Distributors/Service Centers

October 30, 2025

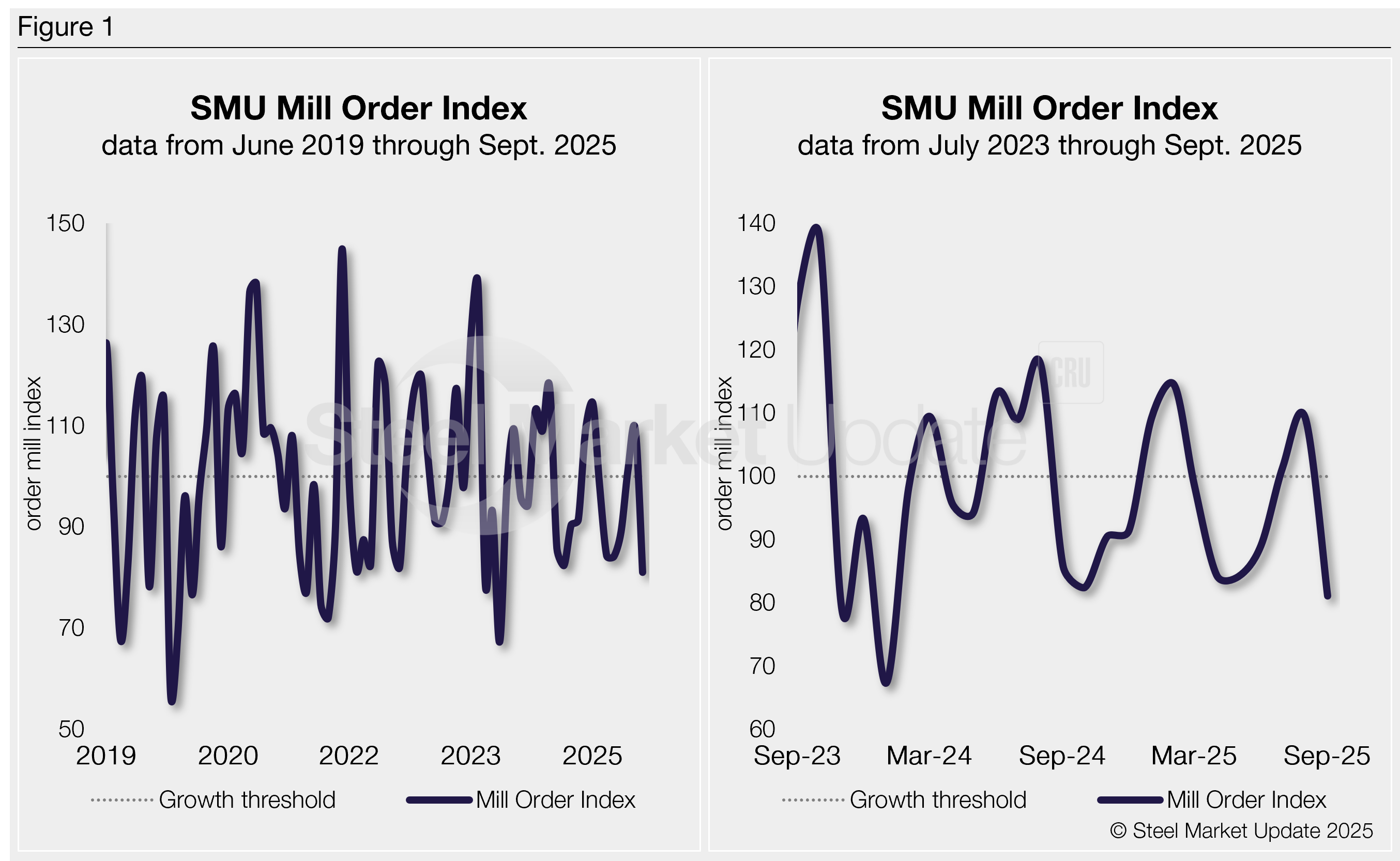

SMU Mill Order Index fell in September

Written by David Schollaert

SMU’s Mill Order Index (MOI) declined in September after repeated gains from June through August. The shift came as service center shipping rates and inventories both declined, according to our latest service center inventories data.

A reduction in intake and new order entries in September, though at a more aggressive rate, underscored the result. The cut comes as service centers remain mindful of rightsizing inventories. The moderate shipment levels and reduction in inventories put service center supply in balance with demand.

Downstream buyers remain cautious and buy mostly on an as-needed basis. This dynamic was highlighted as service centers’ daily shipping rate declined 4.1% from August to September.

The MOI now stands at 81.1, down nearly 30% from 109.3 in August. After closing in on February’s recent high of 114.5, September’s index is the lowest reading since January 2024.

Methodology

SMU derives its MOI — a relative index that evaluates the latest change in service center mill order entries — from our monthly service center inventories data. This index is a good indicator of current service center buying patterns, displaying perceived demand and lead times. This stands out because lead times typically signal upcoming moves in steel prices.

The MOI uses a base period, presently 2022-2024, to establish a reference point for measuring service centers’ mill orders over time. This base period is assigned an index value of 100. Subsequent MOI values are then calculated relative to this base.

An index score above 100 indicates an increase in buying, and a score below 100 indicates a decrease.

Figure 1 shows the nearly six-year history of the index on the left and provides a closer look at the MOI readings of the past two years on the right (100 = 2022-2024 average).

Background

After restocking in the second half of 2024, demand leveled off. The focus has since shifted sharply to inventory control.

Despite brief price spikes — driven by sudden price increases from mills backed by tariff news — market conditions have remained steady, at times sluggish, due to flat end-use demand (as shown in the right-side chart in Figure 1 above).

A rise in intake volume was reported for most of Q1, with a boost in buying from downstream customers pulling forward demand ahead of tariff-fueled price increases. A rapid rise in mill prices was triggered by the increase in service center orders.

The skinny

Intake has steadily tailed off after the tariff-driven buying surge fizzled out. With downstream buyers managing inventories and focused largely on maxing out contract orders, there’s been no spike in service center shipments, just a sharp decline in late Q3. SMU’s MOI could still edge up some, but most likely little variation in the near term, as service centers keep inventories in check and no downstream push for product, especially from the spot side.

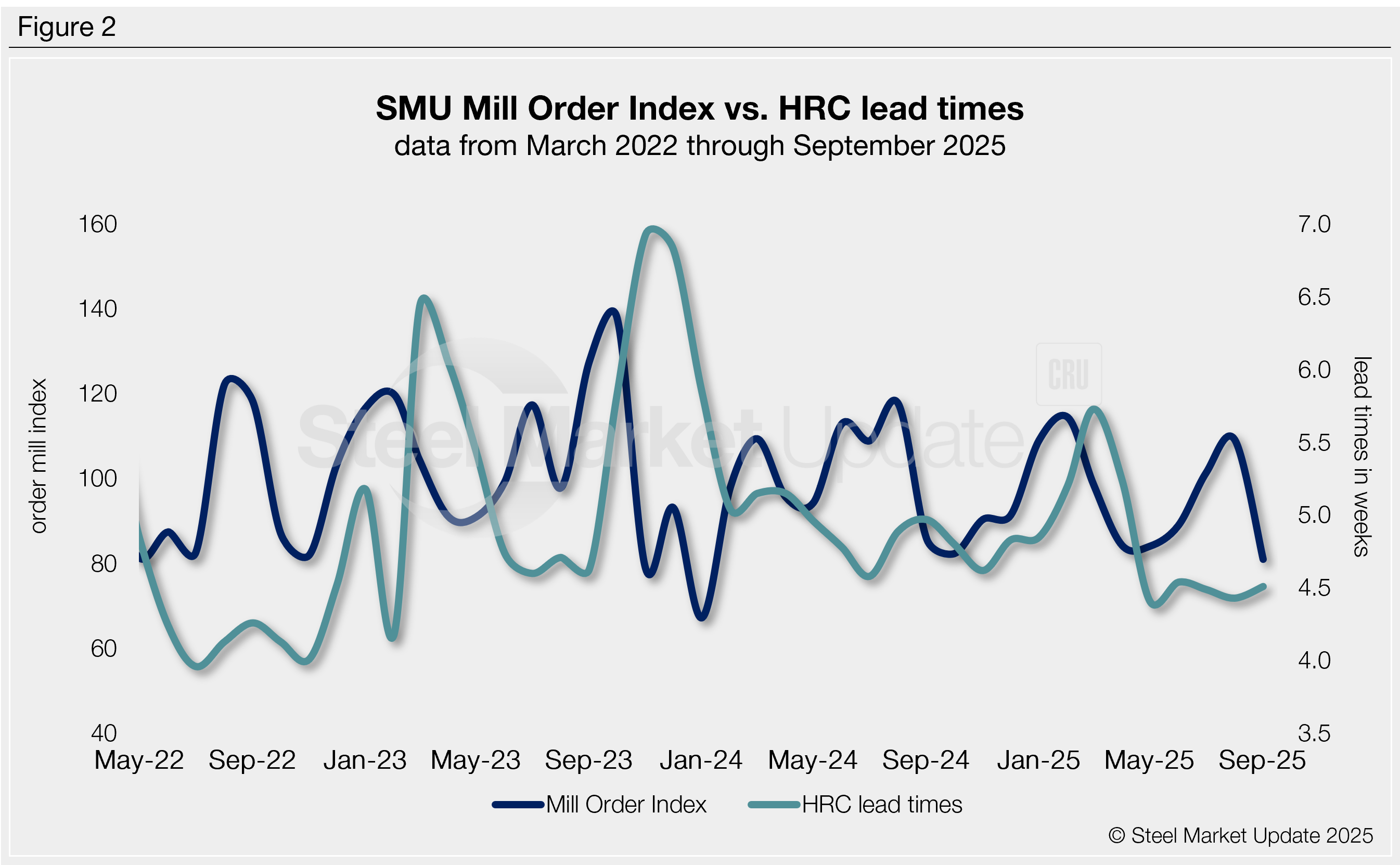

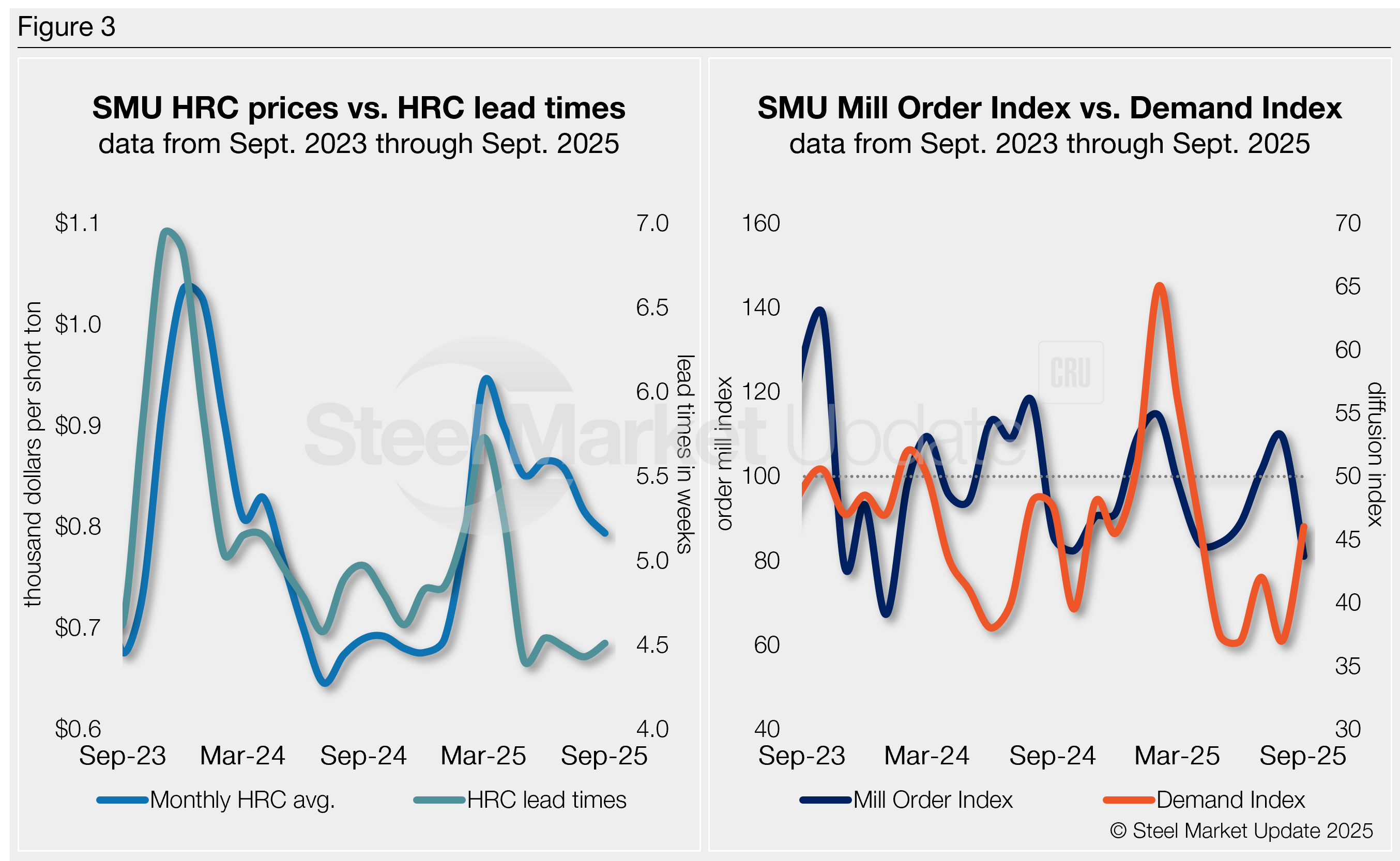

SMU’s MOI pairs well with — and has for the past five years proceeded — moves in mill lead times (Figure 2). And SMU’s lead times have also been a leading indicator of flat-rolled steel prices, particularly for HRC (see left-side chart in Figure 3).

Our MOI also pairs well with our Steel Demand Index (see right-side chart in Figure 3), which, for nearly a decade, has preceded moves in mill lead times.

Prices have been inching up in Q4 after a steady decline since May. Less mill discounting was followed by more outright price increases — including mill hike notices from NLMK USA and Nucor’s weekly CSP. The move is due largely to a continued supply squeeze with 50% Section 232 tariffs.

Will it last? It’s unclear, especially as the market nears a slower holiday period. Lead times have been edging higher ahead of the recent price increases, but moderate demand expectations need to shift higher as well.

And ongoing pricing uncertainty across markets might keep service centers focused on maintaining inventory levels.

Also, service center shipments will need to continue improving, which they haven’t in recent months. But if downstream inventories remain steady and buyers focus only on immediate needs, a significant shift in demand will be necessary to support stronger prices. Something some suggest we could see in the new year.

We’ll be tracking any changes closely as we move through Q4.

Editor’s Note

Order entries, demand, lead times, and prices are based on the average data from manufacturers and steel service centers who participate in SMU’s monthly inventories and every other week market trends analysis surveys. Our demand and lead times do not predict prices but are leading indicators of overall market dynamics and potential pricing dynamics. Look to your mill rep for actual lead times and prices.