Analysis

May 7, 2026

Final Thoughts: Steel is (quietly) partying like it's 2021

Written by Michael Cowden

The rally we’ve seen in US sheet and plate prices started off as a story about limited supply. It’s now clear it’s just as much about increased demand.

The rally has also lasted more than seven months, something without recent precedent. Unless your definition of recent includes the snapback in demand following the pandemic.

The big question remains how long the rally will last. Some market participants say it could keep going into the fall as supply continues to tighten. Others think it will run out of steam over the summer as imports ramp up and should a USMCA deal result in lower tariffs on Canada and Mexico.

More on that in a moment. But, first, let’s some put some context behind what this quietly historic sheet prices rally.

Hot roll on its longest roll since 2020-21

Check out SMU’s pricing archives. You’ll see hot-rolled (HR) coil prices have been stable or rising since mid/late September, so for roughly 7.5 months. That’s the longest upcycle we’ve seen since a 13-month rally spanning from August 2020 to September 2021. And it’s come in the absence of splashy headlines about triple-digit price increases.

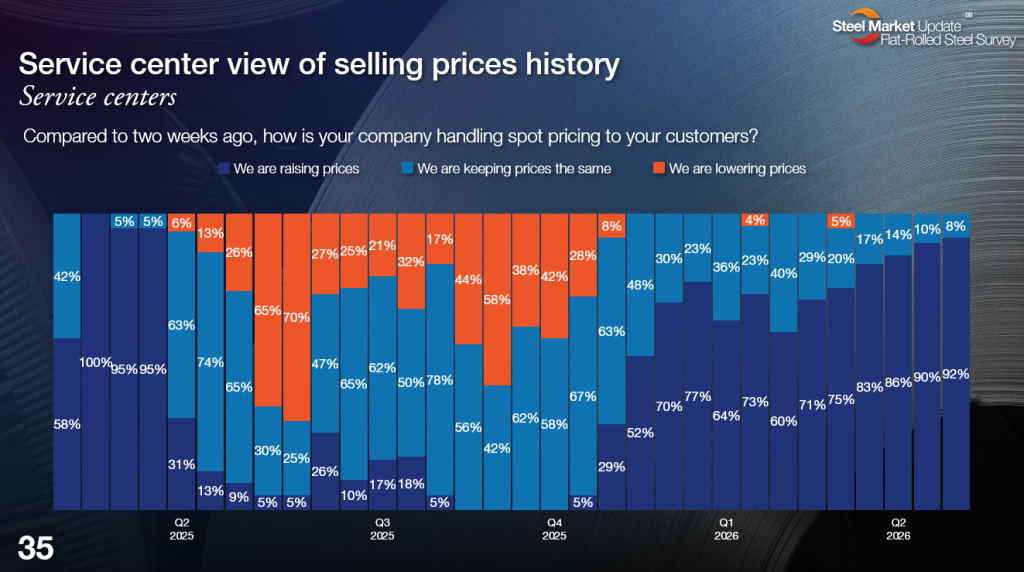

And it’s not just prices at the mill level. For 12 surveys straight, more than 50% of service centers respondents have told us they’ve been raising prices as well, as you can see in the chart below.

We do our surveys every other week. So that represents roughly six months. (A little longer once you factor in the impact of holidays.)

We haven’t seen a result like that since 2021, when from January to September (18 consecutive surveys), more than half of service centers reported raising prices to their customers.

Demand looking ’21-ish too?

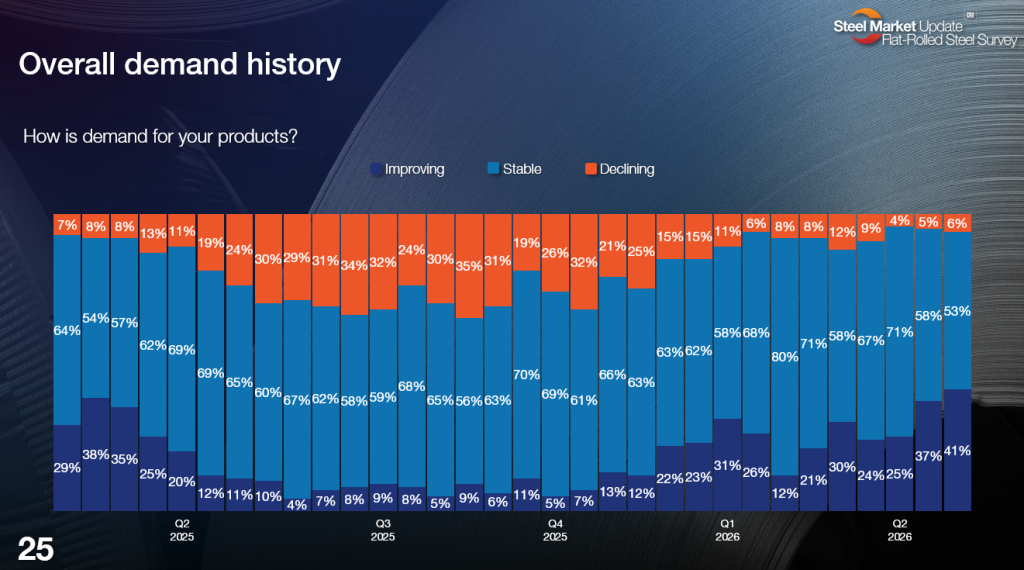

And we’re seeing similar trends in some of the data we collect on demand. More and more survey respondents are telling us they’re seeing improving demand.

Forty-one percent of respondents described demand as improving in our most recent steel-market survey. Check out that data series on our website. You’ll see we haven’t recorded a number that high since early July 2021 – nearly five years ago.

Lead times, not so much

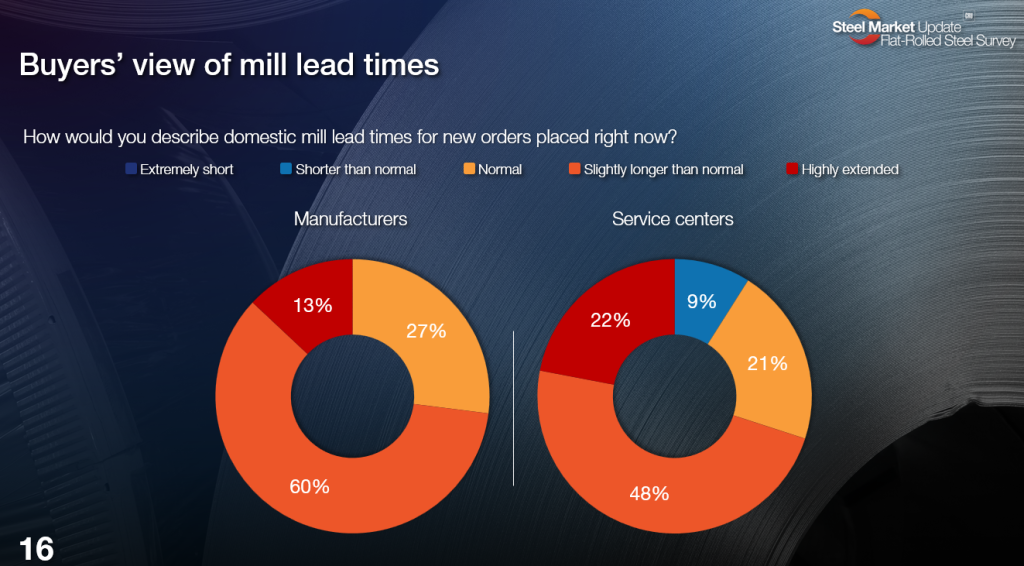

As we reported last week, lead times remain extended. Sure, some mills are catching up. But others continue to report lead times as far out as late July/August. That’s roughly on par with overseas import lead times. And we got word earlier this week about a significant unplanned outage an EAF mill in the South.

I’m not going to parse the numbers again. Instead, here is how people feel about current lead times:

Among service center respondents, 70% describe lead times as extended, and 22% consider them highly extended. Only a minority describe lead times as normal (21%) or shorter than usual (9%). It’s a similar result when you ask manufacturers the same question.

But this is where comparisons between now and 2021 start to unwind. Rewind to 2021, and for a long stretch approximately 40% of respondents reported lead times as highly extended. At times, the figure jumped to nearly 80%.

So, again, this is a historic rally. But it’s nothing (at this point) like the surge in demand we saw in the year following the pandemic.

Where will prices peak?

In fact, most survey respondents don’t see much additional upside to prices – at least by the standards of 2021, when HR hit nearly $2,000/st.

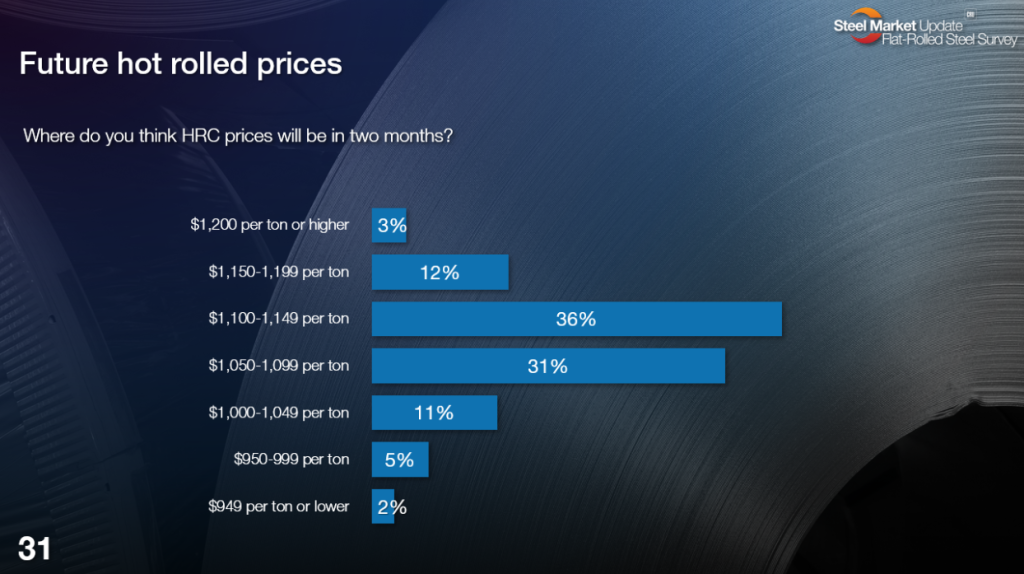

SMU’s price assessment for HR stands at $1,075/st on average. The chart below shows where survey respondents think HR prices will be in two months:

More than half (51%) think HR prices will climb above $1,100/st. But only 3% think $1,200/st HR is in the cards.

Here is what some of them had to say. (Note: The folks who predict prices will be below $949/st in two months are keeping their reasons to themselves.)

$1,200 or higher

“Tight supply.”

$1,150-1,1999

“Mill lead times are still extended, and availability is tight.”

“Mills should be caught up with backlogs, and demand will settle down some.”

“Mills will take advantage of tight supply and improving demand.”

$1,100-1,149

“Seems that market continues to be tight I don’t see anything on the horizon that will change that.”

“Nothing to stop the rise. Mills making a killing and will continue to push prices higher due to protectionism.”

“Slow growth in price.”

“Steady demand will provide enough to fill domestic order books while increasing material costs for international producers will keep import offers higher.

“Imports will start to be put some downward pressure on pricing.”

“Prices are going up $5-10 per week at the moment.”

“We will continue to see smaller increases, which helps keep foreign as less of a factor. But at some point, more foreign purchases will increase.“

$1,050-1,099

“Energy pricing is going up and will keep prices elevated due to higher logistics costs.”

“Peaking higher and drifting back down over the summer.”

“Very slow increases over the next several weeks.”

“We’re close to the end.”

“We are expecting a peak around $1,100/ton and then a gradual float back down.”

$1,000-1,049

“Summer slowdown and imported tons will hit. Also new USMCA agreement.”

$950-999

“There is not enough demand, prices cannot remain this high.”

“Import and weak demand.”

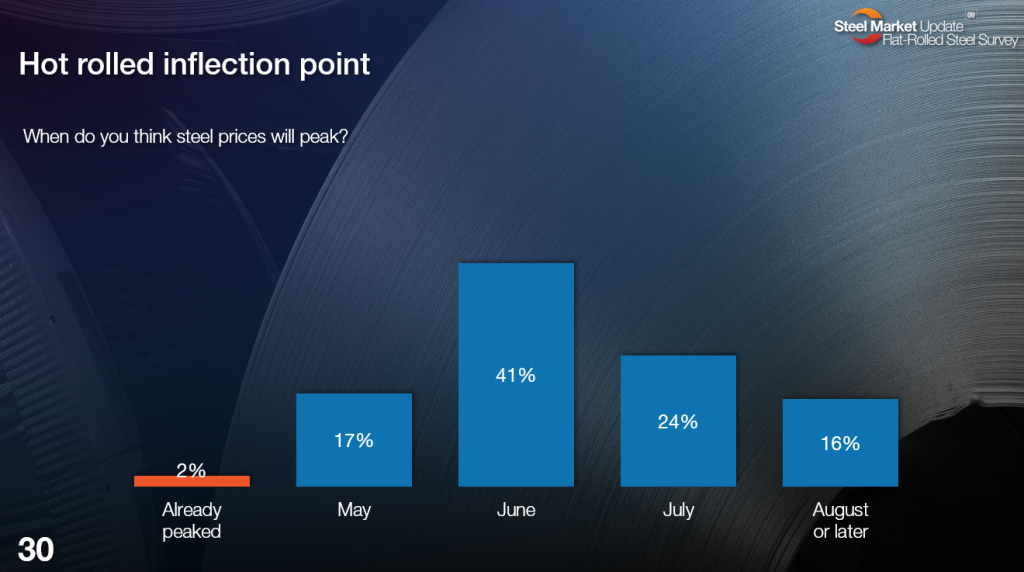

When will prices peak?

As far as when people think the current rally will peak, look at the chart below.

A clear majority of respondents (65%) think the current rally will extend into June or July. But only 16% think it has legs beyond August, which is fewer than those who think we’ve already peaked or will later this month (19%).

Here is what some of them have to say, in their own words. (Note the folks who think prices will continue to rise into at least August are more vocal in the comments than those who think we’ve already peaked.)

August or later

“Demand is still the key factor. Inventory levels are dangerously low, nothing to stop the upward movement right now.”

“Supply is so tight, and demand will start to improve – keeping prices higher longer.”

“I don’t think anything gets cheaper until labor negotiations are settled.”

“Still running up, mill outages on the horizon, and imports not yet coming.”

“The push to the peak is slow and will take some time. Shutdowns will play a role in the peak, and those happen in the fall.”

“There is nothing to stop prices from increasing with inventories low, demand stable, and imports are not a good option.”

July

“Increased production at a few mills, restocking to normal levels of inventory, and CRU quarterly average pricing increasing. Buyers will exhaust 2nd quarter pricing and stay away from 3rd quarter if possible. Conservatively, Q2 average will be up $80 per ton.”

“Supply will increase by early Q3, and imports will be more interesting by then.”

“July is what I’m hearing internally and from others for the peak of this price cycle.”

“Once negotiations of TEMEC (USMCA) are finished.”

“Another 9-10 weeks of $10-$15/NT slow and steady increase.”

“Not sure what stops the current run-up in pricing.”

“Seasonality and softer demand.”

“Plate mills are already quoting late July deliveries.”

June

“I feel we are going to reach a point as mills continue to inch up pricing that foreign will become more of a factor.”

“High enough where some import tons will get into the market, and if there is a USMCA agreement to allow Canadian and Mexican tons into the US without tariffs or reduced tariffs.”

“Iran war will increase raw costs for mills, but demand is slowing down due to cost pressures.”

“The shortage of supply has increased due to the recent introduction of actual demand.”

“Inventories are lean, lead-times long, and imports surpressed. And it’s all amid scheduled mill maintenance outages.”

“Tariffs appear rock solid for now. No reason to think otherwise.”

“Until the conflict in the Middle East is over.”

“When the Iran war is over.”

“Should stop climbing by summer.”

May

“The end seems to be in sight, and summer almost always kills a rally.”

“We definitely aren’t there yet. Maybe late May/June? It probably won’t peak until after the Outages and once ‘summer doldrums’ are here.”

Already peaked

“There is not enough demand. Prices cannot remain this high.”

What the bears think

You’ll notice a theme in those comments. Those who think a peak is in sight reason that imports will become a bigger factor. Yes, mills have been raising prices gradually, but 6-7 months of gradual price increases eventually amount to something bordering on drastic. Some also speculate USMCA negotiations could result in lower tariffs on Canada and Mexico. And sprinkled among those respondents are folks who aren’t seeing demand improving in the markets they serve.

It’s worth noting we’re already seeing evidence of increased import activity. The US could import as many as 1.76 million metric tons (mt) of steel in April, according to license data from the Commerce Department. That’s up ~10% from 1.61 million mt in March and up ~23% from a recent low of 1.43 million mt in December 2025. It also marks the highest monthly total for steel imports since 2.03 million mt arrived from abroad in July of last year.

What the bulls think

In contrast, those who think prices will continue to push high for longer stress increased demand amid an ever-tightening supply squeeze. They have good points too. (One of them being upcoming contract negotiations between integrated mills and the United Steelworkers union.)

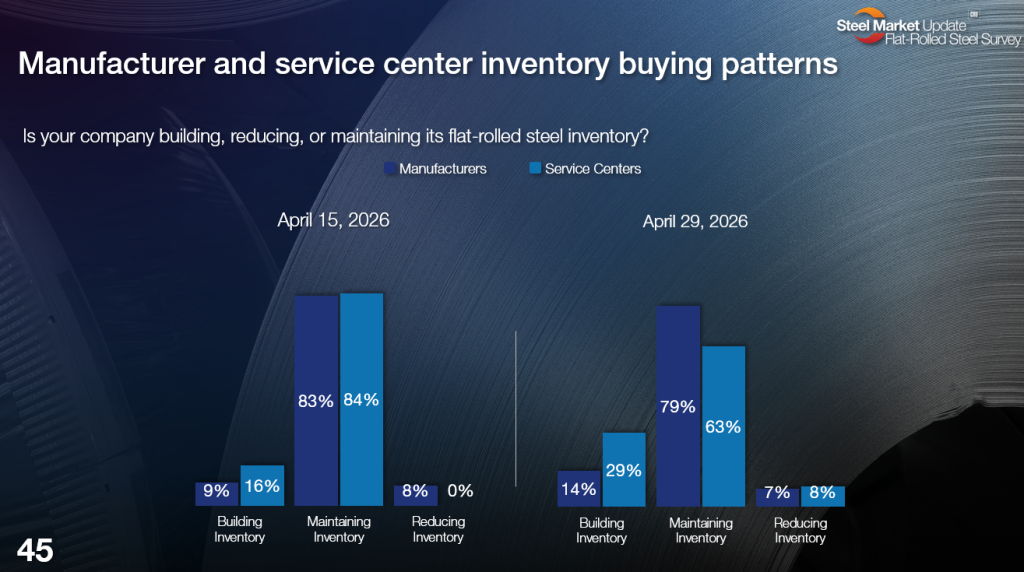

Look at the slide below on inventories:

We’ve seen an increase in the number of steel buyers building inventories. But most are merely maintaining them. And if demand is improving, that could mean they’re effectively reducing stocks.

SMU will release April service center inventory figures to our premium subscribers on Friday, May 15. I don’t know where the final numbers will land.

But we’ve seen in the past that our survey results offer a good indicator. And given what I see above, I wouldn’t be surprised to see inventories little changed from March or perhaps even lower.

That’s saying something. Because (yep, another 2021 reference) March sheet inventories were the leanest we’ve recorded since June 2021.

And if April inventories are flat or lower than March, it would be another clear indicator that, whatever might happen with imports or USMCA this summer, the supply squeeze is still on for now.

Get the good stuff

Executive members get access to SMU’s news and pricing. Premium members get all that and a bag of chips. Namely, access to our surveys and key proprietary data – such as our service center inventory figures.

The latter alone is reason enough to upgrade from executive to premium. If you’d like to, please reach out to us at smu@crugroup.com.

Make your voice heard!

Does what you see above reflect your company’s experience? Or are you seeing things differently? Either way, we’d love to hear from you.

Your responses to our surveys help SMU keep its finger on the pulse of the steel market. Thanks to those who already participate. And if you’re interested in doing so, let me know at michael.cowden@crugroup.com.

It only takes a few minutes to complete, and we’ll always keep your name and your company’s name confidential.