CRU

July 3, 2025

CRU: Excessive global supply could hit rebar mill investments in US

Written by Alexandra Anderson

Following the onset of the war in Ukraine in March 2022, concerns about import availability and expectations of rising demand from President Biden’s Infrastructure Bill pushed US rebar prices to record highs. In response, a flurry of new mills and capacity expansions were announced to meet the rise in demand from growth in the construction sector.

Three years later, stronger end-use consumption has been slow to materialize, and President Trump’s rapid changes to tariffs and trade policy have muddied the economic outlook. Revisions to Section 232 have leveled the playing field in terms of imports, and some countries that were only occasionally present in the US market are starting to gain market share.

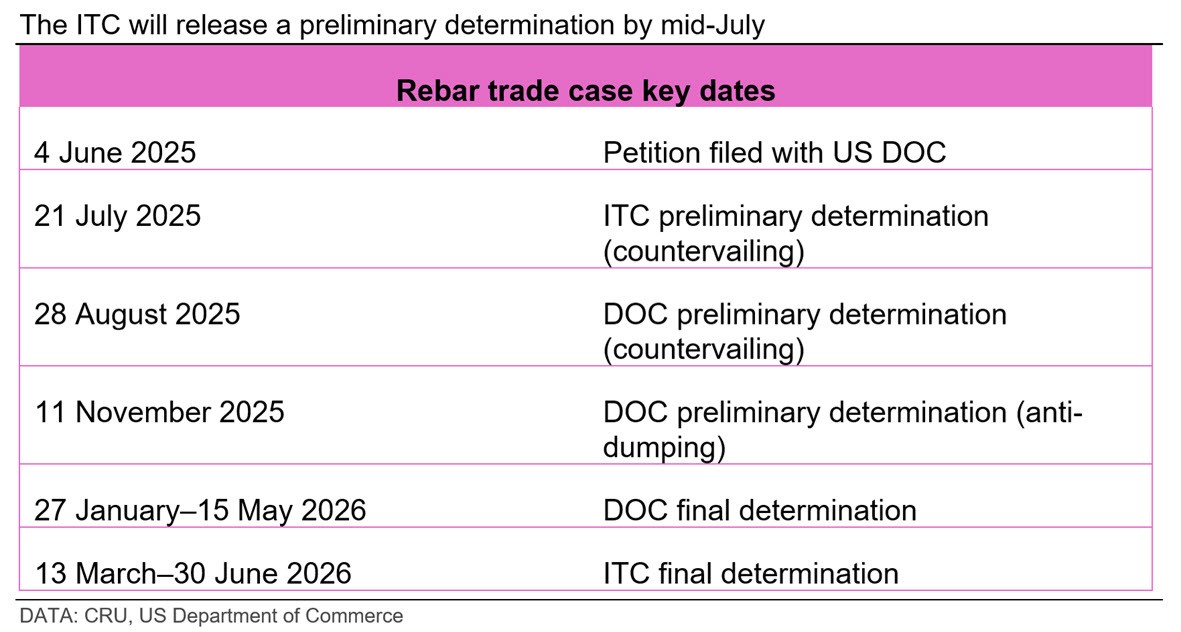

Domestic producers have taken notice. On June 4, the Rebar Trade Action Coalition submitted a petition with the International Trade Commission (ITC) to initiate anti-dumping duties on rebar from Algeria, Bulgaria, Egypt, and Vietnam.

This comes at the same time that several of the previously announced greenfield projects and mill expansions are ramping up. The additional capacity will effectively displace a portion of imports. However, the US is and will remain a net importer of long products. This begs the question: Will this trade case have a meaningful impact?

This insight will explore developments in domestic production, the dynamics of the US rebar market, and changes in trade as a result of tariffs. Considering these factors together should bring clarity on how important this trade case is to the US rebar market.

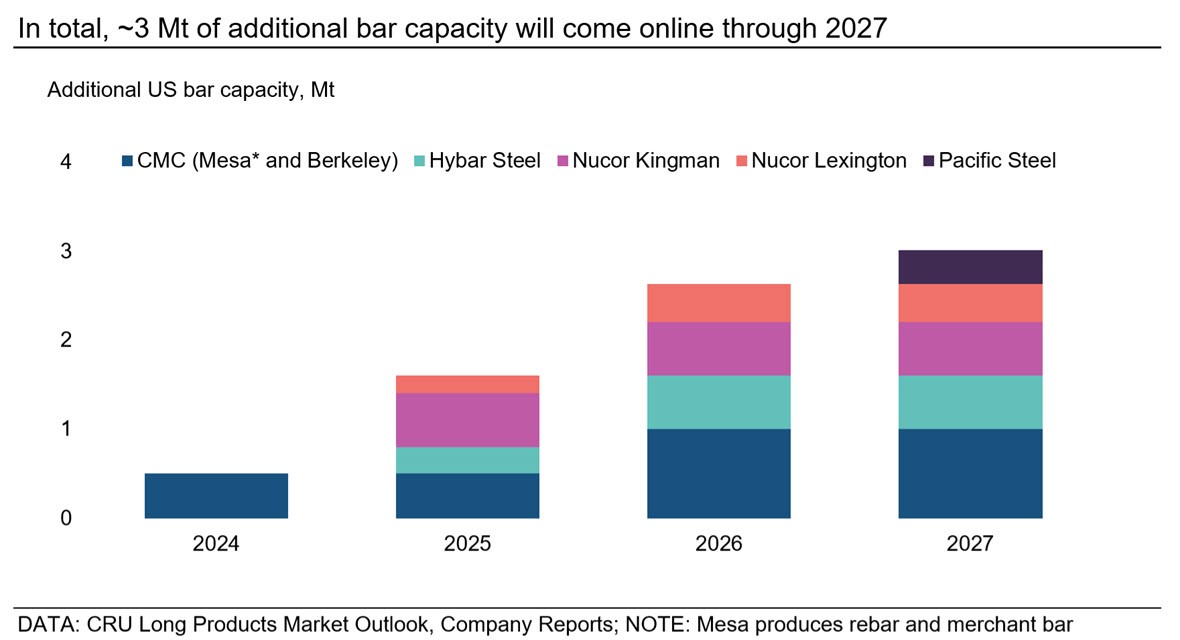

The US will add 2 million mt of rebar production over the next few years

In 2022, expectations of rising demand, along with the prospect of higher sustained prices due to lagging production, prompted numerous announcements of greenfield rebar projects, as well as capacity expansions. In all, nearly 6 million metric tons (mt) of rebar production was proposed to come online through 2027.

The first of these to reach completion was CMC’s Arizona 2 mill in Mesa, Ariz., which started in 2024 and can produce 500,000 mt per year of bar products. In 2025, more than 1.5 million mt of added capacity is set to ramp up from new players and incumbents.

Steel industry veteran David Stickler’s newest investment, Hybar, rolled its first rebar in early June at its plant in Osceola, Ark. In addition to using 100% scrap feedstock, the plant implements a direct connection to a solar installation and battery storage, meaning it can run fully on renewable solar power. These innovations have allowed Hybar to obtain Climate Bond certification, and they strive to eventually secure LEED (Leadership in Energy and Environmental Design) certification, an endeavor that Stickler achieved during his time at Big River Steel.

Nucor is expanding capacity in 2025 as well. It added a melt shop to its Kingman, Ariz., bar mill, which it expects will produce 600,000 mt per year, in addition to a 500,000 mt per year micro mill in Lexington, N.C. Both of these projects are ramping up now and anticipated to be operational sometime in Q3’25.

Looking ahead, CMC is also building a micro mill in Berkeley, W.Va., which is expected to start in H1’26 and produce 500,000 mt per year of rebar. Pacific Steel has a 380,000-mt-per-year micro mill in California slated for 2027. Several other new players in the US market also pledged to add 1.7 million mt per year of production but have not announced target dates.

Rising demand means the US will still require imports

While CRU’s economic outlook for 2025 has cooled, the years ahead will bring some recovery for finished steel consumption. Construction activity will rebound as projects already funded through the IIJA continue to support infrastructure spending. Manufacturing should see a bump from steel mills being built, as well as investments in reshoring across various sectors. The shift toward AI supports continued data center construction, too, further bolstering non-residential construction activity.

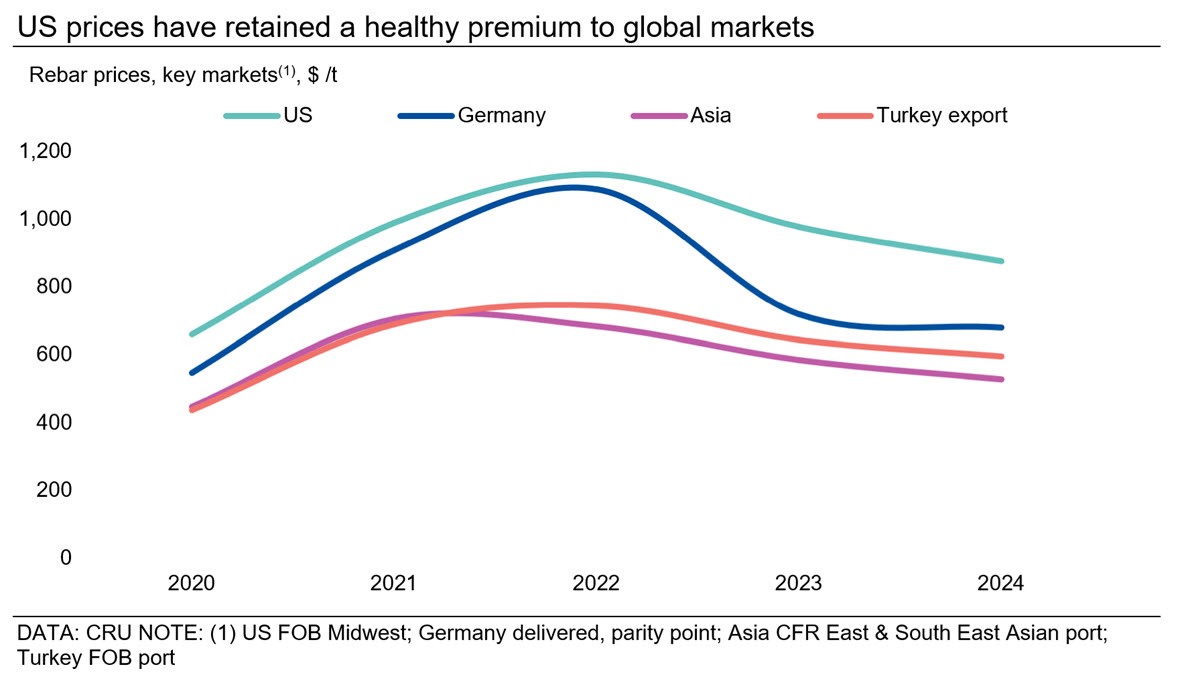

As demand grows, even with new domestic capacity, the US will remain a net importer of rebar. Historically, most US rebar imports have come from Mexico, Turkey, and, in part, Algeria. Mexico’s share of imports has been cut in half since 2020, and low-cost producers like Egypt have taken their place.

Global oversupply remains a risk for the US market

Even as demand has continued to rise over the last decade, expansions in domestic production lagged. Consequently, US rebar imports ballooned to 1.6 million mt in 2016, up more than 450% from the 2011–13 average of ~289,000 t. This resulted in ~1 million mt of bar capacity added to the US market through 2020.

Global capacity has also continued to rise. The latest edition of CRU’s Steel Long Products Market Outlook forecasts that world ex. China production will grow ~6% over the next five years.

Cost-competitive producers in Africa and Southeast Asia will add more than 8.5 million mt of capacity during this time, though demand in those regions grows at a slower pace. Even with tariffs and duties, the overall lower costs for these producers make them a viable option for net importing countries like the US.

Section 232 brings support but is not a long-term solution

The revision of Section 232 to include material from Canada and Mexico has stemmed imports from those regions but also allowed opportunities for others to gain market share. While raising the tariff rate from 25% to 50% will support the US market, effects are generally short-lived after the initial shock.

Negotiations on reciprocal tariffs are ongoing and increasing the Section 232 rate should help move along discussions. As deals are reached, it’s likely we see a drop back to 25% on Section 232 or even some exemptions, letting steam out of the upward pressure on prices. Therefore, any longer-lasting solution to curb imports will come in the form of anti-dumping or countervailing duties.

Ultimately, the case could mitigate risk for upcoming capacity

After the US Department of Commerce decides whether or not to initiate the case, the ITC preliminary determination is scheduled for mid-July. If approved, trade flows could shift again to re-include more traditional trade partners, specifically Mexico. Furthermore, it will stem the risk of new mill investments being undercut by oversupply in the global market.

CRU will continue to monitor developments in the longs market related to this trade case, which can be found in the Long Products Monitor and Long Products Market Outlook.

This piece was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.