Analysis

January 14, 2026

HRC vs. prime spread widens further in January

Written by Ethan Bernard & Stephen Miller

The price spread between domestic hot-rolled coil and prime scrap widened for a fourth consecutive month in January, based on SMU’s most recent pricing data.

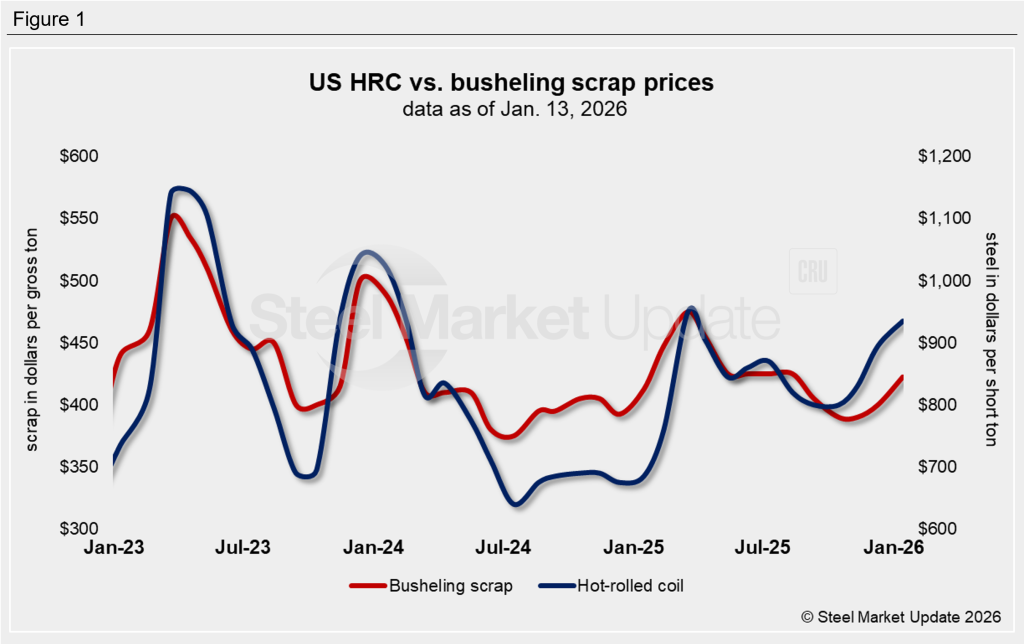

SMU’s average HRC price was $930 per short ton (st), FOB mill, east of the Rockies, as of Tuesday, Jan. 13. That’s up $5 from the previous week and a $25 jump from a month earlier.

Meanwhile, busheling tags in January rose $22.50 month over month to an average of $422.50 per gross ton (gt).

Figure 1 shows price histories for each product.

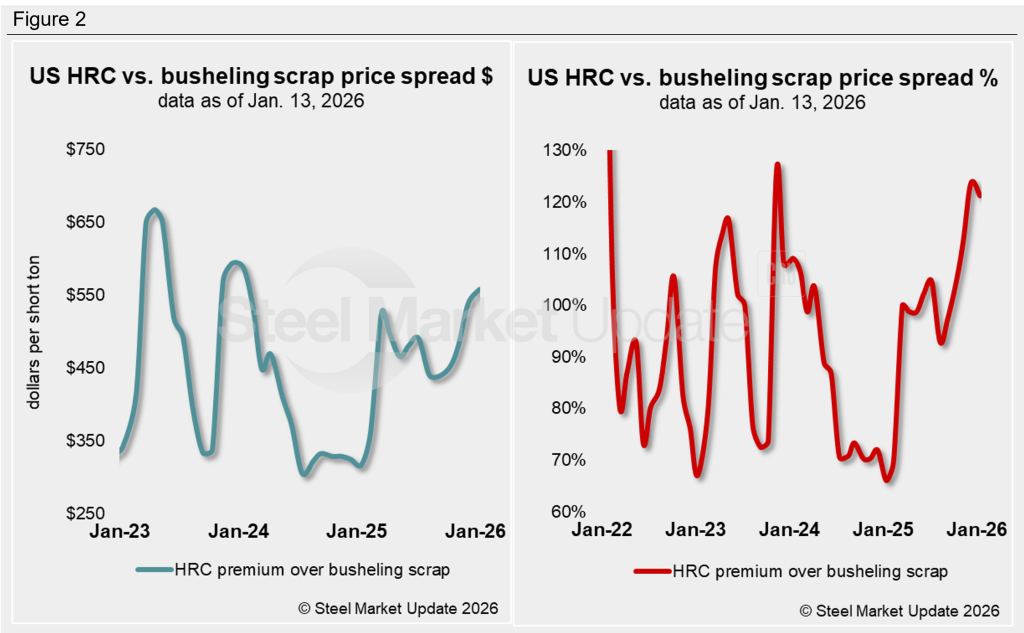

After converting scrap prices to dollars per short ton for an equal comparison, the differential between HRC and busheling scrap prices was $558/st as of Jan. 13. That’s an increase of $20/st from the prior month. Since September, the lowest the spread has been was $438/st as of Sept. 11 of last year (Figure 2).

What’s going on?

This spread has widened a bit, mainly because # 1 busheling did not increase as much as obsolete grades of scrap. This, coupled with increased optimism about demand for HRC, contributed to the increase as the HRC price elevated.

HRC premium as a percentage

The graph on the right-hand side of Figure 2 shows the spread relationship differently: We have graphed HRC’s premium over busheling scrap as a percentage. HRC prices now have a 121% premium over prime scrap, down from 124% a month ago.

Ethan Bernard

Read more from Ethan Bernard