Analysis

May 17, 2026

Final Thoughts: Stronger for longer still in effect

Written by Michael Cowden

SMU released its latest flat-rolled steel market survey results on Friday. The main takeaway: the stronger for longer narrative is still very much in the house.

Another one: We’re finally starting to see evidence of a broader-based restock among service centers, maybe even a historic one – if they can find the tons, that is. You might say that’s risky if you think prices are near a peak. But it’s also overdue.

Service center’s sheet inventories are at their lowest levels since May 2021, according to the latest SMU figures. And with lead times still extended, some might run a real risk of trying to sell from an empty cupboard. (The most expensive steel is the steel you don’t have.)

And, finally, we continue to see some of the stronger demand readings seen since the post-pandemic boom. Forty-four percent of survey respondents reported improving demand, the highest reading since June 2021, according to our records. And that’s despite (justified) concerns about the Iran war and the long-term impact of inflation.

Editor’s note: You can click on all of the images below to expand them. The page numbers show where in the full survey deck you can find them. Our premium subscribers can access that deck here.

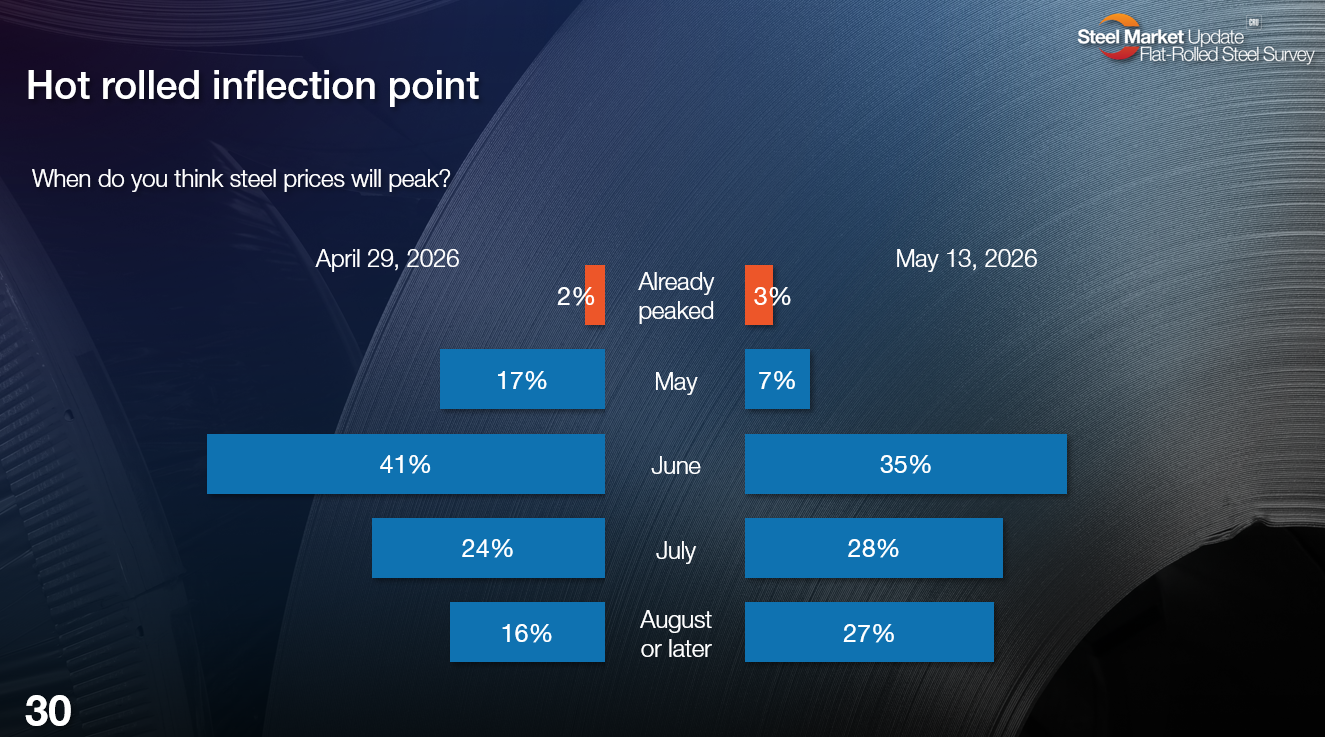

Let’s start with prices

Before we get into specific numbers, let’s look at when people think hot-rolled (HR) coil prices—and, by proxy, sheet prices in general—will peak.

The most common response is that prices will peak in June. That’s a trend we’ve seen since the beginning of the year. People say that prices will peak next month. And then when next month arrives, they say prices will peak the following month.

What’s new this time is the number of people who think prices will continue to rise into August. In other words, more people believe in the durability of this rally than was the case at the beginning of the year.

Here is what some of our survey respondents had to say in their own words.

May

“There is not enough demand. Prices cannot remain this high.”

June

“Seasonal pause and price shock pushback.”

“Iran war will increase raw costs for mills. But demand is slowing down due to cost pressures.”

“Prices are high enough where some import tons will get into the market. And if there is a USMCA agreement to allow Canadian and Mexican tons into the US without tariffs or reduced tariffs.”

“We’re close to the peak.”

“Market just keeps moving out.”

“The demand is still strong. Maybe it will cool down for summer. But who knows now.”

“I’m on the West Coast, and I don’t have enough insight into demand to understand why prices keep going up.”

“I was totally wrong about this rally. It was certainly supply-driven for a while, but here comes demand now!”

July

“Should stop climbing by mid-summer. But who knows.”

“When the war with Iran is over.”

“Mill backlogs should be cleared by July allowing more spot quoting to happen.”

“Demand is continuing to increase.”

August or later

“Demand is still the key factor. Inventory levels are dangerously low. Nothing to stop the upward movement right now.”

“Due to the strong backlogs at the mills. If the ‘summer doldrums’ occur, that might only bring in the lead times. But then demand will start to increase, and lead times should start to extend again. Therefore, pricing should remain steady or keep gradually increasing well into Q3.”

“Prices have more room to increase. Supply will continue to remain tight and demand will increase.”

“Nothing to really stop the mills from raising prices.”

“Even with imports (primarily from Asia?) coming in, I’m hearing/reading that this rally may last longer than expected and go into August.”

“Demand is increasing, so pricing is going to go up.”

“As the manufacturing increases, the demand will increase.”

“All the futures are still trading high.”

“Tariffs, lack of imports, and mill maintenance.”

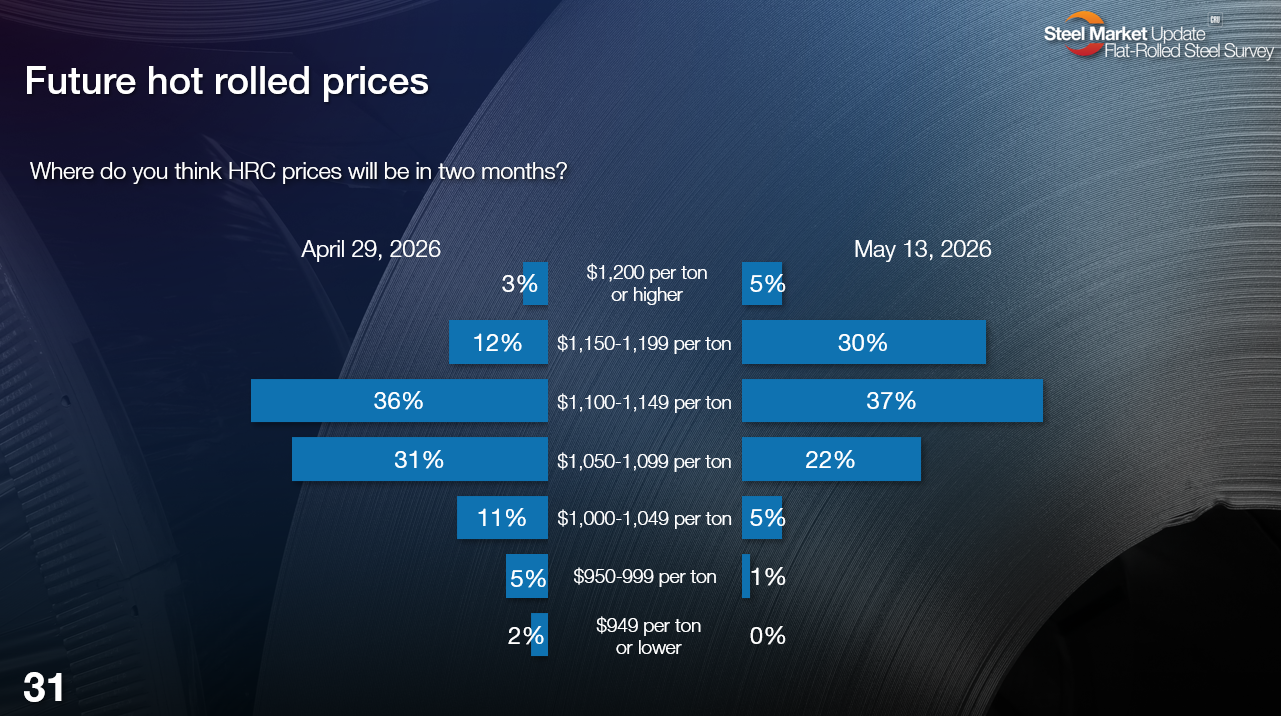

The crystal ball

Another question we always ask: Where do people think HR prices will be in two months? Below are the latest results.

Notice a pattern? We keep rolling when we think the market will peak from one month to the next. Similarly, we continue to nudge price expectations higher from one survey to the next.

The market is now assuming that prices will go above $1,100 per short ton (st). Namely, 73% of respondents think we’ll breach that level. What’s notable is 30% now think we’ll go above $1,150 – something that was a minority view just two weeks ago.

That said, I can see the logic. In mid-March, SMU’s HR price stood at $1,005/st on average. It now stands at $1,080/st. That amounts to a gain of $9.375/st per week. Multiply that by eight weeks and you’re up another $75/st to $1,155/st.

Anyway, enough from me. Here is what survey respondents had to say:

$1,200 or higher

“Pipe mills are busy with data centers and availability is an issue, so demand is up.”

$1,150-1,999

“Energy pricing is going up and will keep prices elevated due to higher logistics costs.”

“No sign of slowing down at the mills, which are still pushing out orders.”

“Prices for HRC have room to keep increasing.”

“Still lean availability.”

“Increases should slow down as backlogs are satisfied.”

“Educated guess on when the market will start moving down.”

$1,100-1,149

“I know things.”

“The spread between imports and domestic is still attractive, but no one is buying heavily offshore. At some point, that spread will cause buyers to look overseas.”

“Based on an average of $8/ton of CRU increases per week since the beginning of the year.”

“Nucor will continue to move prices up $5-$10 per week on their CSP.”

“Imports will start to put some downward pressure on pricing. But apparently this rally/pricing still has some more room to climb.”

“Nothing to stop the rise. Mills are making a killing and will continue to push prices higher due to protectionism.”

“More upside coming but should pause.”

$1,050-1,099

“Educated guess on when the market will start moving down.”

“We’re close to the end of the rally.”

“There is actual demand right now and a shortage of supply.”

“Need to keep a favorable price to reduce outside markets.”

“Very slow increases over the next several weeks will continue.”

“We expect pricing to keep climbing for a while longer and then fall back in the summer.”

$1,000-1,049

“Summer slowdown and imported tons will hit. USMCA new agreement.”

“There is not enough demand. Prices cannot remain this high.”

$950-999

Editor’s note: The folks who think we’re falling below $1,000/st are keeping their reasons to themselves.

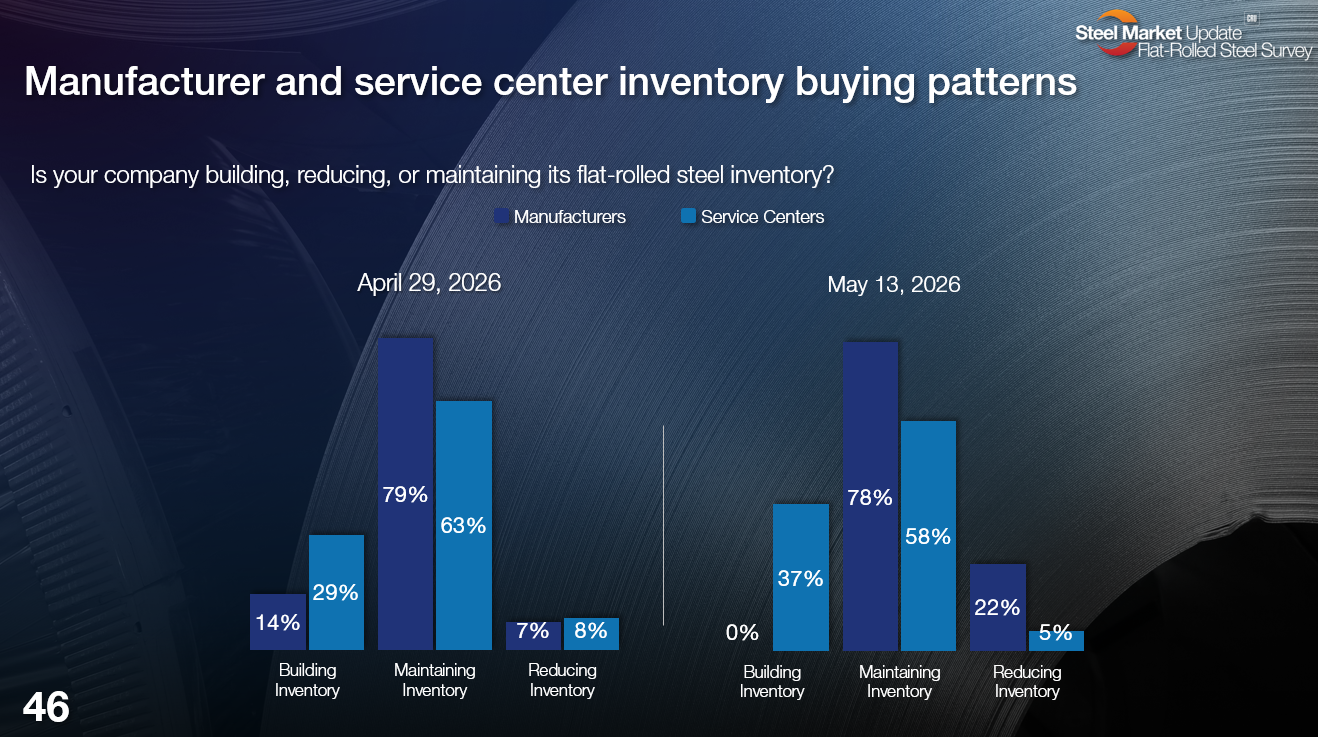

Time to rebuild inventories, if you can find the tons

With inventories dangerously low, it should perhaps come as no surprise that we’re seeing more service centers trying to rebuild depleted stocks.

I’ve been making a lot of comparisons to 2021 lately. This one goes back even further. We haven’t seen 37% of survey respondents saying that they’re building inventories since late December 2011!

But not everyone who is trying to build stocks is able to. Here is what some had to say:

“Reducing, but not by choice.”

“Trying to build. But finding it difficult.”

“Hard to build inventory when the mills are over four weeks late on everything.”

“We’d be building our inventory a lot more if mills deliveries were more on time.”

“Trying to build. But delivery is still lacking.”

USW contract talks and auto ‘strike banks’

By the way, you might have noticed SMU has been covering upcoming labor negotiations between U.S. Steel, Cleveland-Cliffs, and the United Steelworkers union.

Why is that relevant to efforts to replenish inventories and prices? The current contract is set to expire on Sept. 1. While deals are often reached at the last minute, there is always the risk of a strike or a lockout. And we’re told automakers will begin building their “strike banks” – extra tons to tide them over in the event of a work stoppage – next month.

As automakers build up their banks, it could put some pressure on the galvanized market in particular. And since automakers often get priority, it could also make it that much harder for other customers to build inventories.

That’s not to say that there is nothing to tap the brakes on prices moving higher. Seasonality is a stubborn thing. And lead times are into the typically slower summer months.

Also, we’re already seeing an uptick in import volumes. They remain at low volumes by the standards of recent years. But I wouldn’t be surprised to see volumes tick up – especially with US prices high (and moving higher), lead times long, and certain domestic mills effectively skipping over some spot customers.

To paraphrase Monty Python, every ton is sacred. And as Mercury Resources CEO Anton Posner noted in his Community Chat, customers are anxious to know exactly when their vessels with foreign tons are coming in.

SMU Community Chat

Our next Community Chat will be on Wednesday, May 27, at 11 am ET. We’ll be catching up with JSW Steel USA CEO Rob Simon for the first time since the Tampa Steel Conference back in February. The live webinar is free for anyone to attend. You can sign up here, and feel free to share that link with anyone else who you think might be interested too.