Prices

January 16, 2025

HR vs. galvanized price spread shrinks to 18-month low

Written by Brett Linton

The price premium of galvanized coil over hot-rolled (HR) coil has continued to narrow, a trend seen for the past seven months. As of this week, the spread between these two products has reached an 18-month low.

Recent trends

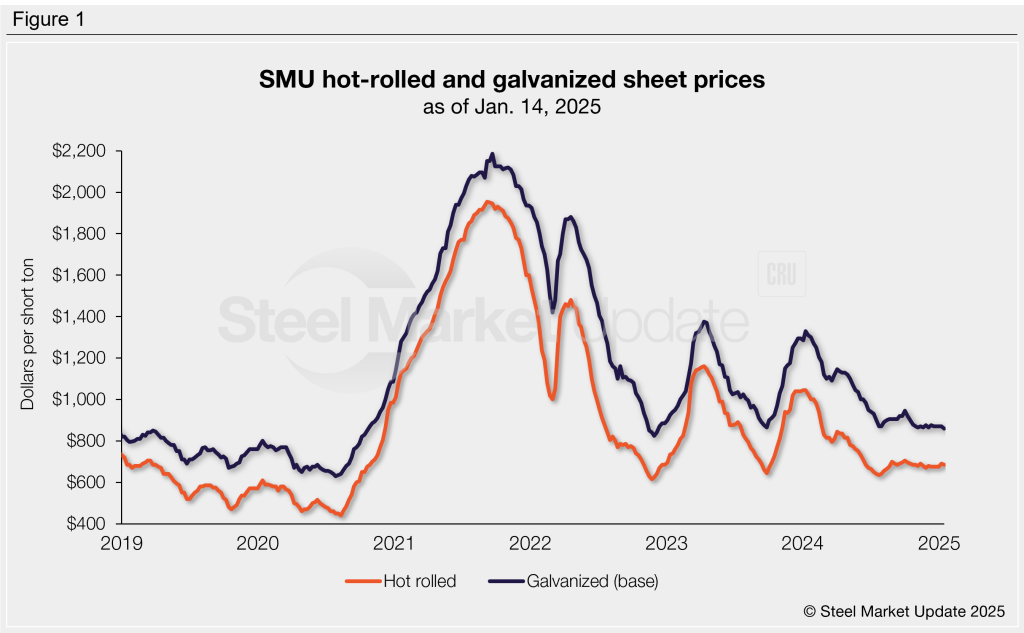

SMU’s average hot-rolled coil price decreased $5 per short ton (st) this week to $685/st. Prices have remained relatively stable over the past three months, fluctuating within a tight range of $670-690/st. HR prices remain marginally higher than the 19-month low seen last July ($635/st).

Our galvanized index also eased this week, declining $10/st week over week (w/w) to a two-year low of $860/st. Note that this is our base price without any additional mill extras. This is the lowest our galvanized index has been since December 2022. Similar to hot rolled, galvanized prices have been stable for some time, bobbing between $860-875/st across the past three months.

Figure 1 shows the pricing relationship between these two products for the last five years.

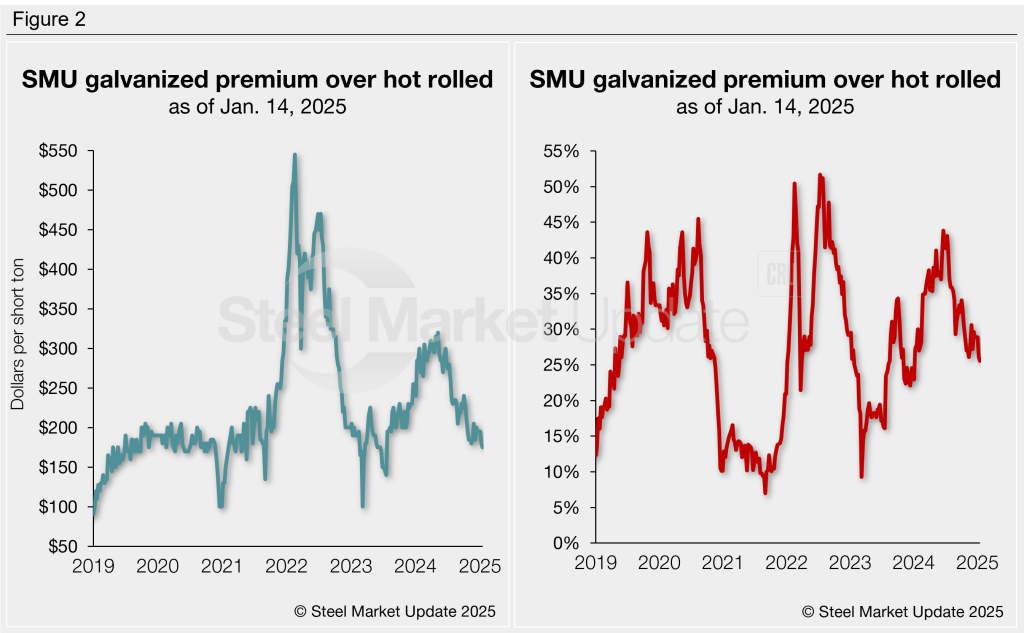

Galvanized premium shrinking

Currently, galvanized coil commands a $175/st price premium over hot-rolled steel on average. This is the lowest spread recorded since July 2023. The spreads observed over the last three months are similar to those seen in the latter half of 2023.

Over the last 12 months the average spread was $249/st. Historically, we saw pre-pandemic spreads mostly between $85-220/st for over a decade.

As shown in the left graph of Figure 2, the relationship between hot rolled and galvanized prices became volatile in late 2021. The spread reached a record-high $545/st by early 2022, gradually easing back to pre-pandemic levels by the end of that year. We saw another bump towards the end of 2023, with the spread peaking at $320/st in May 2024, then shrinking thereafter.

Another way to compare these products is to look at the galvanized premium as a percentage rather than a dollar value. The right graph in Figure 2 shows the hot-rolled/galvanized price spread as a percentage of the hot rolled price.

The percentage premium tells a somewhat different story. Through this week the premium is down to a one-year low of 26%. It had reached an almost two-year high of 44% last June, an upwards trend generally witnessed since March 2023 (when the premium had fallen to 9%). This time last year, the premium was slightly higher at 28%.

Prior to the pandemic volatility, galvanized prices held an average premium of 24% above hot-rolled prices from 2017 through the end of 2021. The premium reached a record high of 52% in July 2022.