Market Data

October 7, 2025

SMU Price Ranges: HR holds, galv slips amid competing market narratives

Written by David Schollaert & Michael Cowden

SMU’s sheet and plate prices see-sawed this week as hot-rolled (HR) coil prices held their ground while prices for galvanized product slipped.

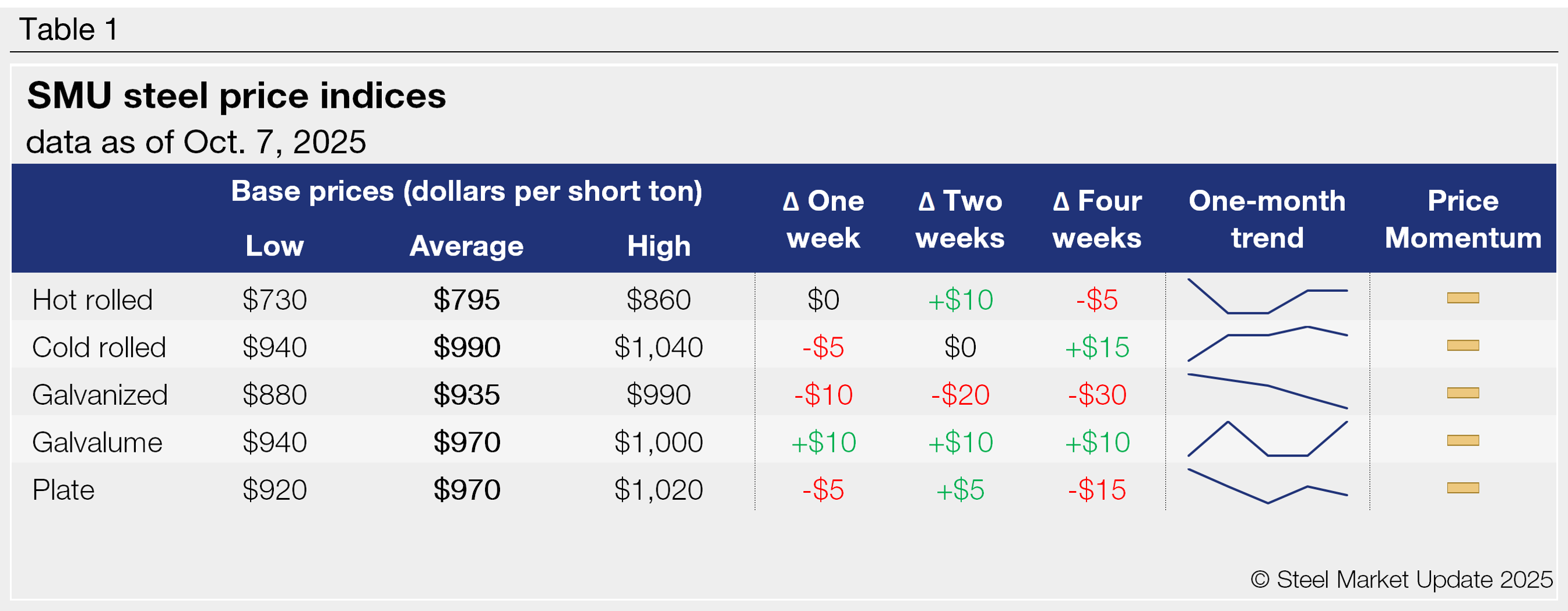

Our average HR price remained unchanged week over week (w/w) at $795 per short ton (st). While our overall price didn’t move, there was significant regional variation.

In the North, domestic mills remain in the mid/low $700s/st for larger buyers, market participants said. But rock-bottom prices that had been in the market just two weeks ago appear to be gone, they added.

In the South, major domestic mills appear to be in a stronger position and are less willing to chase HR numbers below $800/st – even for larger orders, market participants said. But some noted that new capacity continues to offer tons in the mid/low $700st/st.

When it comes to value-added products, CR stands at $990/st on average, down $5/st from last week. Galvanized base prices were at $935/st on average, down $10/st w/w. And Galvalume prices stand at $970/st on average, up $10/st w/w.

Why the drop in galvanized? HR-base product at certain mills continues to sell at a significant discount to CR-base product. And while market participants generally agreed that HR prices were at or near a bottom, several said it was too soon to tell the same of the galvanized market, where weakness in construction, imports of light-gauge material, and new capacity continue to weigh on prices.

On the plate side, meanwhile, tags were little changed at $970/st on average, down $5/st from last week. The market continues to digest the impact of a round of $60/st price hikes.

Momentum

SMU’s price momentum indicators for both sheet and plate remain at ‘neutral’ amid conflicting market narratives.

For example, some sources expect sheet price hikes within the next month, as it becomes clear that the market has bottomed and pricing power shifts to US mills. Others say the market could weaken again once fall maintenance outages have concluded and as lead times stretch closer to the seasonally slower Thanksgiving and Christmas holiday seasons.

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil

The SMU price range is $730–860/st, averaging $795/st FOB mill, east of the Rockies. The lower and top ends of our range are unchanged w/w. Thus, our overall average is also flat w/w. Our price momentum indicator for HR steel has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

HR lead times range from 3 to 6 weeks, averaging 4.7 weeks as of our Oct. 1 market survey.

Cold-rolled coil

The SMU price range is $940–1,040/st, averaging $990/st FOB mill, east of the Rockies. The lower end of our range is down $10/st w/w, while the top end is unchanged. Our overall average is down $5/st w/w. Our price momentum indicator for cold rolled has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

CR lead times range from 5 to 8 weeks, averaging 6.4 weeks through our latest survey.

Galvanized coil

The SMU price range is $880–990/st, averaging $935/st FOB mill, east of the Rockies. The lower end of our range is flat w/w, while the top end is down $20/st. Our overall average is down $10/st w/w. Our price momentum indicator for galvanized steel has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Galvanized .060” G90 benchmark: SMU price range is $958–1,068/st, averaging $1,013/st FOB mill, east of the Rockies.

Galvanized lead times range from 4 to 8 weeks, averaging 6.4 weeks through our latest survey.

Galvalume coil

The SMU price range is $940–1,000/st, averaging $970/st FOB mill, east of the Rockies. The lower end of our range is up $20/st w/w, while the top end is unchanged. Our overall average is up $10/st w/w. Our price momentum indicator for Galvalume steel has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,294–1,354/st, averaging $1,324/st FOB mill, east of the Rockies.

Galvalume lead times range from 5 to 8 weeks, averaging 6.7 weeks through our latest survey.

Plate

The SMU price range is $920–1,020/st, averaging $970/st FOB mill. The lower end of our range is down $20/st w/w, while the top end is up $10/st. Our overall average is down $5/st w/w. Our price momentum indicator for plate has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Plate lead times range from 4 to 7 weeks, averaging 5.1 weeks through our latest survey.

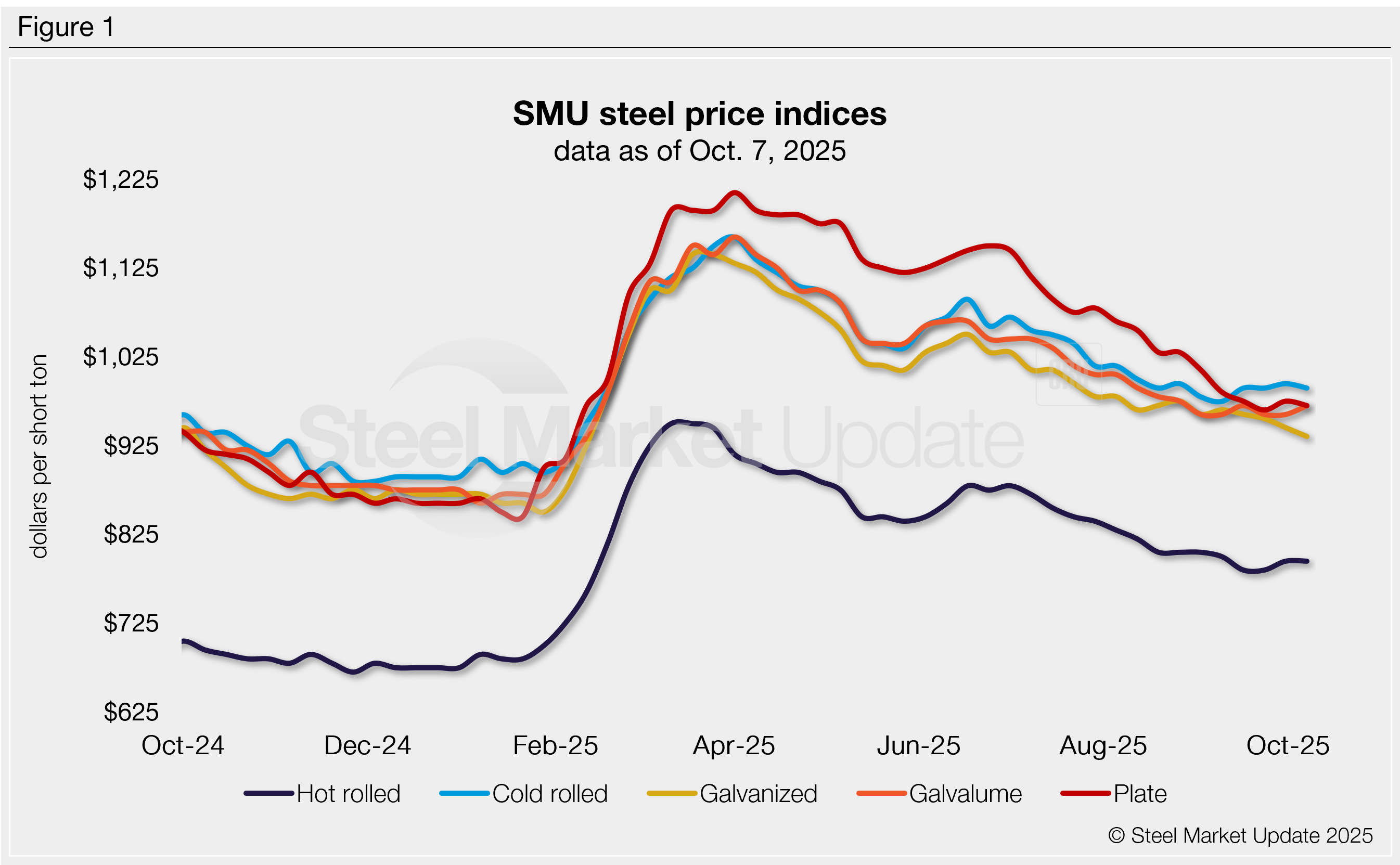

SMU note: The graphic above shows a history of our hot rolled, cold rolled, galvanized, Galvalume, and plate prices. This data is also available on our website with our interactive pricing tool. If you need help navigating the site or logging in, contact us at info@steelmarketupdate.com.

David Schollaert

Read more from David Schollaert