Sheet

April 11, 2025

US, offshore CRC prices diverge

Written by David Schollaert

US cold-rolled (CR) coil prices declined this week, slipping for the first time since early February. Most offshore markets deviated, moving higher this week.

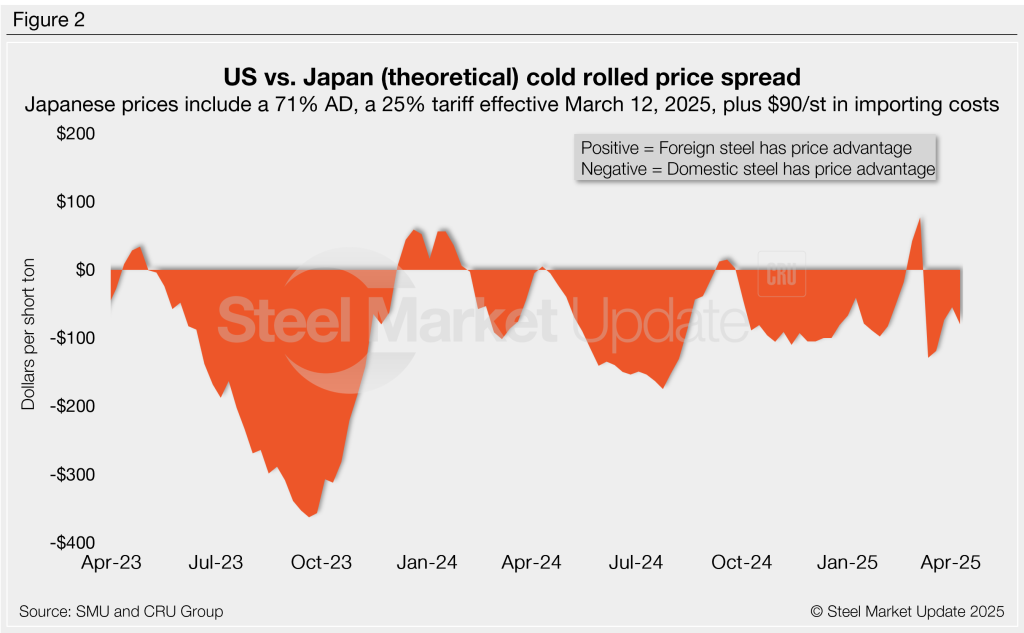

As a result, the US premium over imports on a landed basis widened. The move was helped by a tighter gap since the re-emergence of Section 232 on March 12.

In our market check on Tuesday, April 8, US cold-rolled (CR) coil prices averaged $1,135 per short ton (st), down $25/st from last week. The decline in prices comes as uncertainty in the US market around tariffs, especially after “Liberation Day,” has pushed buyers to the sidelines.

Domestic CR prices are now, theoretically, 16.9% higher than imports. That premium is down from 20% last week and well below 33.9% just before S232’s return.

In dollar-per-ton terms, US CR is, on average, $142/st more expensive than offshore product (see Figure 1) – down $33/st week on week (w/w) and now $143/st lower with S232 in effect.

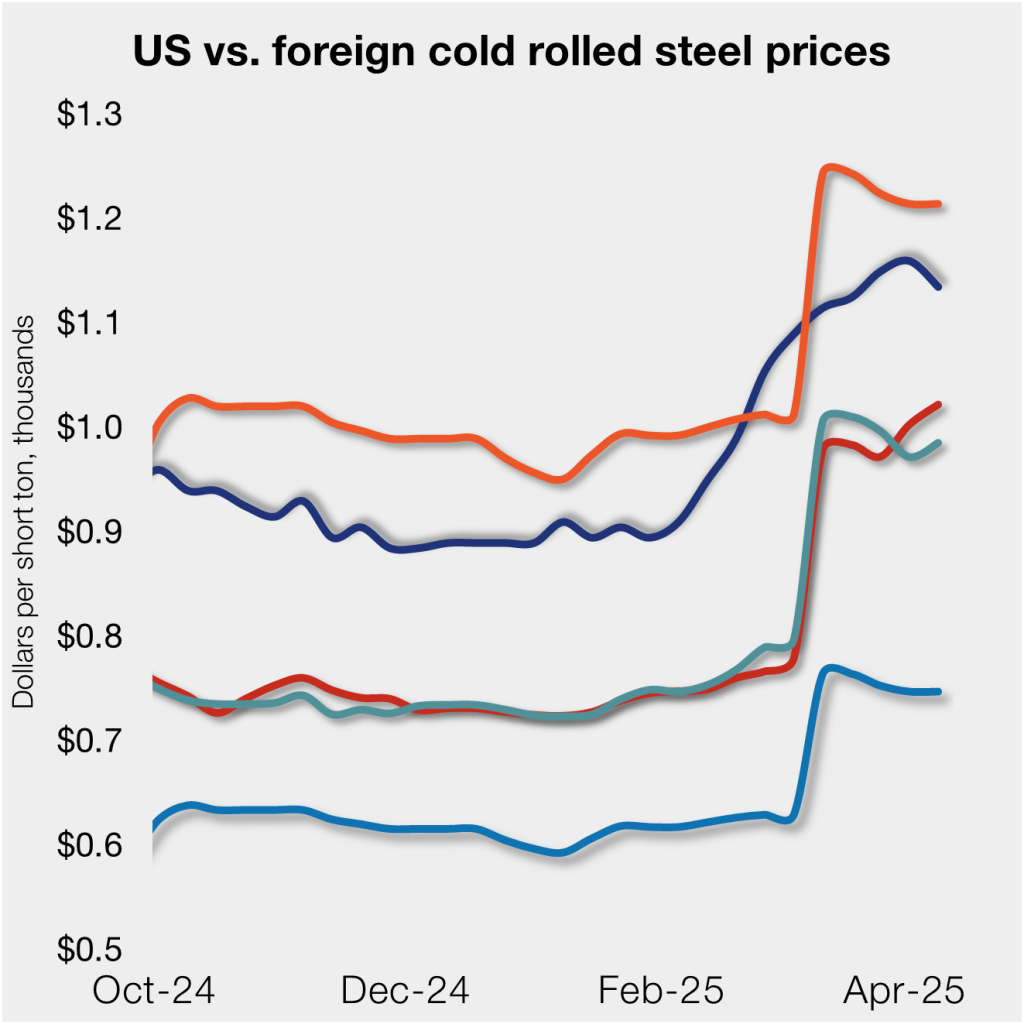

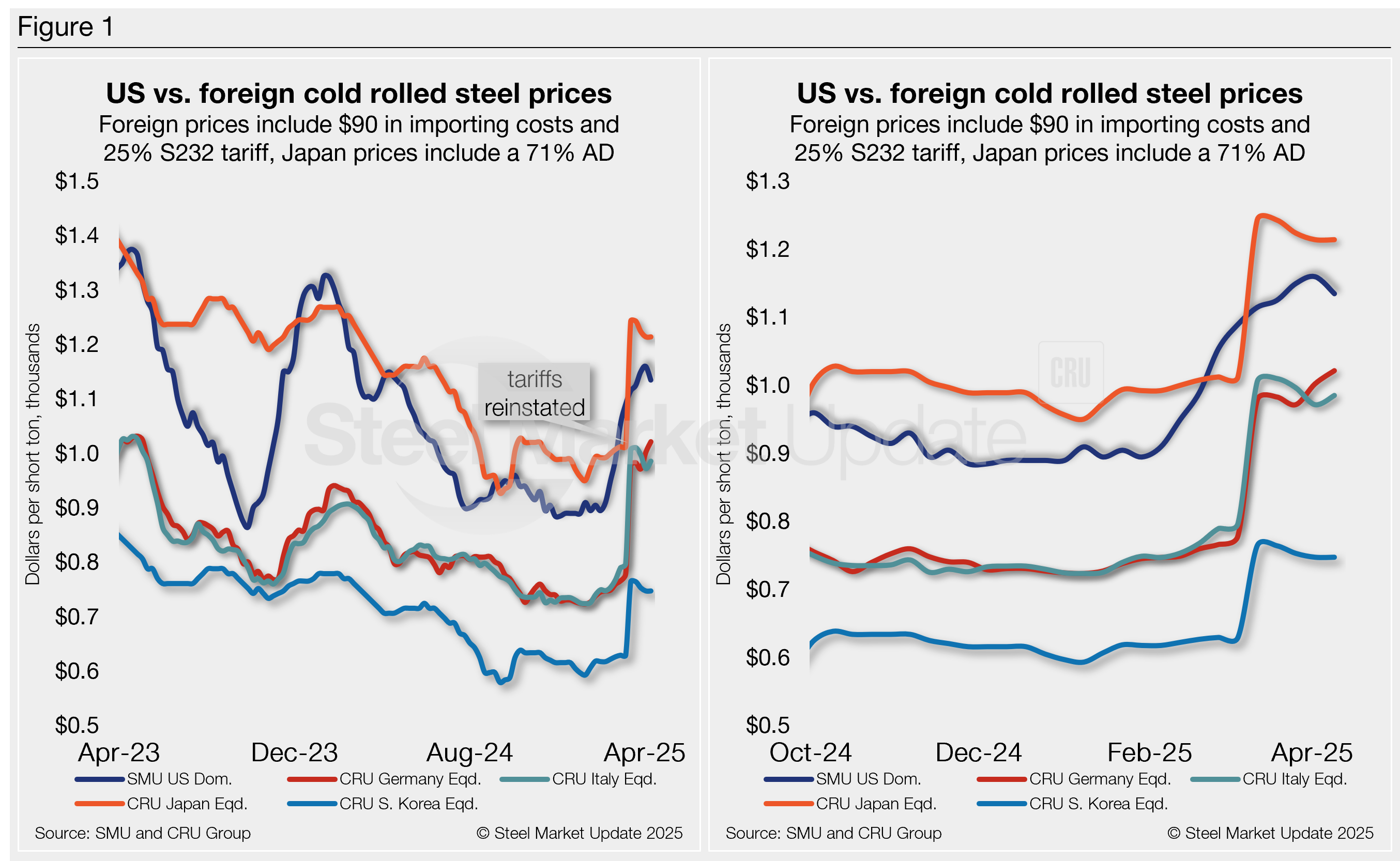

The charts below compare CR coil prices in the US, Germany, Italy, South Korea, and Japan. The left side shows prices over the last two years and the right side zooms in to highlight more recent trends.

Methodology

SMU calculates the theoretical price difference between domestic and imported cold-rolled (CR) steel by comparing our US CR price (FOB domestic mills) with CRU’s indices (DDP US ports) for Germany, Italy, and East Asia (Japan and South Korea). This is an estimate, as actual import costs vary.

To approximate the cost of foreign steel delivered to US ports, SMU adds $90/st to foreign prices to cover freight, handling, and trader margins. This benchmark can be adjusted based on individual shipping costs. (If you import steel and have insights on these costs, you can contact the author at david@steelmarketupdate.com.)

East Asian CR coil

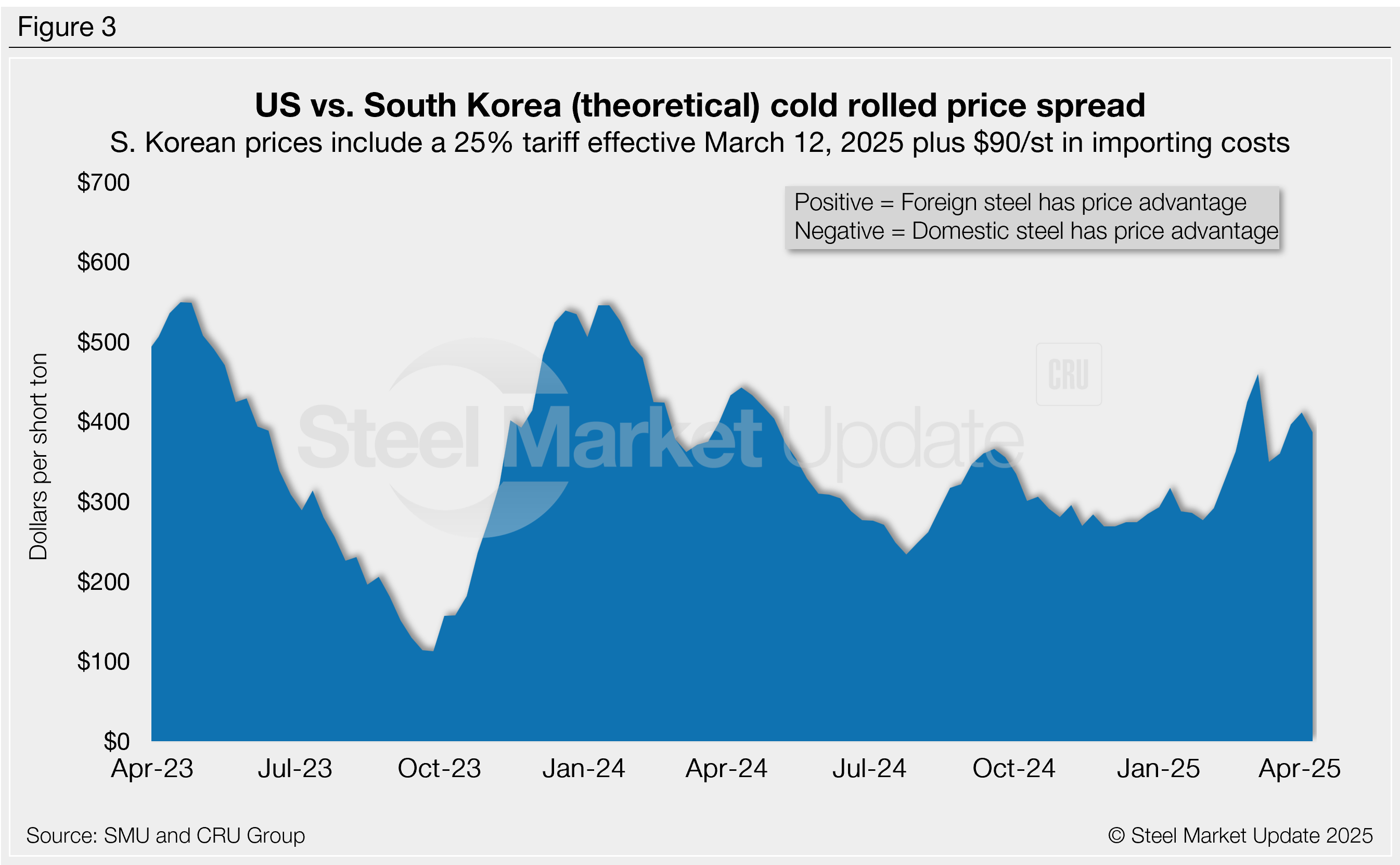

As of Thursday, April 10, the CRU Asian CR price stood at $526/st, flat w/w. Factoring in a 71% anti-dumping duty (Japan, theoretical), a 25% S232 tariff, and $90/st in estimated import costs, the delivered price to the US is $1,215/st. The theoretical landed price of South Korean CR exported to the US is $748/st.

With the latest SMU CR price down $25/st to an average of $1,135/st, US-produced CR is now theoretically $80/st below Japanese imports but $387/st above South Korean imports.

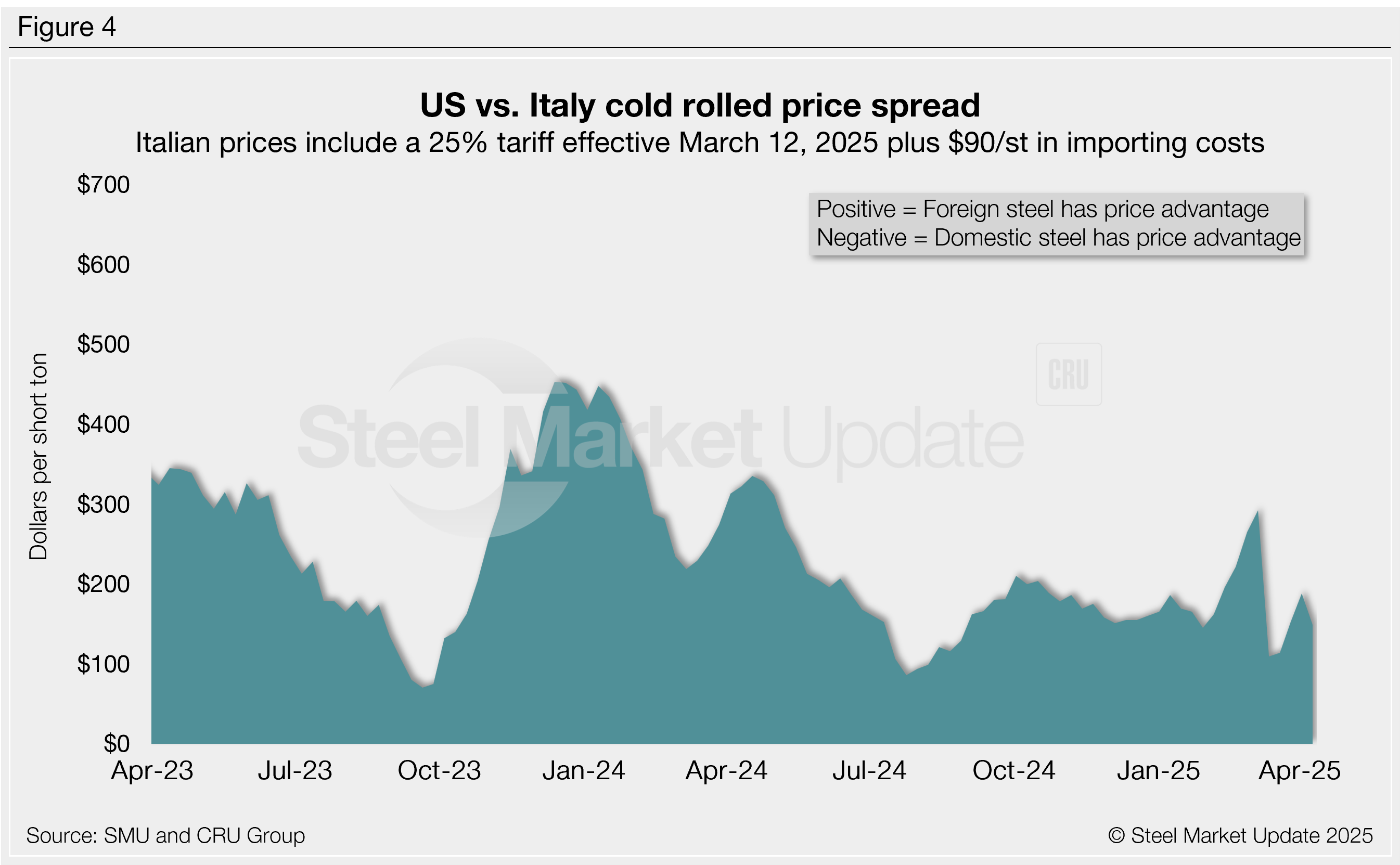

Italian CR coil

Italian CR prices ticked up $11/st this week to $717/st. After adding import costs and a 25% tariff, the price of Italian CR delivered to the US is, in theory, $986/st.

That means domestic CR is still theoretically $149/st more expensive than CR coil imported from Italy. The spread is down $39/st vs. last week, but $143/st off from about a month ago before S232 was reinstated.

German CR coil

CRU’s German CR price was up $16/st vs. the previous week. After adding import costs and a 25% tariff, the delivered price of German CR is, in theory, $1,022/st.

The result: Domestic CR is theoretically $113/st more expensive than CR imported from Germany. The spread is down $44/st w/w, yet still nearly a $200/st cut since S232’s re-emergence.

Editor’s note

We reference domestic prices as FOB the producing mill, while foreign prices are CIF the port (Houston, NOLA, Savannah, Los Angeles, Camden, etc.). Inland freight from either a domestic mill or a port is important to keep in mind when deciding where to source from. It’s also important to factor in lead times. In most market cycles, domestic steel will deliver more quickly than foreign steel. Note also that, effective March 12, 2025, undiluted Section 232 tariffs were reinstated on steel imports. Therefore, the Japan, South Korea, German, and Italian price comparisons in this analysis now include a 25% tariff.