Analysis

May 31, 2026

Final Thoughts: Sheet prices still have gas in the tank

Written by Michael Cowden

Stronger for longer sentiment remains in the house when it comes to flat-rolled steel prices, according to SMU’s latest steel market survey.

And that’s despite chatter in some corners about the summer doldrums, supply finally catching up to demand, and potential concessions related to United States-Canada-Mexico Agreement (USMCA) negotiations.

Before we dive into some highlights of our latest survey, a few housekeeping notes. The page numbers in the slides below reflect where you can find them in the full deck. And those with a premium subscription can access the full survey results here.

Executive members, data like this is a great reason to upgrade your subscription! Contact us at smu@crugroup.com to learn more.

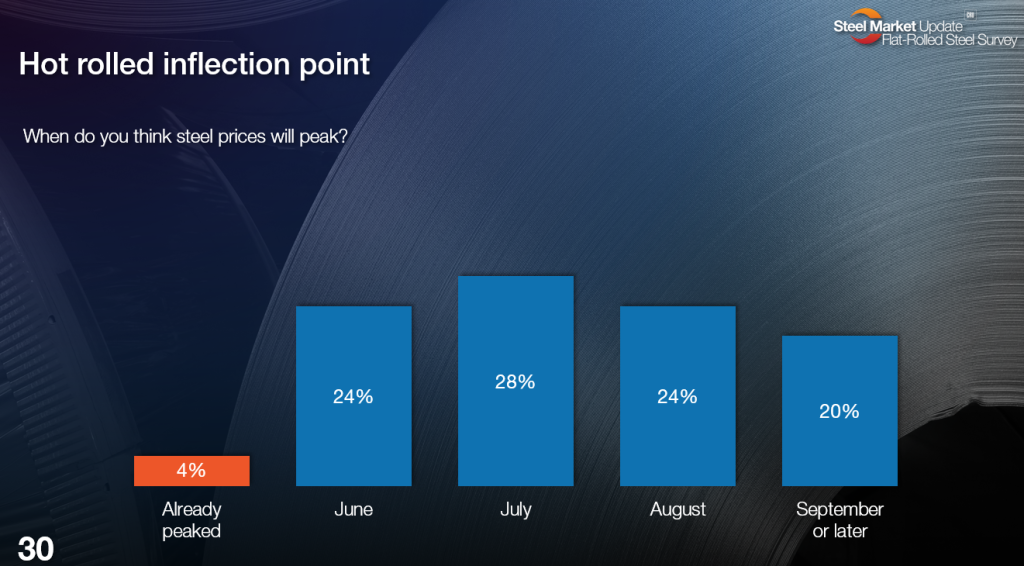

When will sheet prices peak?

Long story short, the consensus (as it’s been pretty much all year) is next month or the month after. Now that we’re in June, the most common response (28%) is that prices will peak in July.

Again, this is not a new trend. People have been rolling their expectations on when prices will peak from one month to the next for most of this year. For example, in our surveys in late April and mid-May (we survey the market every two weeks), the most common response was that prices would peak in June.

One change to note: Some of you told us you think prices will continue to rise into the fall. So we’ve added a new answer option “September or later”. And, it turns out, a significant minority (20%) think sheet prices will remain on an upward trend until at least Labor Day.

Here is what some survey respondents had to say:

June

“Demand is softening, and supply is increasing.”

“Heading into summer doldrums.”

July

“Imports, increased supply, mills start to get caught up, and the Iran war ends. It could stay flat or continue up if auto demand picks up.”

“Outage on top of outage should be the boiling point.”

“Demand is slowing, and inventories are growing.”

August

“Demand continues to drive pricing, along with the Middle East conflict.”

“Supply is super tight.”

“Improving demand and low inventory.”

“Market pushback on increases.”

“I would think the auto production softness will eventually catch up with the market.”

September or later

“Without demand collapsing, the mills can continue to raise prices.”

“This is such a unique market. Trade barriers and tariffs have created a perfect storm, allowing domestic mills to consistently raise prices … while keeping imports on the sidelines. It will top out. But much later. And it probably won’t fall quickly due to the high value of inventory.”

“Demand is getting stronger, which is a good sign heading into the summer. No imports to slow this down, and mills will keep discipline and raise prices gradually.”

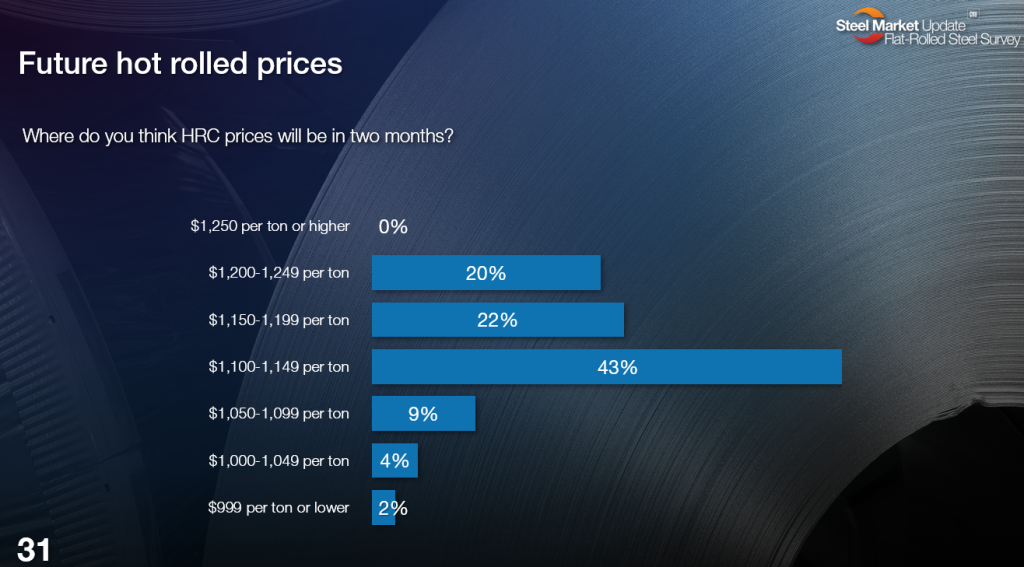

Where will HR prices be in two months?

We continue to see a similar trend when we ask people where they think hot-rolled coil prices will be two months from now.

SMU’s hot-rolled coil price now stands at $1,095 per short ton (st) on average. (We’ll update prices again on Tuesday afternoon.) And the most common response (43%) is that prices will be slightly higher two months from now ($1,100-1,149).

HR prices have been rising at a pace of $8-9/st in recent weeks. So such a response assumes we’ll see a moderation in price gains over the summer months. But not everyone agrees with that more conservative outlook. A significant minority (20%) think prices could be $1,200/st or higher by late July.

That, too, squares with what we’ve seen in the past. Earlier in the year, a lot of people thought prices couldn’t go above $1,000/st or there might be political intervention. Then it was $1,100/st. Now that we’re nearly there, there is a school of thought that HR can’t go above $1,200/st.

There seems to be less concern about politics now. The theory I’ve heard most often is that HR prices over $1,200/st would invite imports back into the domestic market in a significant way.

But enough from me. Here is what survey respondents had to say:

$1,200-1,249

“Nothing to stop the rise. Mills are making a killing and will continue to push prices higher due to protectionism.”

“No sign of slowing down at the mills. They’re still pushing out orders.”

“Indications from mill reps.”

“Demand increasing.”

$1,150-1,999

“Inventories are low, demand is improving, and imports are not as available.”

“Effects of the Iran war.”

“Low supply.”

“Seems like protectionary policy is in place for steel worldwide. Current geopolitical conditions are probably constraining a solid demand environment.”

“Small, incremental increases will continue.”

$1,100-1,149

“Very slow increases over the next several weeks will continue.”

“Price increase fatigue setting in.”

“There will be an attempt to keep the increases steady but relatively conservative.”

“A little more increase, then it flattens out for a few months.”

“I believe the market will stabilize in this range.”

$1,050-1,099

“We still think we’ll rise through May/June and then fall from there on out.”

Sidenote: The people who think prices will drop below $1,100 two months from now are keeping their reasoning to themselves. If you happen to be one of them, please feel free to share your thoughts in the comments next time. SMU won’t bite!

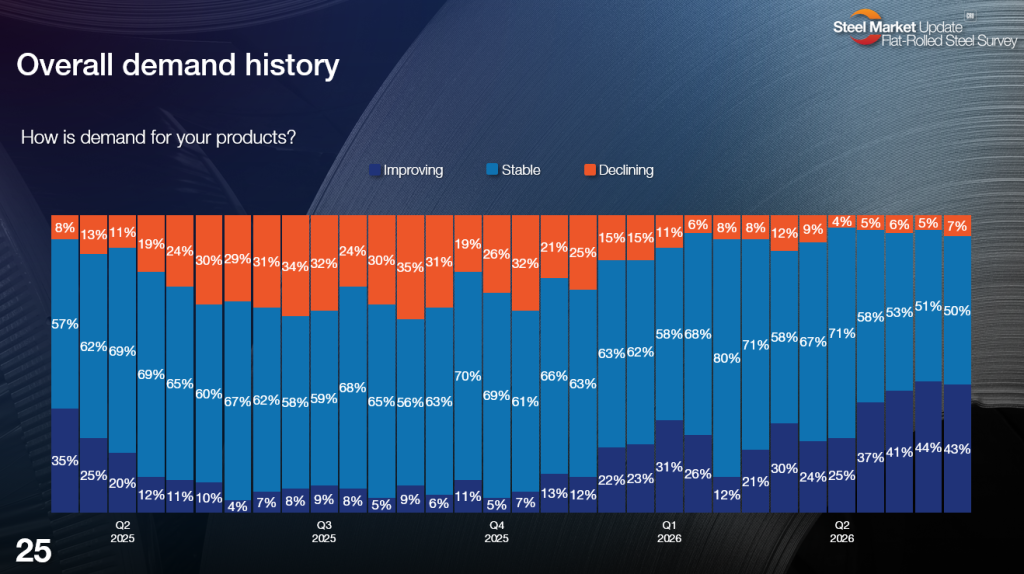

Demand remains (mostly) solid

As we’ve noted before, the sauce that seems to be making this near record-breaking rally (at least in terms of duration) and extreme spot shortage tolerable to steel buyers continues to be solid demand.

Forty-three percent of survey respondents tell us that demand is improving, little changed from our last survey (44%) – and at the highest levels we’ve seen since July 2021, according to our data archives. That said, it’s important to note that the July 2021 figure was actually on its way down from 55% in May of that year. (The 2021 rally showed some early signs of slowing down in July.)

Here is what survey respondents had to say about demand trends:

“For the first time in a looonnnnggg time, it feels like demand is improving. We’ll take it!”

“We have had an increasing backlog all year with a slight dip last week. I think it is just a lull.”

“Demand is steady and strong, but sourcing is restricted”

“Spot is hot.”

“Spot demand is exploding.”

“Better each couple of weeks.”

“Heading into our summer doldrums.”

“Demand forecasts start dropping in June.”

“Larger sales projects are lagging due to instability in the economy.”

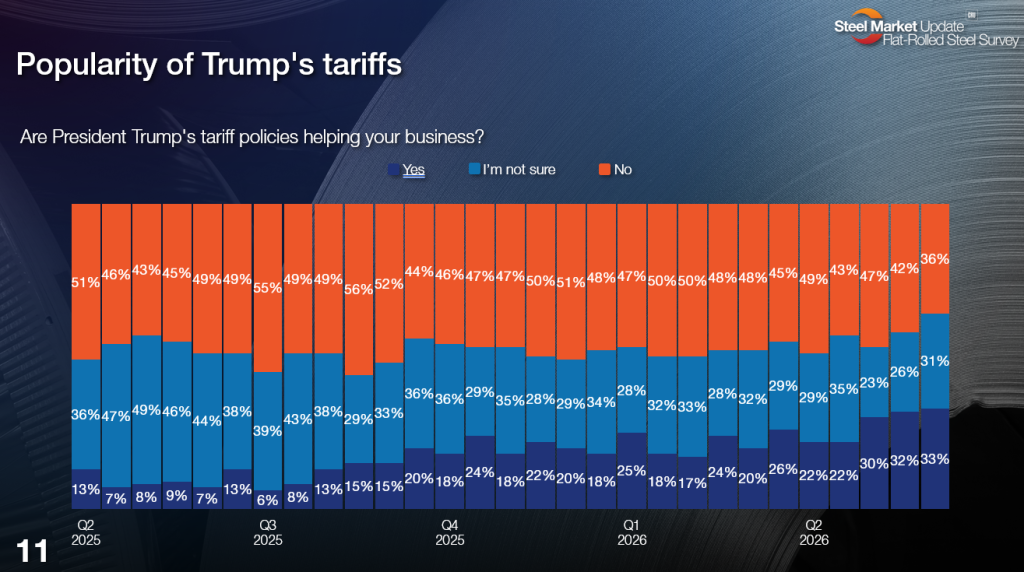

More buyers turning pro-tariff?

So if we’re seeing mostly a continuation of the trends I’ve been highlighting in these columns for a little while now, what has changed? Somewhat to my surprise, it’s opinions around the Trump administration’s tariffs.

It would be a stretch to say tariffs are popular among the steel buyers we survey. That said, roughly one-third reported tariffs are helping their businesses in our latest survey. That’s consistent with numbers we’ve over the last couple of months. (Each bar in the chart above is two weeks.)

And that’s a big change from 6-7% a year ago. (I had to get a 6-7 joke in somewhere for the kids reading along.) Seriously, though, rewind to last year and the percentage of respondents saying tariffs helped their business was consistently in the single digits. And for long stretches, half or more said tariffs were hurting their business.

What’s changed? Are revised downstream tariffs helping steel buyers? Maybe buyers are finally seeing evidence of reshoring? Perhaps buyers are more invested in tariffs now that they’ve got inventory reflecting a 50% Section 232? Or is it something else entirely?

Here is what some of those survey respondents had to say:

Yes, Trump’s tariffs are helping my business

“Still seeing signs of quotes for items being re-shored.”

“Virtually no imports, and parts are finally being reshored.”

“The domestic push helps the logistics side of the business.”

“Inventory values are increasing and products are shipping.”

I’m not sure whether Trump’s tariffs are helping my business

“Hurt on the buy side, help on the sell side.”

“I’m not sure. But I know the war with Iran is not helping!”

No, Trump’s tariffs are not helping my business

“Tariffs have just made things more expensive. Trying to track all of the monthly tariff dollars has forced us to add staff.”

“All eyes in our sector are on USMCA. Fingers crossed for a smooth renewal of sorts.”

“Hurting. Protectionism has allowed the mills to continue to raise prices each week and limited contract tons to the min.”

“They are terrible and not conducive to free and fair trade.”

“Creating additional cost impacts.”

“Restricting trade and competition.”

SMU Steel Summit: See you in Atlanta on Aug. 24-26!

Every year, we see registrations for SMU Steel Summit start to tick up in a big way after Memorial Day. And this year is no exception.

You can see the latest list of companies that have already registered to attend here. We’ll be updating the list as more registrations roll in.

Want to let the steel world know you’ll be joining us on Aug. 24-26 in Atlanta? Then register here!