Analysis

July 10, 2025

SMU Community Chat: CRU analysts discuss shifting metallics mart tangled by tariffs

Written by Laura Miller

With steel prices drifting and trade flows shifting, CRU analysts provided a grounded look at what’s really happening — and what’s not — across the metallics supply chain during Wednesday’s SMU Community Chat.

Some key takeaways? Metallics markets are tangled in tariffs, zinc demand is sliding, and reshoring is still more talk than action.

Metallics market moves

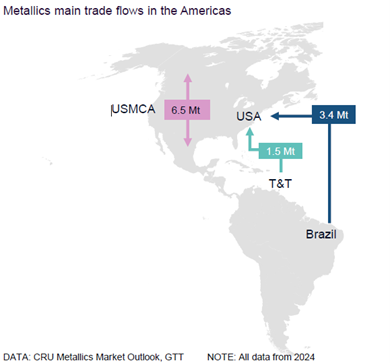

Thais Terzian, CRU principal analyst, steel, began her presentation with a broad overview of metallics — scrap, DRI/HBI, and pig iron — and the shifting trade routes they follow.

“I was kind of impressed on how big the interdependency of the metallics market within the Americas was,” Terzian commented, noting how US scrap crisscrosses borders with Canada and Mexico (see image).

She pointed out that 100% of US imports of DRI/HBI come from Trinidad & Tobago. And despite the material being traded inter-company (Nucor owns the Nu-Iron Unlimited Point Lisas DRI plant in Trinidad), it’s still subject to a 10% tariff. Additionally, 75% of US pig iron imports come from Brazil, and those also face tariffs.

The scrap market, meanwhile, has stayed relatively insulated. “Scrap is USMCA compliant, so it’s not under any taxation,” she noted. That makes it a safe haven in a volatile metallics environment and explains why US exports in the region remain strong.

Terzian said the spikes in scrap prices that followed March’s tariff announcement were short-lived. “There was an oversupply in the market … a lot of new financials in April,” she commented. Pig iron buyers pivoted to prime scrap, pushing spreads higher than usual. At one point, “Prime scrap became more expensive than pig iron,” she noted.

With the addition of a host of new EAF steelmaking capacity in the US, CRU anticipates a continued decline in US scrap exports, a reduced reliance on slab imports, and higher levels of pig iron imports.

The analyst also warned of a potential undersupply in DRI/HBI, given rising demand, limited new production in Brazil, and Russian and Ukrainian material still off the table. While Cleveland-Cliffs and SSAB have pulled back on domestic DRI investments, Nippon Steel has said it could potentially construct DRI facilities at U.S. Steel’s Big River Steel. (See Stephen Miller’s recent story Are more DRI investments coming to the US? for more information.)

Mexico is also investing in new slab capacity to reduce its exposure to imports. New slab production capacity from Ternium and Grupo Acero will reduce the country’s need for imports, she said.

Brazil is the dominant player in semi-finished steel in the Americas. In 2024, 80% of its slab and billet exports went to the US and Mexico, according to Terzian’s presentation. With both countries increasing their own slab production, Brazilian producers have had to diversify and find new destinations for their product.

She said CRU is already seeing Brazilian product beginning to fill a void in the European market left by sanctions on Russian slab and capacity closures in the UK and elsewhere.

Note, after the Community Chat on Wednesday, Trump announced a hike in the US tariff rate – to 50% – for imports from Brazil. Check out Michael Cowden’s article on why the South American country matters so much to the steel industry here.

Zinc losing steam

Frank Nikolic, vice president of base and battery metals for CRU in North America, provided a solid overview of zinc.

Used to enhance corrosion resistance, zinc is a chemical element utilized across various industrial applications, but primarily for galvanizing steel. In fact, galvanized steel accounts for ~60% of global zinc consumption.

This makes construction the largest end-use market for zinc, accounting for nearly half (48%) of demand, followed by engineering and infrastructure (16%), consumer and other (11%), and automotive (10%).

Since zinc is used in the early stages of construction, it is highly sensitive to infrastructure investment cycles, Nikolic said.

He said the entire value chain is being pressured by falling demand, especially from China, whose building boom peaked almost a decade ago.

And zinc’s decline tracks alongside the country’s broader shift “from a societal uplift to more of a consumer economy,” he explained.

What does that mean for the zinc market in North America? It’s vulnerable, especially given how reliant the US is on Canadian and Mexican supplies, said Nikolic. Tariff uncertainty is freezing investment: “Decision-makers need to see stability and direction before committing large amounts of capital,” he warned.

And while zinc prices have been stable, they’re stuck in a narrow band. “We have seen a steady decline in LME stocks,” Nikolic noted. This suggests a tightening supply, especially if demand were to snap back anytime soon.

Reshoring in North America

“If there’s permanence to these tariffs,

the world will be shuffled.”

– Frank Nikolic

While reshoring is a popular talking point, we aren’t yet seeing those projects translate into real production or sourcing shifts.

During SMU Editor-in-Chief Michael Cowden’s introduction on the chat, he pointed out that, despite the higher tariffs on imports, most steel buyers at this point aren’t seeing any meaningful reshoring activity.

Terzian later added that some new DRI and semi-finished capacity has been announced in the US and Mexico, but nothing has really materialized at scale.

On the mining front, Nikolic emphasized how long timelines and regulatory hurdles make reshoring difficult in practice, not just theory.

So, reshoring may still be more of a buzzword than a reality at this point, but that doesn’t mean shifts in supply chains aren’t coming – they just might take some time to take shape.

Editor’s note

If you missed Wednesday’s chat, SMU subscribers can access a replay of this Community Chat, as well as past webinars we’ve hosted, on our website.

Thais Terzian and Frank Nikolic will be speaking at the upcoming SMU Steel Summit in Atlanta. They’ll join Estelle Tran, CRU steel prices analyst, on the main stage on the afternoon of Tuesday, Aug. 26, to discuss CRU’s views of the steel and metallics markets. For more information or to register for the Summit, visit the event page here.