Analysis

February 27, 2026

CRU: Tin hits a record high

Written by CRU

This news item was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.

Entering 2026, tin has led a frenzied base metal rally during a historic phase for commodities. Frothy market conditions, driven by volatile investor positioning and shifting macro risk sentiment, pushed several metals—including tin—to record highs in January, before a sharp correction in February.

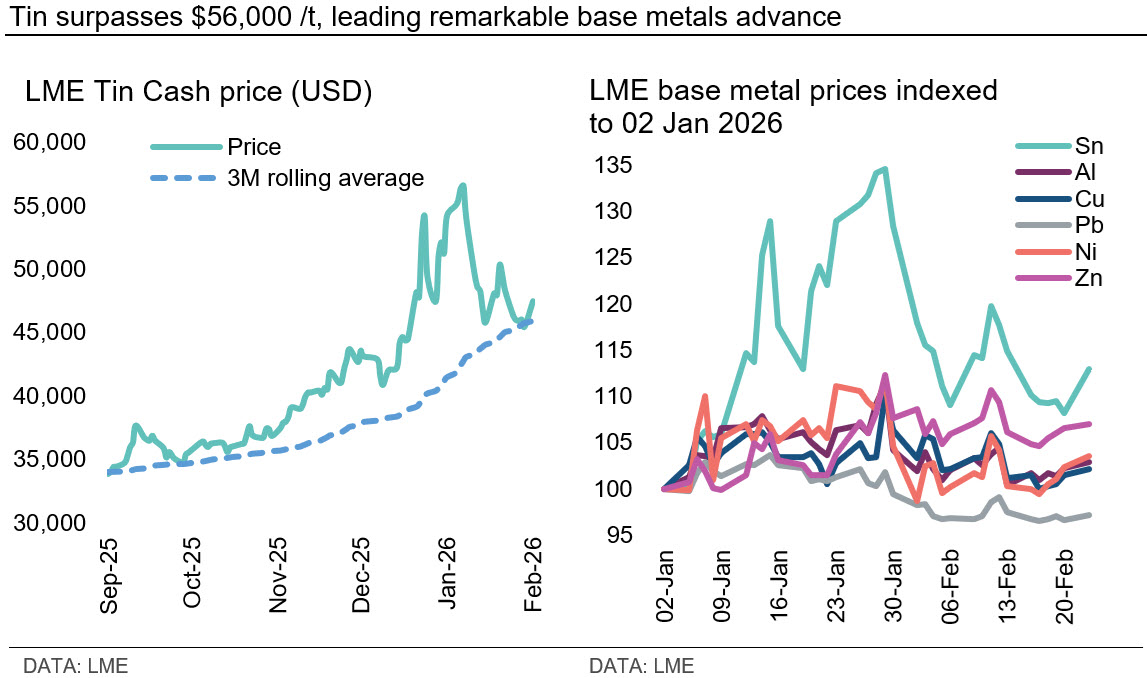

- Tin surged to successive record highs above $50,000 per metric ton (mt) in January, as prices appear increasingly disconnected from fundamentals.

- Financial flows—particularly from Chinese investors—have dominated short-term price formation, with extreme SHFE volumes and aggressive positioning shaping the rally and subsequent correction.

- Influenced by elevated prices, visible exchange inventories have more than doubled over the past three months, signaling no physical shortage despite a tight supply narrative underpinning speculative interest. A survey of tin consumers indicates the recent price spike has dampened tin use forecasts for 2026.

- While risks remain, supply-side pressures look set to ease in the months ahead, as concentrate shipments from Myanmar to China stabilize at improved levels. However, some disruption to Indonesian exports stemming from RKAB changes should be anticipated in Q2.

- In a potentially significant policy development, the Trump administration launched a critical minerals stockpile earlier this month, as efforts by the world’s second-largest tin consumer to secure future supply continue.

Fundamentals take a backseat as prices soar

It’s been quite a start to the year for metals and tin. The broadening of the precious metals rally into base metals—which kicked off in Q4 last year—has been turbocharged heading into 2026.

Both tin and copper hit record highs in January while gold and silver continued to soar. This performance has not been driven by fundamentals, though, with macroeconomic uncertainty instead pushing investor allocations toward safe-haven and physical assets amid heightened geopolitical tensions, including those surrounding Venezuela, Greenland, and most recently Iran.

Looking back to 2025, tin led the complex nearly all year but was narrowly pipped by copper to the mantle of best-performing base metal on the final trading day. The ‘spice metal’ concluded 2025 at $40,850/mt, up 40.3%. Entering 2026, tin has resumed its position as the leading base metal, in what has proved an incredibly tumultuous opening to the year.

Tin prices set a record high of $53,462/mt on Jan. 14, correcting briefly, before rallying to another record of $56,816/mt on Jan. 23, supported by US dollar weakness, a resurgence of debasement trading, and frenzied activity from Chinese investors.

The US dollar slumped to a four-year low on Jan. 27, but strengthened on Jan. 30, as president Trump nominated Kevin Warsh for the next chair of the Federal Reserve, generally seen as a hawkish pick. A wild day of trading ensued, triggering a broad retreat by precious and base metals.

Tin corrected sharply into February, falling 15.4% over two days to close at $46,591/mt on Feb. 2.

In line with the rest of the base metal complex, tin has entered a steadier phase in recent weeks, supported by cooling speculative volatility and subdued Chinese market activity around the Lunar New Year. A bounce in tin prices is expected as Chinese traders return from the Spring Festival break.

Frenzied investor activity spurs historic rally

Fundamentals have taken a backseat of late as geopolitics and investor activity dominate the market direction. Though recent moves have been more exaggerated, as is customary for tin, it has followed the same pattern as other base metals, generally trading on the macro and news flow.

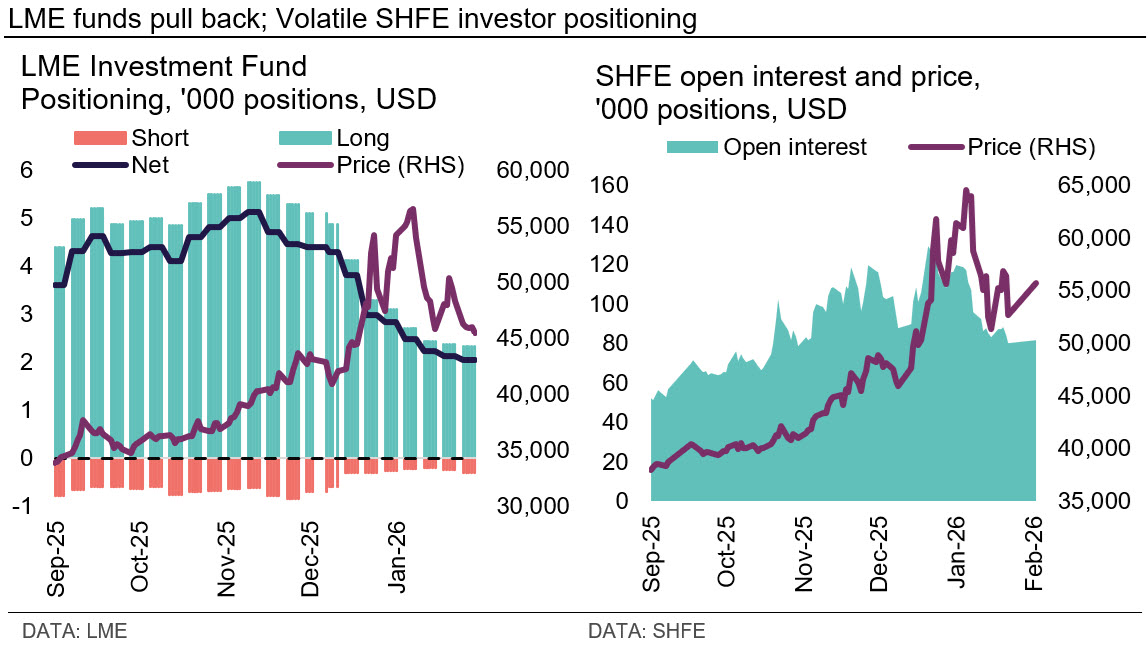

Discussed extensively last year, financial flows are playing an increasingly important role in short-term price formation, with Chinese investors, in particular, responsible for driving prices higher in the new year.

SHFE tin trading in January was marked by exceptionally heavy volumes and volatile positioning. Open interest rose sharply in early January, signaling fresh speculative participation, before peaking mid-month alongside a surge in trading activity. Daily volumes exceeded one million contracts on Jan. 15—equivalent to nearly three times the size of the annual physical tin market.

Accompanying the rally to record prices, consecutive limit-ups were reached on the SHFE, prompting the exchange to adjust the daily price limit for tin futures from 8% to 11%. The SHFE also moved to restrict the activity of a select group of clients (for ownership rule breaches), potentially contributing to the subsequent cooling.

Similarly, following the historic declines witnessed at the end of January, several other exchanges acted to safeguard against heightened volatility, with CME Group raising margin requirements for gold and silver futures.

In contrast to the explosive interest on the SHFE, LME net fund positions have shortened for ten consecutive weeks, to just above 2,000 contracts long. The end of January and early February also saw sustained position liquidation on the SHFE, pointing to aggressive profit-taking and a loss of momentum following an overheated rally.

For tin prices, sideways trading is expected to remain the prevailing near-term trend.

Exchange inventories build and AI jitters

Elevated prices have dampened downstream purchasing and spot market activity. The risk of demand destruction at current price levels has been widely discussed in the copper market. In response, a survey of the ITA’s tin use study group confirms that the recent price spike has weakened 2026 tin use forecasts and disrupted purchasing behavior, with some consumers flagging the need to revise annual budgets.

Substitution risks are also being highlighted in certain end-use sectors, although tin continues to benefit from relatively inelastic demand in solder applications.

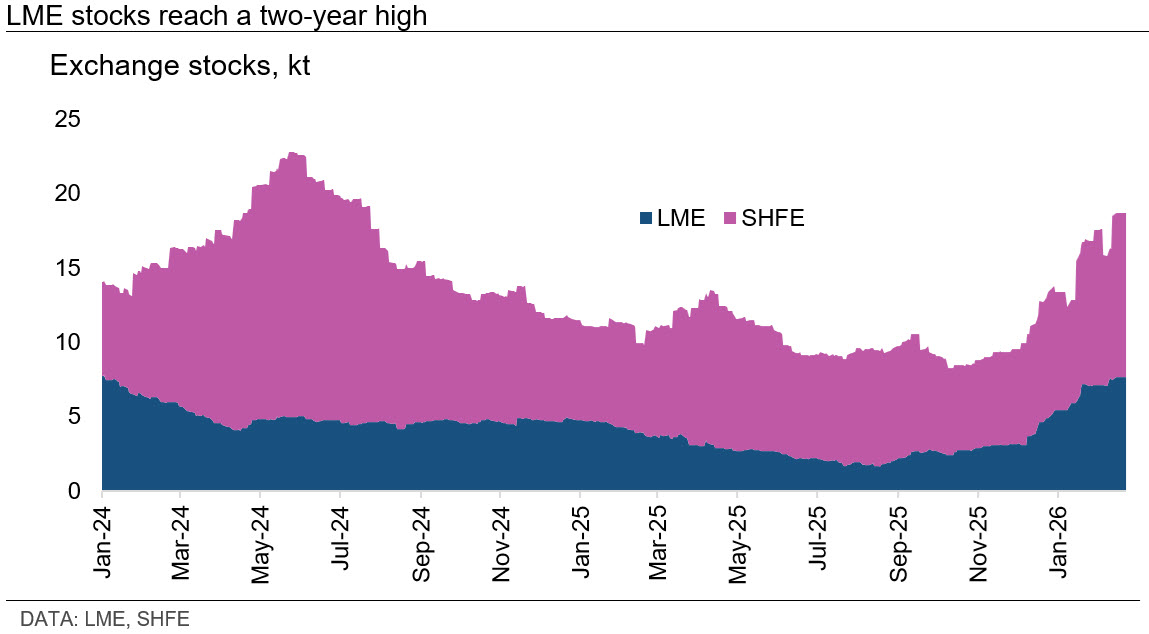

Despite a tight supply narrative underpinning much of the recent speculative interest, tin remains readily available in the physical market. This is evidenced by the rapid build-up of visible exchange stocks, which have more than doubled over the past three months, reaching 18,670 mt as of Feb. 20. While higher prices have clearly incentivized increased deliveries to exchanges, the scale of the stock build suggests no immediate physical shortage.

For context, when tin prices last reached comparable levels in 2021, exchange stocks stood at just 2,000–3,000 mt. LME inventories are now at a two-year high, above 7,000 mt, with inflows dominated by deliveries into Hong Kong and Singapore.

The structural demand case linked to AI continues to be supportive of tin. Bullish announcements on AI-related expenditure, alongside strong earnings reports from US companies involved in data-center buildouts, likely also contributed to recent price strength.

While February has been marked by a selloff in US equities on renewed AI disruption scares, the theme will likely remain a meaningful bullish driver in the medium to longer term. According to SIA, global semiconductor sales increased 25.6% in 2025 with a similar growth forecast for 2026, approaching $1 trillion in value.

Turning to China, despite a recent slowdown in the domestic PV sector, the planned cancellation of tax rebates for PV and battery products from April 1 may front-load and support demand in Q1.

Beyond this, and in the absence of a clearly defined new stimulus package, Chinese demand is expected to remain broadly flat in 2026, characterized by ongoing structural adjustments rather than outright growth.

US strategic stockpiling to return

The long-awaited outcome of the Section 232 critical minerals investigation came in January, with Trump deciding, for now, against imposing tariffs. However, in line with our December editorial forecasting a return to strategic stockpiling, the administration launched a $12 billion critical minerals reserve—Project Vault—on Feb. 2, which is understood to cover tin.

Shortly thereafter, UK-based tin developer Cornish Metals received a letter of interest from the US Export-Import Bank (EXIM) for up to $225 million in financing to restart the historic South Crofty tin project. The potential financing is conditional on the mine supplying ‘responsible’ tin concentrate to the United States, underscoring the US government’s growing foray into the tin sector.

This follows EXIM issuing a letter of interest to fellow UK-based developer First Tin in November, as well as progress by leading US secondary tin producer Nathan Trotter to secure feedstock for its new primary tin smelter currently under construction.

Having let the Defense Logistics Agency (DLA) tin stockpile decline from over 120,000 mt in 1995 to less than 4,000 mt today, it is evident that the world’s second-largest consumer of tin is intensifying efforts to secure future supply. However, in the absence of domestic primary production in the US, alongside stringent ESG and responsible sourcing requirements and a limited pipeline of new global supply projects, such efforts are unlikely to be straightforward.

Supply pressures begin to ease

Despite recent price performance, signs of a gradual recovery on the supply side are emerging.

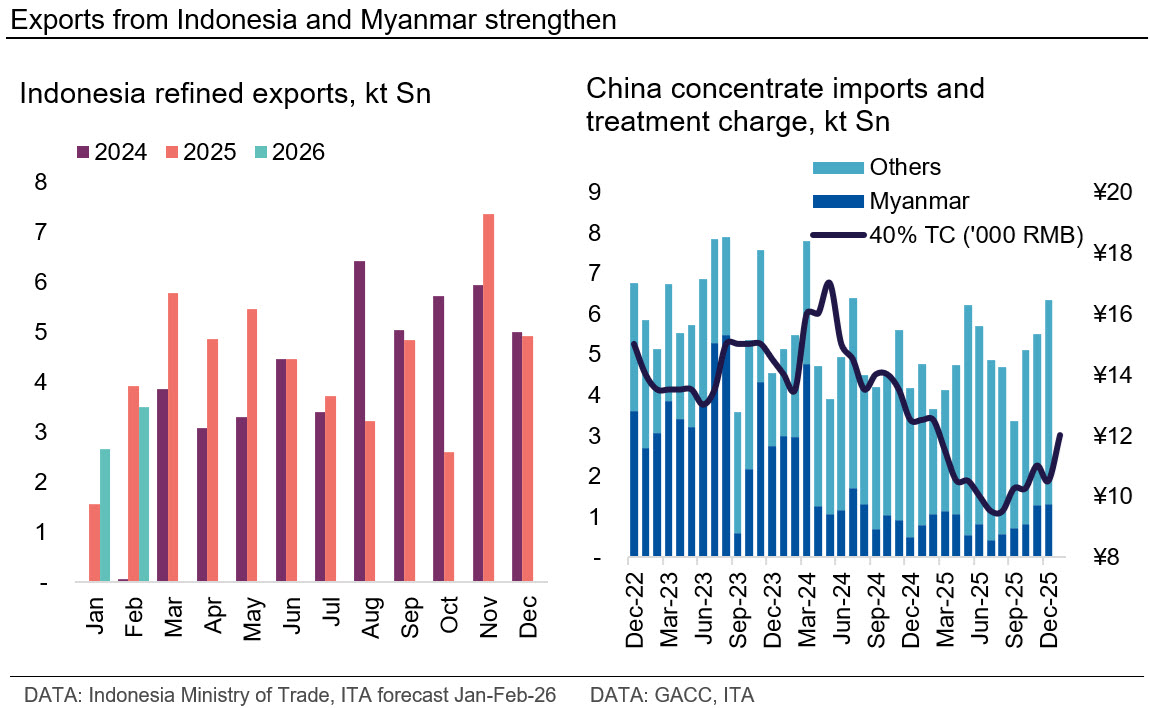

Although later than expected, refined shipments from Indonesia resumed following the customary New Year-related delays to export permits. Trading on the JFX restarted on Jan. 21, with monthly volumes totaling 2,670 mt, up 68% y/y and notably strong for January, extending the momentum seen toward the end of last year.

In line with our expectations, Indonesian exports in 2025 totaled 52,300 mt, rebounding from 45,700 mt in 2024. Looking ahead, the Indonesian Tin Exporters Association (AETI) has indicated that the 2026 production quota will be set at around 60,000 mt, while PT Timah has confirmed a production target of 30,000 mt for the year.

The recovery in Indonesian supply, therefore, appears set to continue, although output is expected to remain below 2022–2023 levels. A key risk to monitor is potential disruption in Q2 stemming from the RKAB changes, which could trigger renewed price strength and speculative support.

Meanwhile, production in Myanmar has finally shown signs of improvement, with tin-in-concentrate shipments to China stabilizing at around 1,300 mt over the past two months, up from a monthly average of 630 mt between May and October 2025.

However, this recovery remains insufficient to ease raw material tightness in China, as flooding in the deeper, higher-grade sections of the Man Maw mining complex remains unresolved, with remediation not expected until after the Lunar New Year. Under an optimistic scenario, Myanmar output could exceed 20,000 mt of contained tin, still only around half of pre-suspension levels.

Turning to the DRC, rising speculation about escalating unrest in the country’s east re-emerged as a primary driver of the price rally toward the end of 2025. Alphamin has so far avoided a second shutdown at the Bisie mine, despite rebel advances beyond strategic towns that triggered last February’s suspension.

Although the Congolese authorities and M23 have signed a document outlining the terms of reference for a ceasefire, with talks being mediated by Qatar, we remain skeptical of its effectiveness.

The ongoing conflict continues to pose a significant supply risk for 2026, with recent reports suggesting limited de-escalation in fighting despite the signing of peace agreements between the DRC and Rwanda last year. Nevertheless, if Alphamin’s operations remain unaffected, DRC mine output could increase to around 30,00 mt of tin-in-concentrate in 2026.

Beyond these developments, there has been no fresh supply-side news to justify recent price action, with prices at such elevated levels appearing unsupported by fundamentals or the cost of production.

Have prices overshot?

At present, the prevailing view in the tin market is that prices are unsustainably elevated. While it may be premature to declare a definitive peak in the broader base metals rally, the sharp intraday reversals observed at the end of January suggest this may have already been reached.

Speculative positioning—particularly in China—remains central to near-term price dynamics. A cooling macro risk environment could allow fundamentals to reassert themselves; however, heightened volatility is likely to persist, especially amid ongoing US–Iran tensions and renewed tariff uncertainty following the recent US Supreme Court ruling.

From a fundamental perspective, although risks remain, we anticipate some softening in the months ahead. Against this backdrop, alongside rising exchange inventories and a shortening in LME net fund positions, tin prices are expected to trend lower over the medium term.