Analysis

October 10, 2025

CRU: China’s indirect steel exports find new destination markets

Written by Juliana Guarana & Ying Jie Ong

This news item was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.

Chinese direct and indirect steel exports are on the rise

The boom in China’s direct steel exports has not stopped in 2025. After an increase of 24% y/y in 2024, Chinese direct steel exports rose by 7% y/y in the first half of 2025, even with a rise in protectionist measures globally.

The increase in Chinese direct steel exports is driven by an attempt to maintain high production levels against a backdrop of lower domestic steel demand in China, particularly from the construction sector. Demand for exports has been supported by the strong cost competitiveness of Chinese steel products (see the related CRU Insight here).

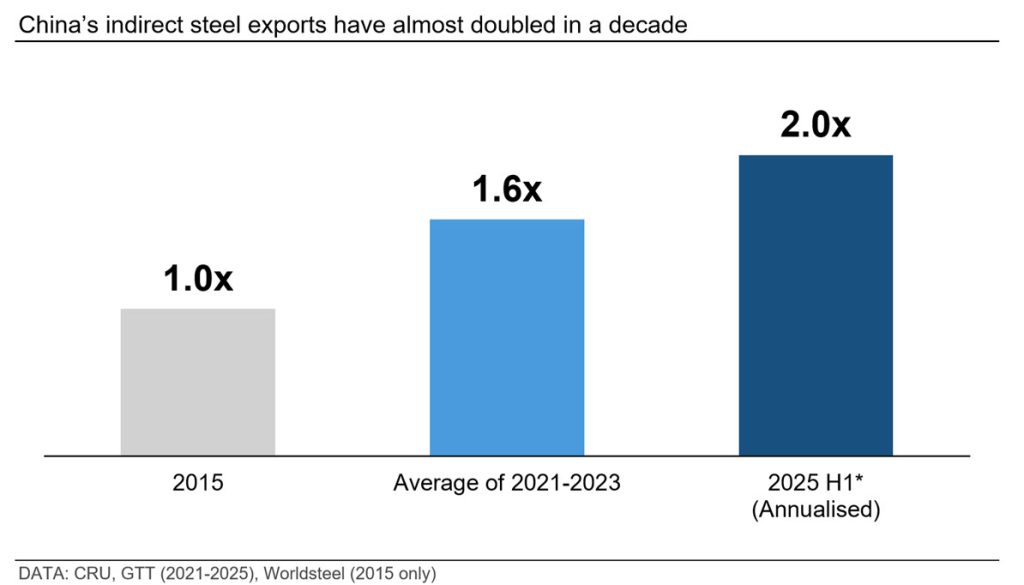

Similarly, Chinese indirect steel exports increased significantly in 2024, reaching 136 million metric tons (mt), an increase of nearly 20% y/y. According to CRU’s Global Steel Trade Service, China’s indirect steel exports reached 72 million mt in H1’25, an 11% y/y increase.

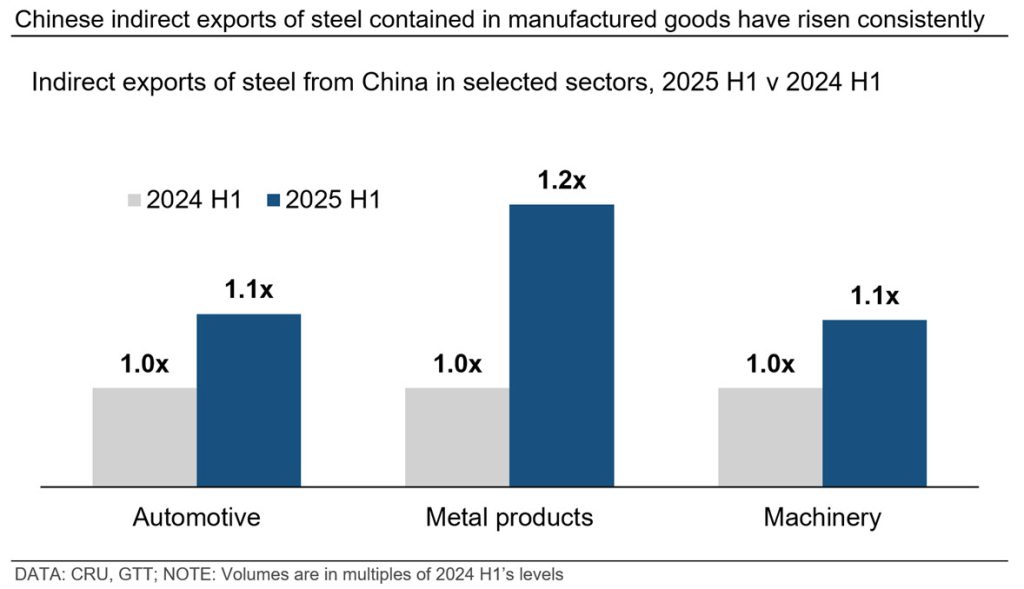

Chinese metal products exports drove the strong growth

Metal products and mechanical machinery sectors account for over 60% of China’s indirect steel exports. The significant growth in Chinese indirect exports of steel H1’25 was mainly driven by exports from the metal products sector, which increased 19% y/y. This sector includes a wide range of products such as containers, metal tools, nails, furniture, and household articles. Exports of electrical equipment recorded a 14% y/y increase in H1’25, while those of automotive increased by 8% in the same period.

All Chinese steel-containing goods sectors, such as mechanical machinery, automotive, and domestic appliances, have seen increased export volumes since 2024. The other transports sector registered the strongest growth in 2024, with a 58% y/y increase, followed by the domestic appliances sector, with a 21% increase.

Trade protectionism has forced a shift in destinations

China’s long-term economic strategy is set to drive the country’s industrial sector further downstream towards higher-value products (see CRU’s Steel Long Term Market Outlook). In line with this, Chinese manufacturers have strategically pursued new markets. This partly mitigates the impact of increased global protectionism (see the related CRU Insight here).

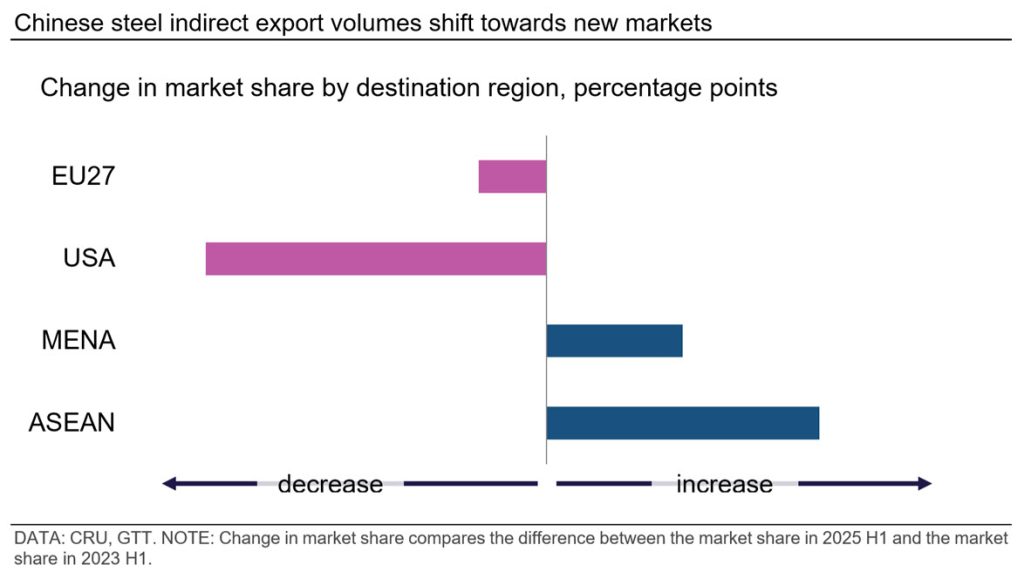

As the chart below illustrates, the share of Chinese indirect steel exports to the US has declined since 2023. This trend has intensified in H1’25, as US President Donald Trump introduced a set of new tariffs that impacted the entire ferrous supply chain (see the related CRU Insight here). Meanwhile, ASEAN and MENA shares have increased significantly in the same period.

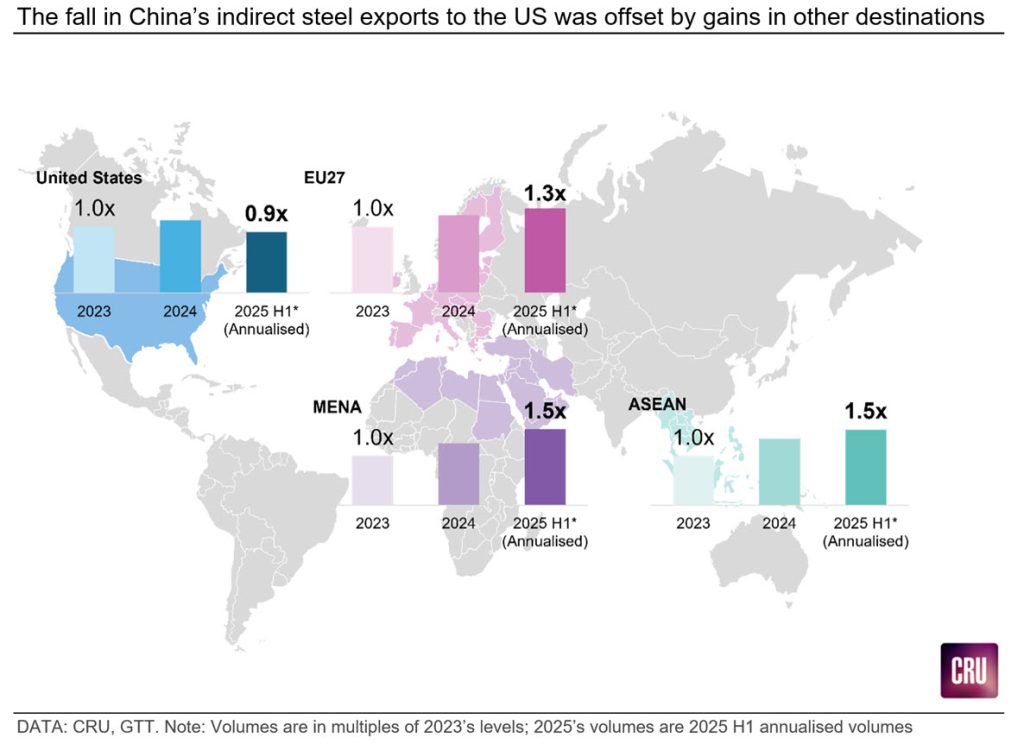

CRU estimates that the ASEAN region will absorb an additional 9 million mt of steel through imports of Chinese-manufactured goods in 2025 compared with 2023 (see chart below). This represents over 50% growth in just two years. In H1’25, Europe and MENA imported an additional 5 million mt of steel contained in manufactured goods compared with the same period in 2023. Most indirect steel exports from China into these regions are associated with the mechanical machinery sectors.

China’s indirect steel export volumes to the US increased in 2024 but will decline in 2025 due to the impact of new US trade tariffs on Chinese-manufactured products.

On Aug. 18, the US government expanded the scope of Section 232 tariffs by adding 407 derivative product categories, including automotive components, furniture, and domestic appliances. As the steel content of these goods is now subject to a 50% tariff, we expect that US imports of steel-containing goods from China will decrease further in H2’25. Further diversification of Chinese indirect exports of steel into non-US markets is expected.

Steel sheet producers in new destination markets face the biggest challenge from the growing presence of China. Chinese producers also face problems – the higher indirect exports of steel were not enough to offset the decline in domestic Chinese sheet demand in 2024 (see CRU’s Steel Sheet Market Outlook).

CRU’s Global Steel Trade Service is now tracking China’s indirect steel exports monthly. We will continue to monitor developments in the indirect steel trade and, in parallel, adjust our forecasts for steel demand in different markets as the situation evolves.

Please contact CRU if you want to know more about the CRU Global Steel Trade Service.