Analysis

October 21, 2025

Final Thoughts: Survey says edition

Written by David Schollaert

It’s a can-kicking race at its finest. And it’s been drawn out! Some are getting so good at it, they’re kicking cans and taking names.

All joking aside, if the current “kick-the-can” cycle has shown us anything, it is to remind us that demand is still king.

There’s a lot of noise that’s been surrounding the market. For starters, the government’s on holiday. Capacity’s playing musical chairs – Granite City’s “stop-start” and Algoma’s US shipments halt. Then there are fall outages (just a handful left), import cuts, and a sideways-to-down scrap market. And we can’t forget tariff uncertainty.

Any one of those items would be a key pricing driver in any prior market. And mills would be notifying customers of price hikes. Yet we haven’t seen that at all. While prices have fluctuated a bit here and there, they have been largely flat, hovering right around $800 per short ton since mid-August for hot band.

Contract demand is steady. Max volumes are being shipped, but the spot side is still failing to deliver. And most of you are telling us, there’s nothing yet on the horizon pointing to a key factor driving spot demand.

Survey says

And SMU’s latest steel market survey results note just that. Most market participants still think sheet prices are at or near a bottom. But most also believe there is limited upside once they inflect higher.

Survey respondents attribute the bottom (or anticipated bottom) mostly to limited import volumes and fall maintenance outages at domestic mills – factors that have constrained supply. But anemic demand means that the drop in supply isn’t expected to create any big waves in the market.

And even when lead times stretch into Q1 – which is typically a busier time for the steel market – few think it will be a major or lasting driver on prices.

Anyway, enough from me. Below are some highlights from our survey and comments from our survey respondents. If you’re a ‘premium’ subscriber, you can find the full results here. (The page numbers in the charts below indicate which slide in the survey deck they’re in.)

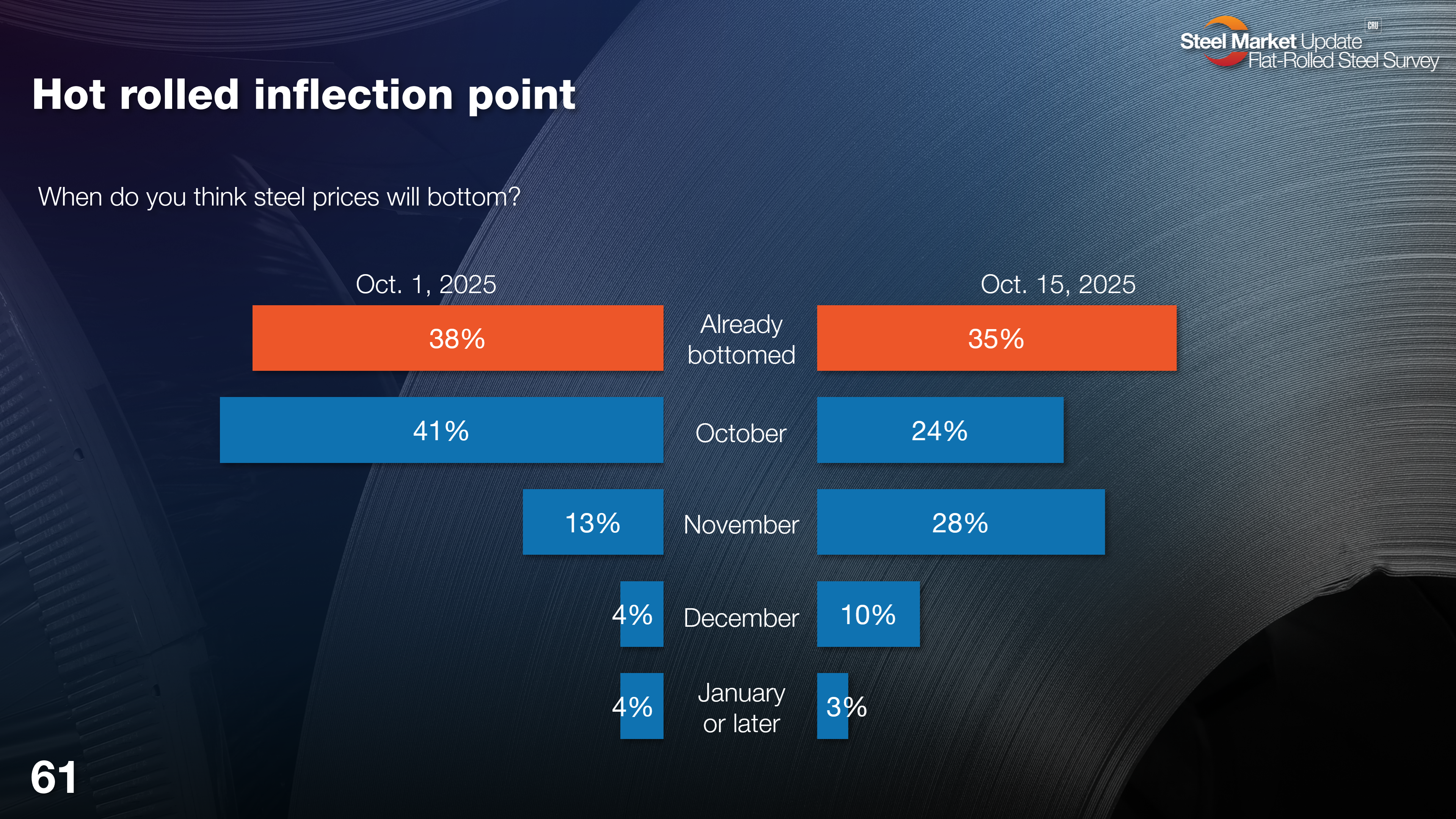

When is the bottom?

As you can see, most people think hot-rolled (HR) prices have already bottomed out or will later this month. I’m using HR as a proxy for the rest of the sheet market. If you think, for example, that cold-rolled and coated follow HR on a lag, then you’d want to adjust accordingly from the results below.

And here’s what some of our survey respondents had to say.

Already bottomed

“Market is soft but already priced out.”

“No imports, raw material costs bottoming out. Inventory moderate. Mill will try to increase prices now.”

“Seeing some stability, with a seasonal lull in place.”

“Seems like outages and higher contract order booking are enough to establish a bottom for the time being.”

October

“Demand is stable and inventories are stable.”

“I feel it will be within the next few weeks, with buyers coming back to purchase for some 2026 needs. I don’t feel that it will be a significant climb upward because supply still outpaces demand.”

“I feel more tariffs are coming that will allow domestics to raise prices.”

November

“Demand will remain challenged as long as the uncertainty of tariffs make near- to longer-term planning difficult.”

“Market will bottom out late October or early November. Looks like mills will sell out of hot roll in December before they close out December for galv.”

“Mills aren’t showing enough restraint.”

“Will start moving higher as lead times extend into 2026.”

December

“Demand decreases due to holidays.”

“Other than automotive, demand in other industries is slowing down to the point that the additional volume taken due to import replacements is not offsetting it.”

January or later

“I think we maybe see a slight uptick in November/December, but then pricing will erode again. Demand is just too bleak.”

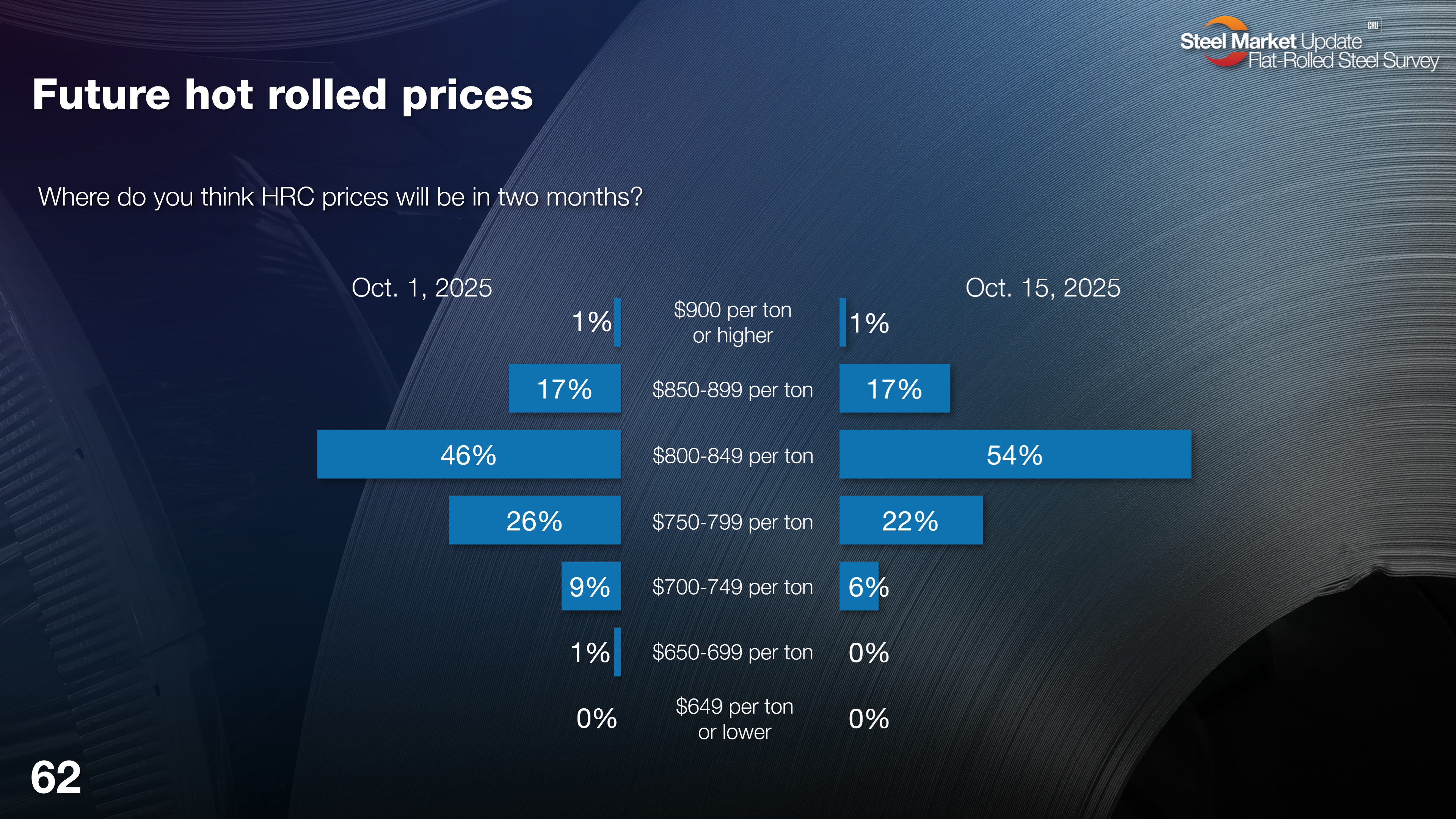

Where is the bottom?

And while there was a bit of a shift when it came to an inflection point timeline between our last two surveys, there was little change regarding where prices will be two months from now at the end of Q4. Most don’t expect the market to turn sharply anytime soon. But the jury’s still out on whether Q1’26 gets a replay of 2025.

Nearly three-quarters of surveyees (71% of respondents) think HR prices two months from now will be in the $800s/st. Keep in mind that by early December, most lead times should be into 2026. Still a few less (28%) now see ticking back down into the $700s/st. (SMU’s current HR price stands at $805/st on average, up $5/st vs. last week.)

Here is what survey respondents had to say.

$900/st or higher

“Prices are going up. Get your orders in.”

$850-899/st

“Less import, fewer players, Algoma, hopefully demand finally picks up, it’s long overdue.”

“Maybe wishful thinking, but I would think in two months, lead times are into the new year, and contract business will begin to be placed, and some level of restocking with falling imports will help mills push prices up.”

“More and or more solid tariffs.”

“Restocking, mill outages, and low import volumes, no change in trade dynamics for some time.”

$800-849/st

“Bottom will have been reached.”

“Low end, we are in a very stagnant economic situation with tariffs and uncertainty. Jobs numbers are horrible.”

“Mills are tired of losing money; planned and accelerated outages; inventories of cheaper steel are running out; interest rates will drop further, stimulating demand.”

“Some seasonal bump likely going into Q1.”

“Still no strong demand.”

“We’re close to the bottom. This has been a very long and drawn-out softening.”

$750-799/st

“Demand decreases due to holidays.”

“Demand is stable.”

“Demand will slow down towards December.”

“Maybe a slight bump up, followed by erosion. So we’ll be either where we’re at now or a bit lower.”

“Spot pricing is not at $795.”

$700-749/st

“Flooding of the global market with steel will keep domestic steel down.”

“Lack of demand – Interest rates need to come down.”

$650-699/st

And similar to our last survey, the small number of folks who think HR prices will drop back into $600s/st aren’t tipping their hand on why they think that.

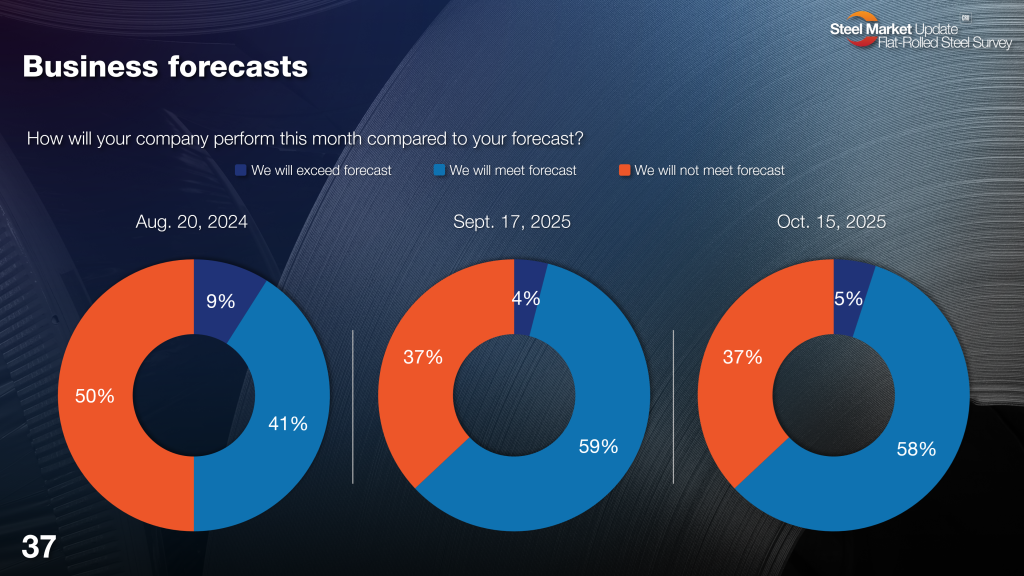

The woes of forecasting

The shift was clear when Section 232 tariffs were doubled to 50% in June. They were backed by a bit of seasonality, and the battle has been uphill since. We continue to see that many steel buyers aren’t meeting forecasts. It’s been a clear trend since late May.

But another wrinkle in the way to look at this data, especially since we continue to hear from many that they are downgrading forecasts, is that presently, just 5% of folks are exceeding their forecasts.

This tracks well with data underscoring a rather bearish spot market with little driving momentum to elevate forecasts.

Will not meet forecast

“Shipments and demand are down.”

“Too many trade barriers.”

“US tariffs on steel will affect our Mexican operation.”

Will meet forecast

“Remain conservative.”

“We’ve got a pretty solid backlog, so we’re fighting the good fight. Definitely tough out there, though.”

Editor’s note: The small number of those exceeding forecast are not giving us a peek behind the curtain on the pockets of demand that are driving growth and why they think that.

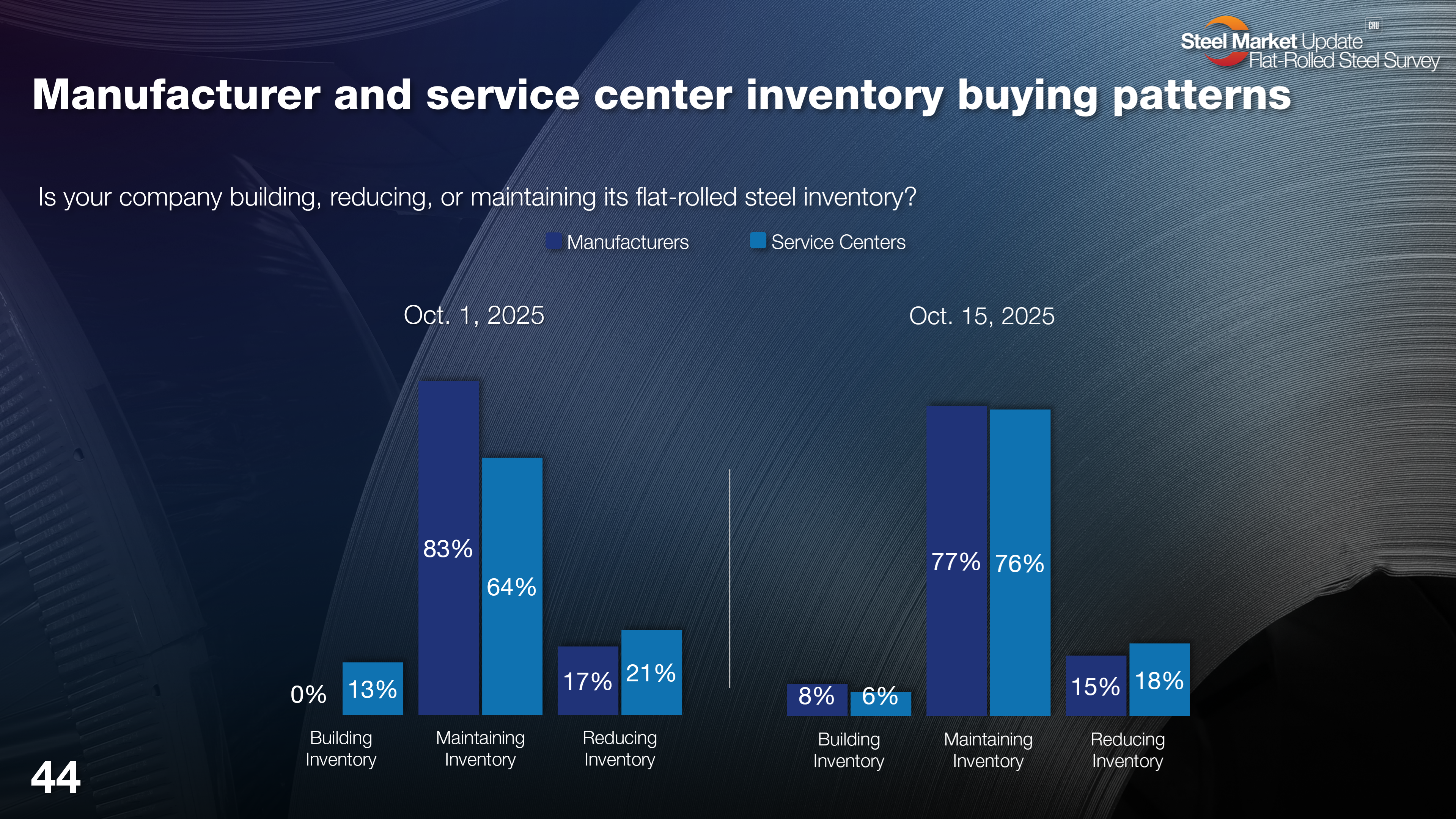

A word on inventories…

We released data on September service center inventories on Oct. 15 to our premium subscribers. US service centers flat-rolled steel supply edged lower for the second consecutive month.

And, according to our survey, a clear majority of steel buyers – both service centers and manufacturers – continue to either maintain or reduce inventories:

We do see some restocking among service center and OEM respondents, but still in a somewhat marginal volume. It will be interesting to see if this trend shifts at all as flat-rolled buyers position themselves in Q4 for early 2026 demand.

Tariffs have done their job

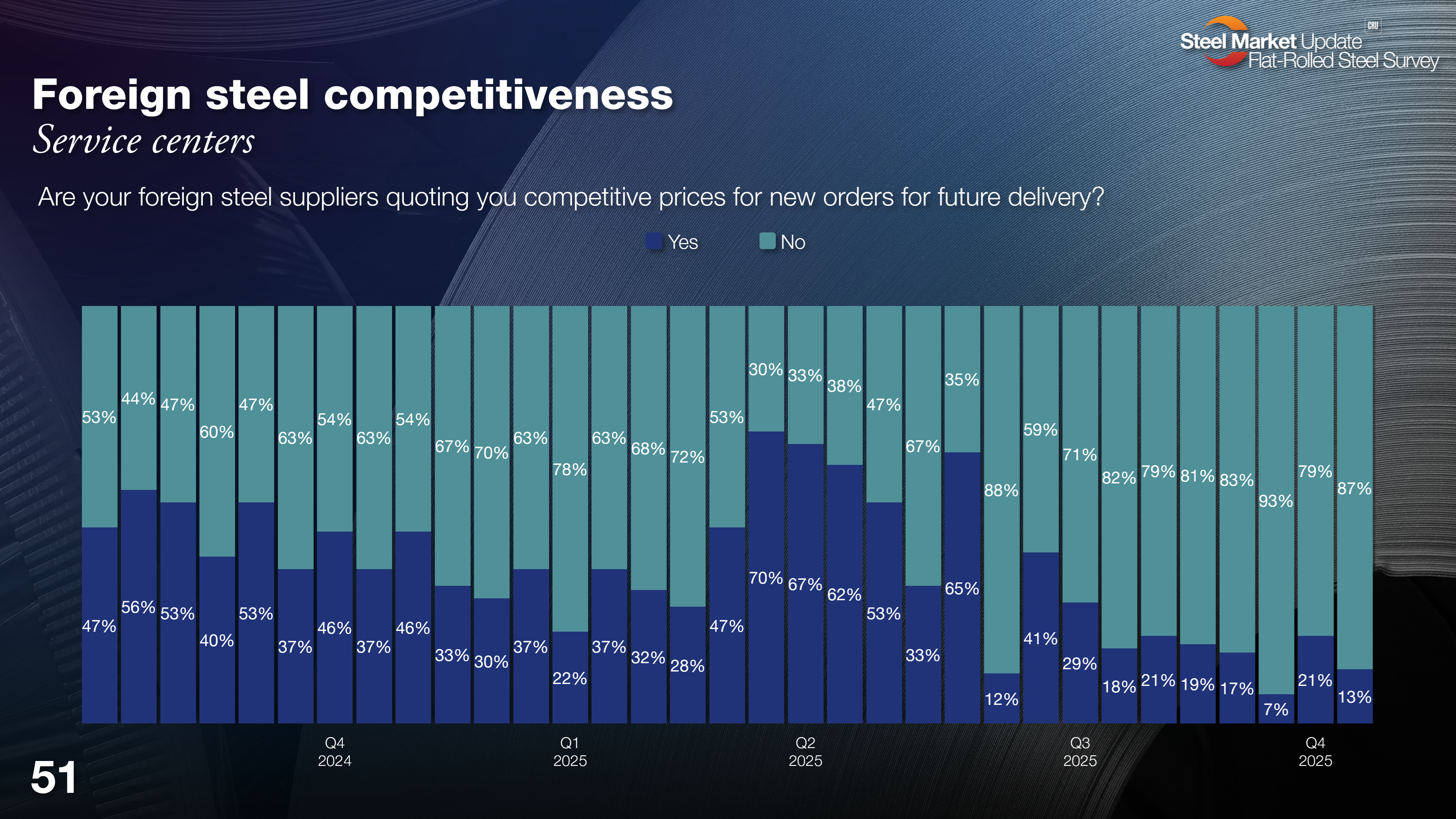

Evidence continues to point to declining imports. While the Commerce Department hasn’t updated import volumes due to the shutdown, recent data suggest finished steel imports might be down near some of the lowest totals in recent history. Look at the chart below. So it’s no surprise that nearly 90% of service center respondents say that imports aren’t competitive.

And numbers have been hovering around two-thirds or more since June, when Trump’s 50% Section 232 tariffs went into effect.

Meanwhile, most trading companies unanimously tell us that foreign steel isn’t attractive to US buyers.

Well, there you have it — just a few data points from our latest survey. Be sure to check it out. There’s a lot more very interesting data to look through.

And if you don’t have a premium-level membership, reach out to Luis Corona at luis.corona@crugroup.com, and he’ll set you up.

As always, we appreciate all your support.