Market Data

September 16, 2025

SMU Price Ranges: HR slips, hopes for Q4 rebound still standing

Written by Brett Linton & Michael Cowden

SMU’s price ranges were mixed again this week as the market continues to seek a floor amid industry hopes for a Q4 rebound.

Spotlight on HR

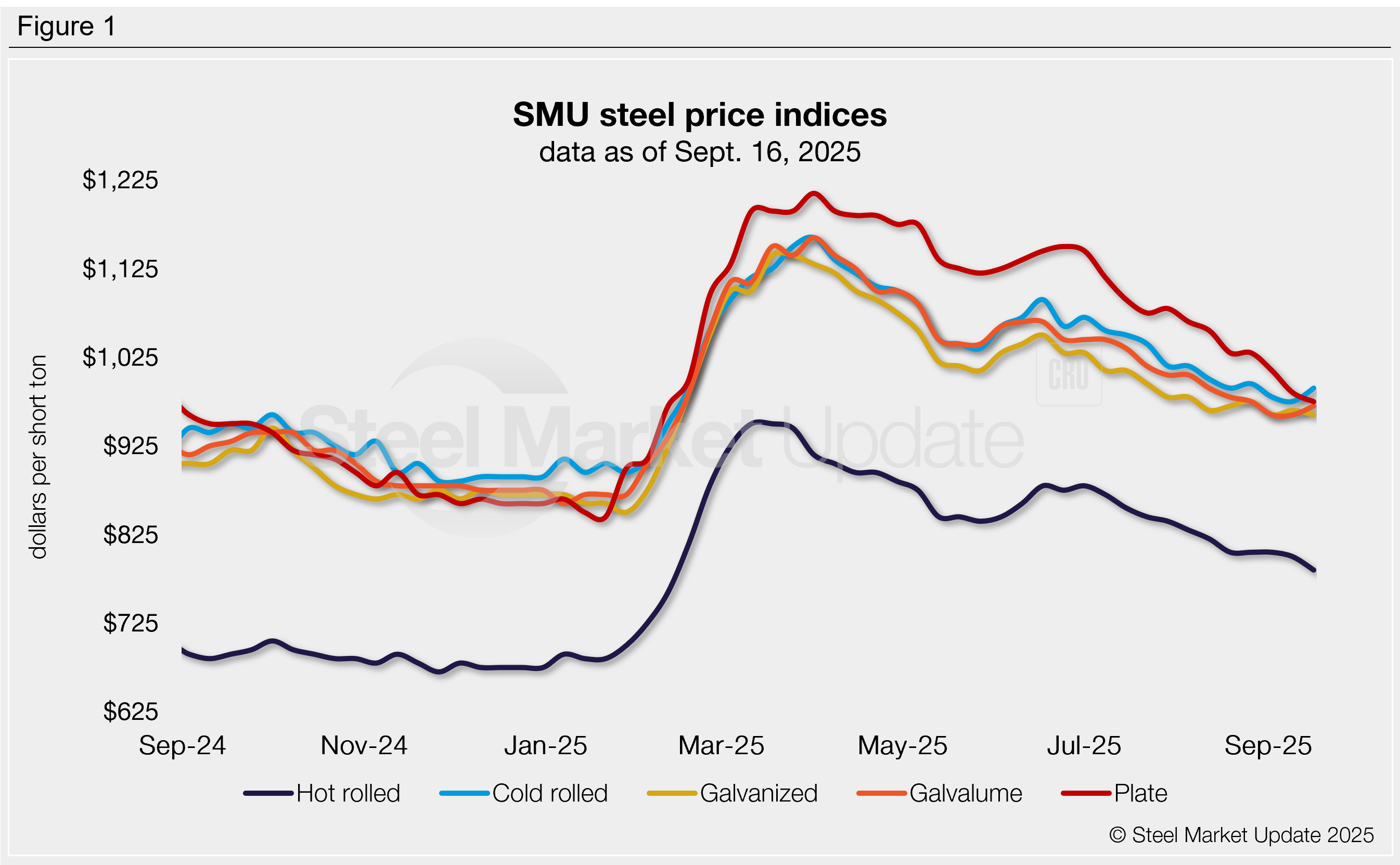

Our hot-rolled coil price slipped to $785 per short ton (st) on average, down $15/st from last week. The latest decline means HR prices are now at their lowest point since mid-February, before President Trump’s re-imposition of blanket Section 232 tariffs. (You can find such historical information with SMU’s interactive pricing tool.)

The dip came as market participants reported that deals in the lower $700s/st remained available for larger buyers (~5,000/st minimum order). We also found few buyers transacting at mill list prices in the upper $800s/st, which brought the high end of our range down.

There had been hopes last week that HR deals in the low $700s/st would be gone from the market this week. But industry sources said the US market remained under pressure from certain Canadian mills that continue to sell into the Midwest at numbers in the low $700s/st. Some questioned how Canadian producers could do so profitably given that such offers include both freight and a 50% Section 232 tariff.

While some market participants think such low-priced deals will remain available, others think they’ll soon be out of the market.

CR, coated, and plate

But prices were not down across the board.

SMU’s cold-rolled price, for example, increased to $990/st on average, up $15/st from a week ago. Our galvanized price slipped to $960/st on average, down $5/st from last week. The decline in galv came as sources said lead times at certain mills were as short as three weeks. Our Galvalume base price, however, rose $10/st to $970/st on average.

Also of note on Galvalume front: Coating extras are up on a sharply higher Midwest premium (MWP) for aluminum. The MWP has skyrocketed on the imposition of Section 232 tariffs on imported aluminum, including material from Canada – where the US gets most of its aluminum from. And while US steel mills have increased capacity, there has been no similar expansion to date on the aluminum side.

Plate prices, meanwhile, slipped to $975/st, down $10/st from last week – and marking their lowest point since February – on continued concerns about demand.

Market commentary

Broadly speaking, some US mills continue to have October tons available, and they appear more willing to negotiate lower prices to fill orderbooks for next month. But other mills have closed October, and market participants think they could open November books at higher numbers.

Most market sources we contacted continue to expect that prices will move higher this fall on lower imports, lower inventories, mill maintenance outages, and better demand following the typically slower summer months. They say it’s just a question of whether that inflection point happens a week from now or a month from now.

But others countered that the most notable impact of fall outages so far had been a $20 per gross ton (gt) drop in prime scrap prices thanks to reduced scrap demand from sheet mills. They also suggested that new domestic capacity could largely replace imports. And they in addition weren’t convinced that demand would improve enough to support higher prices.

Momentum

SMU is keeping its sheet and plate momentum indicators at lower on flat or lower scrap prices, continued discounting from North American mills, and ongoing concerns about demand. But if we see more concrete signs of a bottom forming, we’ll switch them to neutral.

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil

The SMU price range is $720–850/st, averaging $785/st FOB mill, east of the Rockies. The lower end of our range is unchanged w/w, while the top end is down $30/st. Our overall average is down $15/st w/w. Our price momentum indicator for hot-rolled steel remains at lower, meaning we expect prices to decline over the next 30 days.

Hot-rolled lead times range from 3–6 weeks, averaging 4.5 weeks as of our Sept. 4 market survey. We will publish updated lead times on Thursday.

Cold-rolled coil

The SMU price range is $920–1,060/st, averaging $990/st FOB mill, east of the Rockies. The lower end of our range is up $30/st w/w, while the top end is unchanged. Our overall average is up $15/st w/w. Our price momentum indicator for cold-rolled remains lower, meaning we expect prices to decline over the next 30 days.

Cold-rolled lead times range from 4–8 weeks, averaging 6.0 weeks through our latest survey.

Galvanized coil

The SMU price range is $900–1,020/st, averaging $960/st FOB mill, east of the Rockies. The lower end of our range is unchanged w/w, while the top end is down $10/st. Our overall average is down $5/st w/w. Our price momentum indicator for galvanized steel remains lower, meaning we expect prices to decline over the next 30 days

Galvanized .060” G90 benchmark: SMU price range is $978–1,098/st, averaging $1,038/st FOB mill, east of the Rockies.

Galvanized lead times range from 4–8 weeks, averaging 6.1 weeks through our latest survey.

Galvalume coil

The SMU price range is $920–1,020/st, averaging $970/st FOB mill, east of the Rockies. The lower end of our range is up $20/st w/w, while the top end is unchanged. Our overall average is up $10/st w/w. Our price momentum indicator for Galvalume steel remains lower, meaning we expect prices to decline over the next 30 days.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,274–1,374/st, averaging $1,324/st FOB mill, east of the Rockies. Note that the coating extras for this benchmark have been adjusted this week in consideration of revised U.S. Steel extras, increasing from $268/st to $354/st.

Galvalume lead times range from 5–8 weeks, averaging 6.4 weeks through our latest survey.

Plate

The SMU price range is $950–1,000/st, averaging $975/st FOB mill. The lower end of our range is up $20/st w/w, while the top end is down $40/st. Our overall average is down $10/st w/w. Our price momentum indicator for plate remains lower, meaning we expect prices to decline over the next 30 days.

Plate lead times range from 3–7 weeks, averaging 5.3 weeks through our latest survey.

SMU note: The graphic above shows a history of our hot rolled, cold rolled, galvanized, Galvalume, and plate prices. This data is also available on our website with our interactive pricing tool. If you need help navigating the site or logging in, contact us at info@steelmarketupdate.com.

Brett Linton

Read more from Brett Linton