Analysis

February 6, 2026

CRU: US, Mexico longs prices continue to rise while Brazil demand lags

Written by Alexandra Anderson

US rebar and wire rod prices rose month on month (m/m) alongside continued scrap increases, while merchant bar and structurals were unchanged.

End-use consumption remained seasonally low, although reduced import volumes kept mills fully booked. Furthermore, uncertainty surrounding trade policy is still a concern among market participants ahead of the USMCA renegotiation in July.

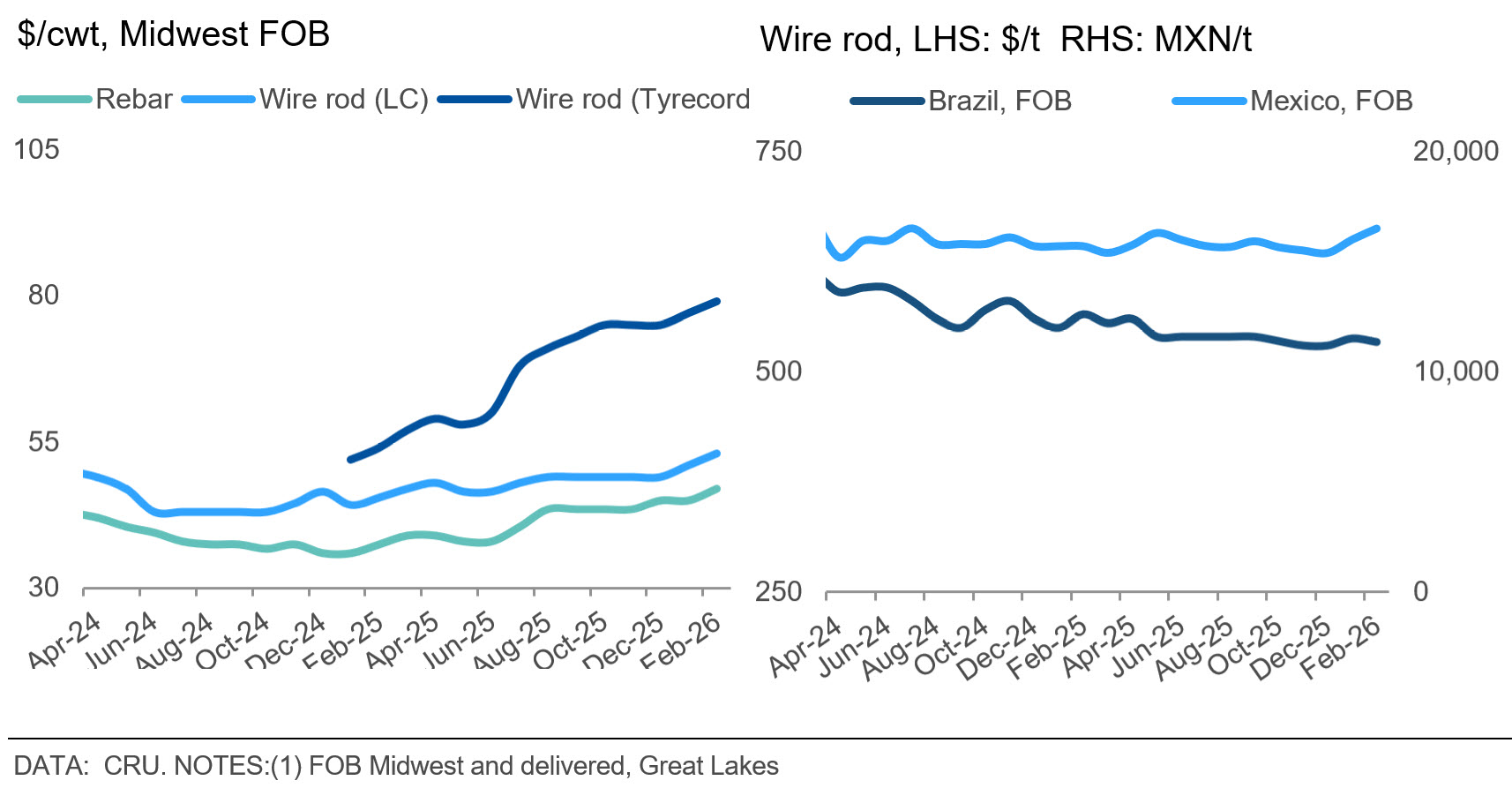

Prices for US rebar rose $2 per hundredweight (cwt) on further rises in scrap. Sources noted that downstream fabricator margins are squeezed because they have not been able to increase prices to end users to the same degree that mills have increased steel prices. That is despite some support from data center construction, although traditional construction demand is low.

Import volumes are down significantly year on year (y/y). However, a widening delta between import offers and domestic prices is starting to draw buyer attention, and further price increases could open the door for higher import volumes.

Wire rod also increased $2.00-2.50/cwt, depending on grade, this month as domestic supply availability stays tight, imports remained low, and scrap prices continued to edge higher.

Demand was seasonably stable for low-carbon (LC) wire rod, while high-carbon (HC) and tyrecord are seeing more upward pressure from end-use consumption. HC wire rod has benefited from data center construction and infrastructure, and a recovery in the auto sector has market participants optimistic about late Q1 demand.

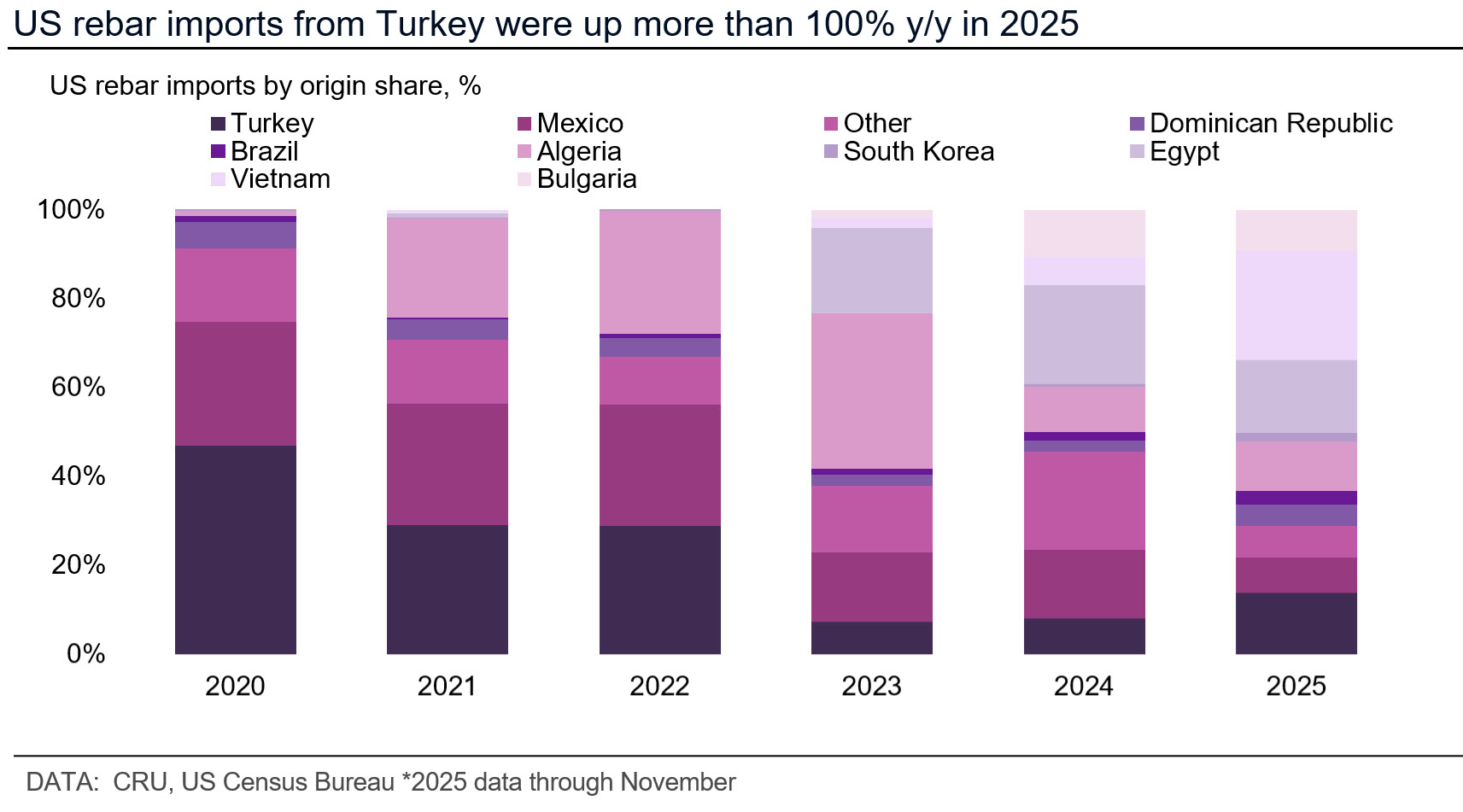

Total long product imports for Q4 were down ~55% y/y. Rebar imports were down ~24% y/y in Q4, while wire rod imports fell ~27% y/y.

Trade policy remains uncertain given the upcoming USMCA review this summer, during which the US, Mexico, and Canada rework their trade framework, as well as recent threats of increased tariffs. Furthermore, the ongoing trade case against rebar from Algeria, Egypt, Bulgaria, and Vietnam has shifted the mix of import origins, given the dominance of these countries as import suppliers over the last couple of years. As a result, imports from Turkey are at their highest level since 2022. Volumes from Turkey declined starting in 2023 alongside trade case reviews and overall fewer exports from the country.

In Mexico, long prices increased m/m as domestic mills increased prices. Mills are trying to increase prices even though end-use demand remained weak, as domestic supply remains tight, as one mill recovers from production issues.

In Brazil, domestic long demand continues to be weak. According to IABr, longs production decreased by 41.8% m/m in December, ending last year with a production volume down by 2.3% y/y.

Meanwhile, GECEX, the Executive Management Committee of the Foreign Trade Chamber, increased import duties for several steel products from February for 12 months. The list includes two categories of wire rod, which will have their import duties increase from 10.8%-12.6% to 25%.

These two categories were not previously included in the temporary import quota, and category 7227.90.00, accounted for 22% of all wire rod imported in 2025.