Analysis

February 12, 2026

HR Futures: Market holding steady as prices firm

Written by Gaby Ain

The most notable development since my last column has been how little has changed. That stability, however, may be the point. Prices have firmed and held, and the defining feature has been follow-through. A narrow range has emerged, suggesting the market’s repricing of downside risk is starting to stick.

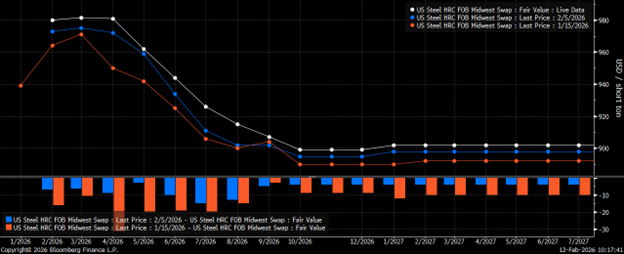

Looking at the curve’s evolution over the past month, what stands out is strength in nearby months has been absorbed rather than rejected, suggesting tighter physical conditions are being accepted rather than dismissed.

The most notable change has been the belly of the curve. Since January (orange), the market has largely stopped trying to price a summer collapse. While some easing may still be expected, the curve is no longer expressing confidence a meaningful break is inevitable. Seasonal relief, imports, and mill behavior might be no longer assumed to overwhelm the market.

Further out, deferred contracts into late-2026 and 2027 have edged higher, flattening into a band around ~$900 with no clear attempt to reprice a return to pre-2025 lows. The back end appears increasingly anchored by structural considerations such as trade friction, cost structures, and supply discipline rather than seasonal noise. The curve is simply less dismissive of the fundamental backdrop.

This rally also differs from prior cycles. Unlike past moves that, considering recency bias, often unfolded quickly and aggressively, this rally has developed at a much slower pace, with smaller dollar gains and fewer abrupt dislocations. This dynamic could suggest corrections, if/when they occur, may be shallower and better supported than in previous episodes.

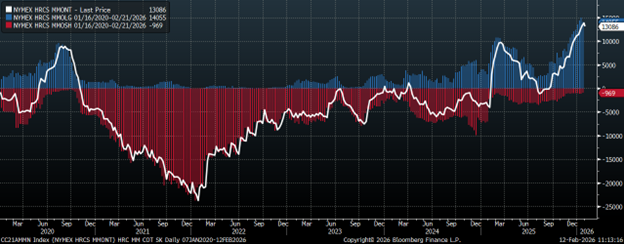

Positioning data provides additional context. Since 2021, money managers have carried a persistent net short bias, with length typically short-lived even during rallies. Current positioning breaks from that pattern. Net length is now the largest and most sustained in years. That helps explain why the curve has re-anchored higher and why downside expectations have softened, furthering implications of why correction could look different this cycle. While elevated length introduces vulnerability if conditions change, the recent modest reduction in length appears to be profit-taking driven rather than renewed bearish conviction.

That said, stability at these levels has rarely proven permanent. There are still many factors in play. Domestic production recently ramped up, and lead times, while still elevated, may be losing momentum as prices approach a psychologically important threshold near $1,000 amid lingering disbelief. Profit margins appear sufficient, which can reduce the incentive to chase volume even as demand remains uneven, though not necessarily deteriorating. With positioning still extended and uncertainty around tariffs and spring outages ahead, the surface may look calm, but volatility may not be far behind.

Disclaimer

The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed by Flack Global Metals or Flack Capital Markets should not be treated as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his opinion. Views and forecasts expressed are as of date indicated, are subject to change without notice, may not come to be and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.