain on a weak footing. Moreover, the next few months are considered seasonally strong for scrap generation and collection, which is likely to add to the oversupply pressure unless recyclers decide to curtail operations to support prices.

While trying to adjust output, scrap suppliers in these regions are also likely to allocate higher volumes to exports, the prices of which will be determined by underlying demand in key importing regions within Asia – most of which have entered a seasonally weak period for construction steel demand due to the onset of the rainy season.

Meanwhile, global demand and prices for ore-based metallics (particularly pig iron) is likely to remain subdued over the next month, with Russia continuing to flood the market with low-priced material.

CRU thinks near term trends in metallics prices will be largely dictated by the direction of steel prices. Steel prices will be influenced by the extent of the mismatch between supply and demand following output cuts and the gradual reduction of inventories across the steel supply chain. We continue to forecast risks to prices tend to the downside, at least in the very short term.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com