Prices

July 28, 2022

Ferrous Futures: Treading Water This Summer

Written by Jack Marshall

The following article on the hot-rolled coil (HRC), scrap and financial futures markets was written by Jack Marshall of Crunch Risk LLC. Here is how Jack saw trading over the past week:

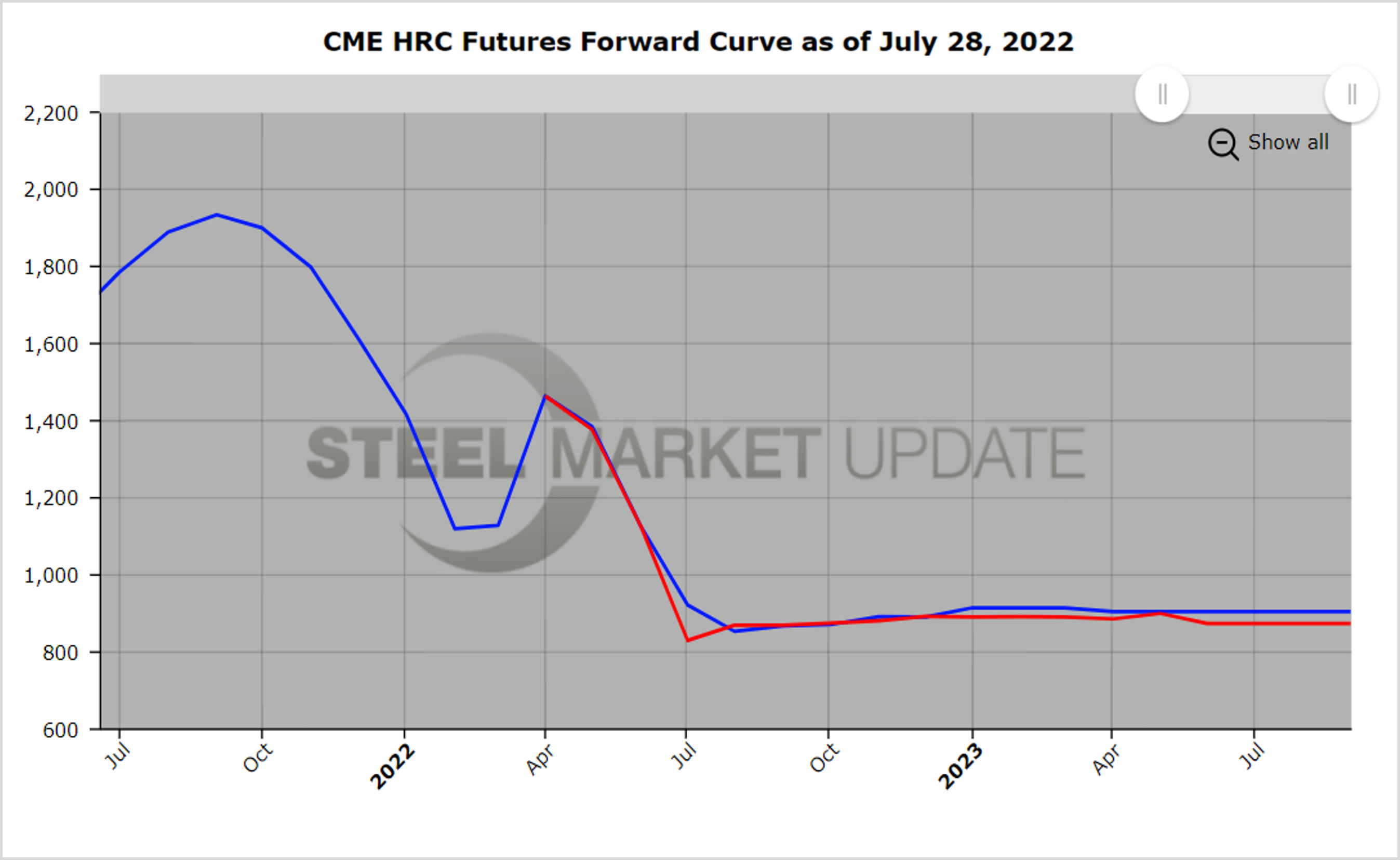

Hot Rolled

The HR futures market has been somewhat subdued this month, which is reflected in the price changes for July.

Over the last four Wednesdays, spot has declined $127 per short ton—from $988/ton to $861/ton—to settle at an average of $922/ton.

Continued inflation concerns and another 75-basis-point hike by the Federal Reserve have weighed on activity.

Meanwhile, the futures curve has changed little this month, with the latter half months of 2022 down roughly $25/ton to an $870/ton average.

Q1’23 is basically unchanged at $895/ton, and the latter part of the futures curve is up roughly $25/ton.

The bulk of trading has been in 2022 months. But there has been a small pickup in Cal’23 periods this week. That could be signaling a change as folks look to hedge out further interests.

Also, a few Q4’22 HR call options have traded recently with strikes in the low $900/ton range.

Open interest, which closed out June just shy of 30,000 lots, currently sits at 27,300 lots—reflecting the quieter markets.

Trading volumes are running at an average volume of 15,000/ton per day this month, which has 18 trading days.

Below is a graph showing the history of the CME Group hot rolled futures forward curve. You will need to view the graph on our website to use its interactive features. You can do so by clicking here. If you need assistance with either logging in or navigating the website, please contact us at info@SteelMarketUpdate.com.

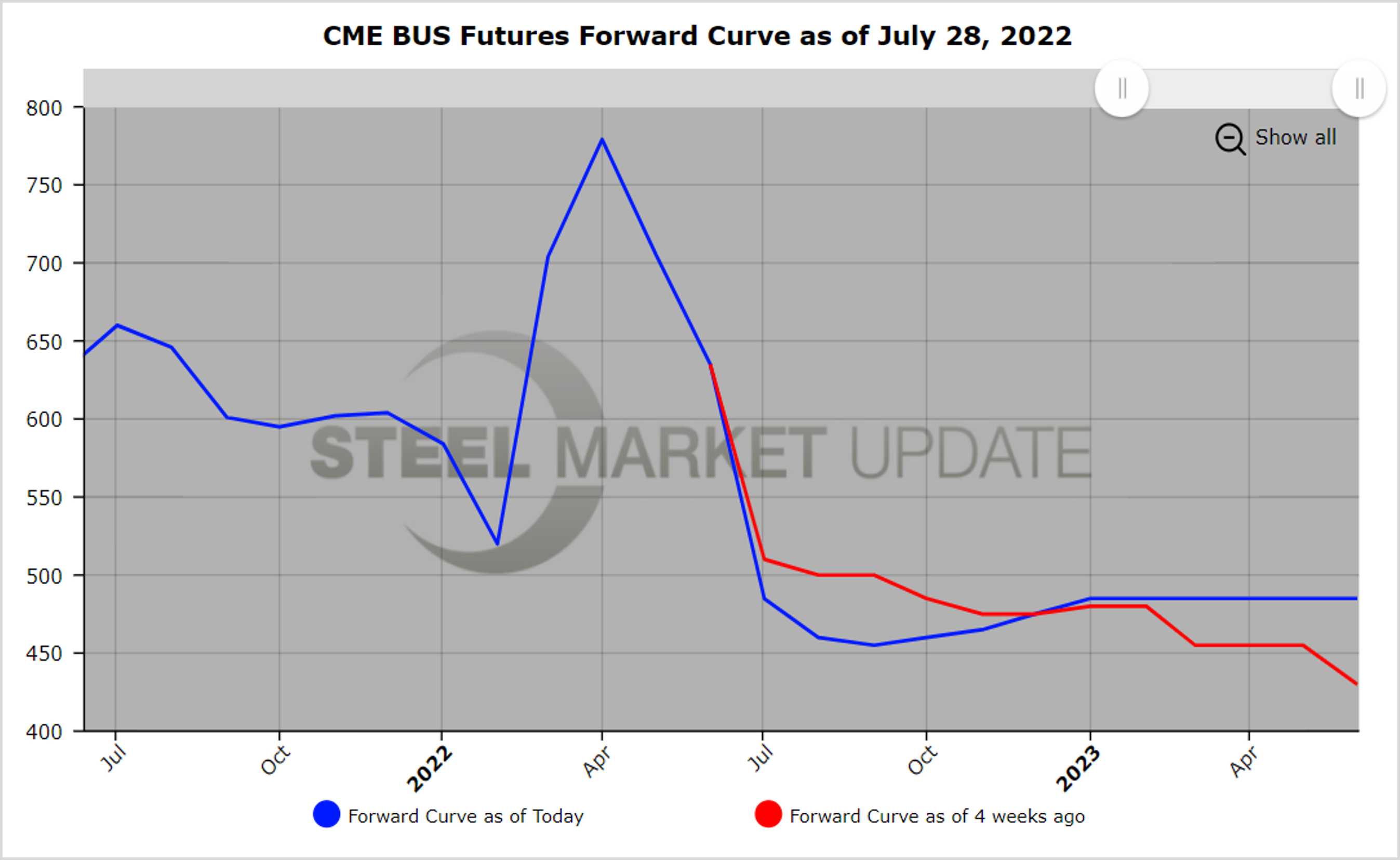

Scrap

BUS declined from $635 per gross ton in Jun’22 to $501/gross ton for the Jul’22 settlement. It has continued to show some further weakness this month, with Aug’22 futures trading as low as $460/gross ton after sitting at $475/ton for a few weeks.

Since the end of June, the latter half of 2022 average settlement price has declined from $495/gross ton to roughly $470/gross ton currently. With prices under $500/gross ton, we are starting to see more BUS inquiries.

Below is another graph showing the history of the CME Group busheling scrap futures forward curve. You will need to view the graph on our website to use its interactive features. You can do so by clicking here.

By Jack Marshall of Crunch Risk LLC