Market Data

April 13, 2023

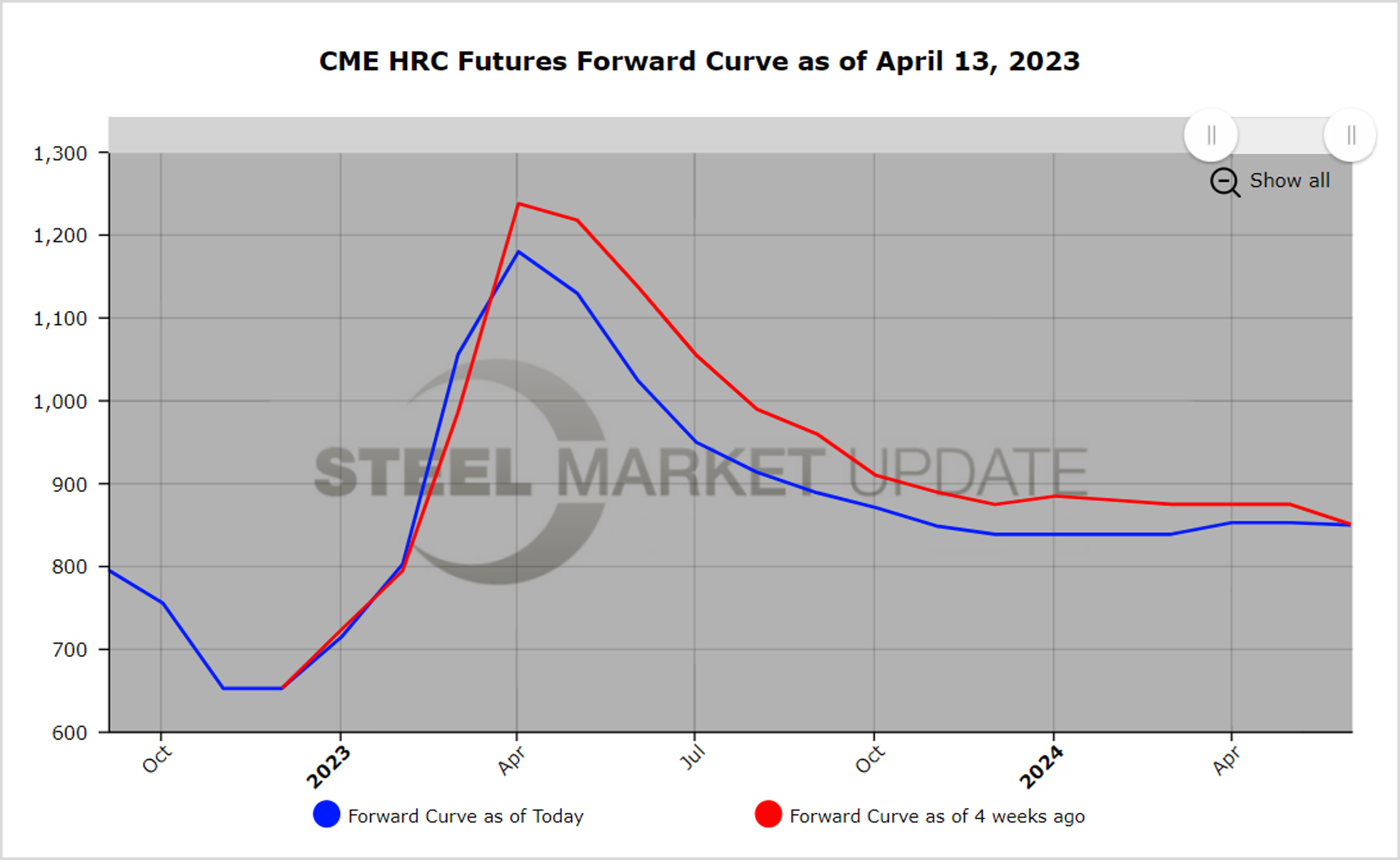

HR Futures April Surprise

Written by Jack Marshall

Surprise! Instead of $10-$20 per-short-ton (ST) increase expected by most the index for the CME HR jumped $50/ST this week. This caught many by surprise as recent futures activity seemed to reflect a more bearish sentiment. It appears small retail truckload transactions from the mills carried the day. Wednesday HR futures volume was healthy as the near months ticked higher on some short covering. The front month future bounced about $20/ST from the mid $1,165/ST settlement price. Meanwhile, open interest in HR futures has risen about 1,000 lots since the March futures contract rolled off, which is a touch softer than the market finished the end of March.

We could have a spell of lighter activity as participants look for further signs the HR market will either continue to inch higher or maintain current levels. Recent liquidity issues with banks will likely suppress activity as participants keep inventories tight due to concerns of tightening liquidity from their banks.

The latest US and Chinese economic data do not paint a very robust demand picture going into the heart of 2023. However, the HR index could linger at these elevated levels for longer than the market participants expect as the HR index tends to lag market expectations.

In addition, lack of physical spot trades will lead to more reliance on small retail transactions, which are typically higher. The higher index (over $1,200/ST) has helped move settlement prices for the HR May’23 to HR Sep’23 futures up by about $16/ST on average since the beginning of April ($982/ST average price). HR Oct’23 futures through Jan’24 futures have stayed unchanged, while the Feb’24 through Apr’24 futures have risen over $35/ST.

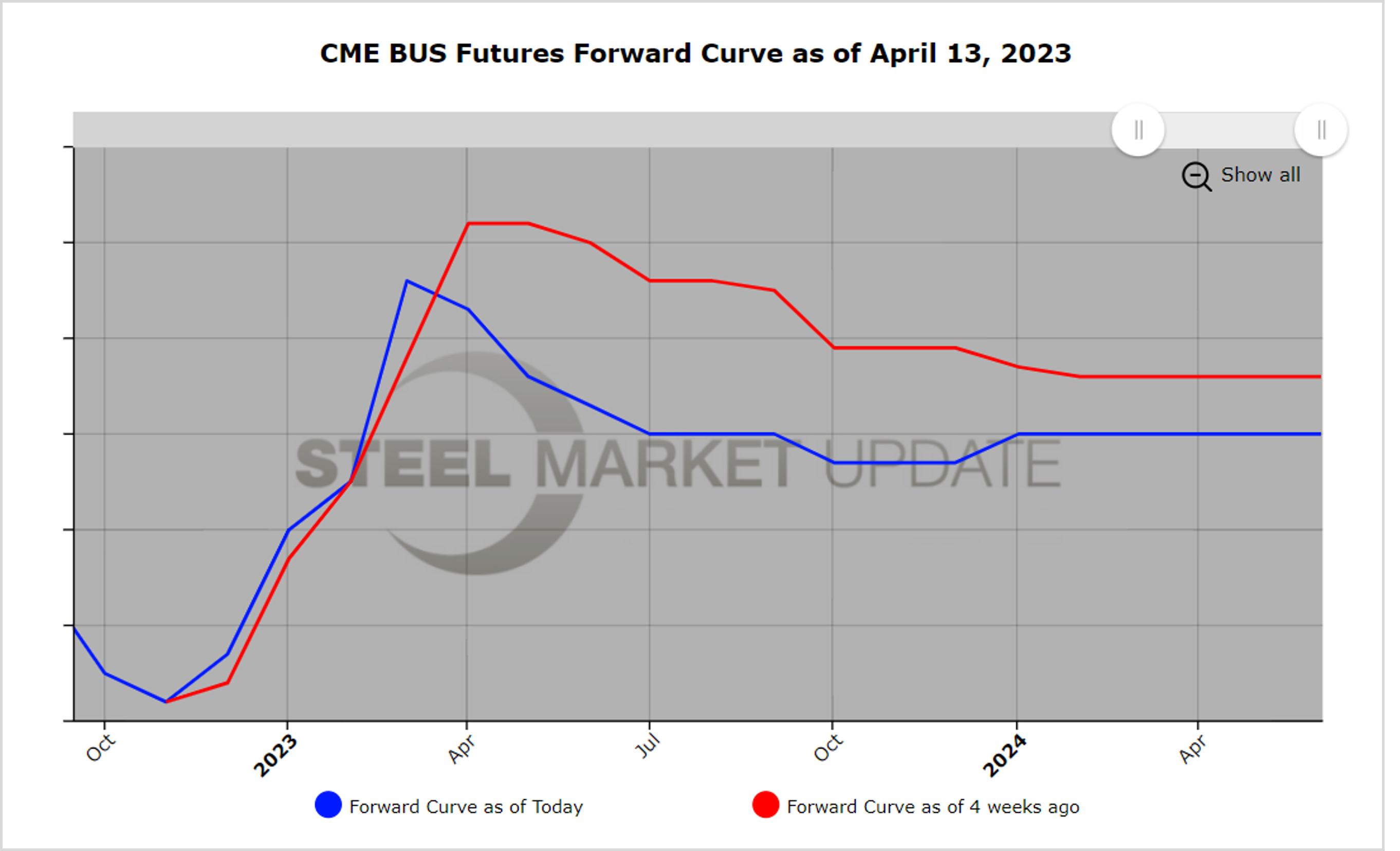

April BUS futures settled at approximately $566/GT, up roughly $10/GT from the Mar’23 settlement. Futures activity has been very muted the last few weeks as the market was expecting a strong sideways settlement for April. Since the beginning of April, the May and June BUS futures have lost about $15/GT on average in settlement value.

With the April settlement in the rearview mirror, we could start to see a further drop in BUS prices. Weak demand from China and Turkey, in addition to lower capacity utilization rates domestically, have the potential to translate to softer price levels. Any improvement in obsolete scrap collections as we roll slowly out of winter weather could also help ease BUS prices.

Note in the last two weeks the metal margin (HR minus BUS) has widened for the futures months May’23 through Dec’23 on average about $21/ton.

Editor’s note: Want to learn more about steel futures? Registration is open for SMU’s Introduction to Steel Hedging: Managing Price Risk Workshop. It will be held on April 26 in Chicago. Learn more and register here.

By Jack Marshall of Crunch Risk LLC