Final Thoughts

July 10, 2026

Final Thoughts: Is a week of flat prices and lead times signal or noise?

Written by Michael Cowden

SMU’s lead times for both hot-rolled (HR) coil and cold-rolled (CR) coil ticked down this week, according to our latest steel market survey. We’re talking less than half a week in each case, which I’d read as essentially flat.

For what it’s worth, I pay more attention to trends than any one given survey result. But if a trend of flat lead times holds, it would represent a change. And we’ve also seen a few of the other indicators we track slip from historic highs – so the potential shift is worth paying attention to.

To be clear, I’m not saying that the hot-rolled market has suddenly gotten looser. It’s still awfully hard to find spot tons from a domestic mill. Or even from a service center, for that matter. And that’s probably not going to change anytime soon. But maybe, just maybe, the historic supply squeeze we’ve seen is starting to ease, at least a little.

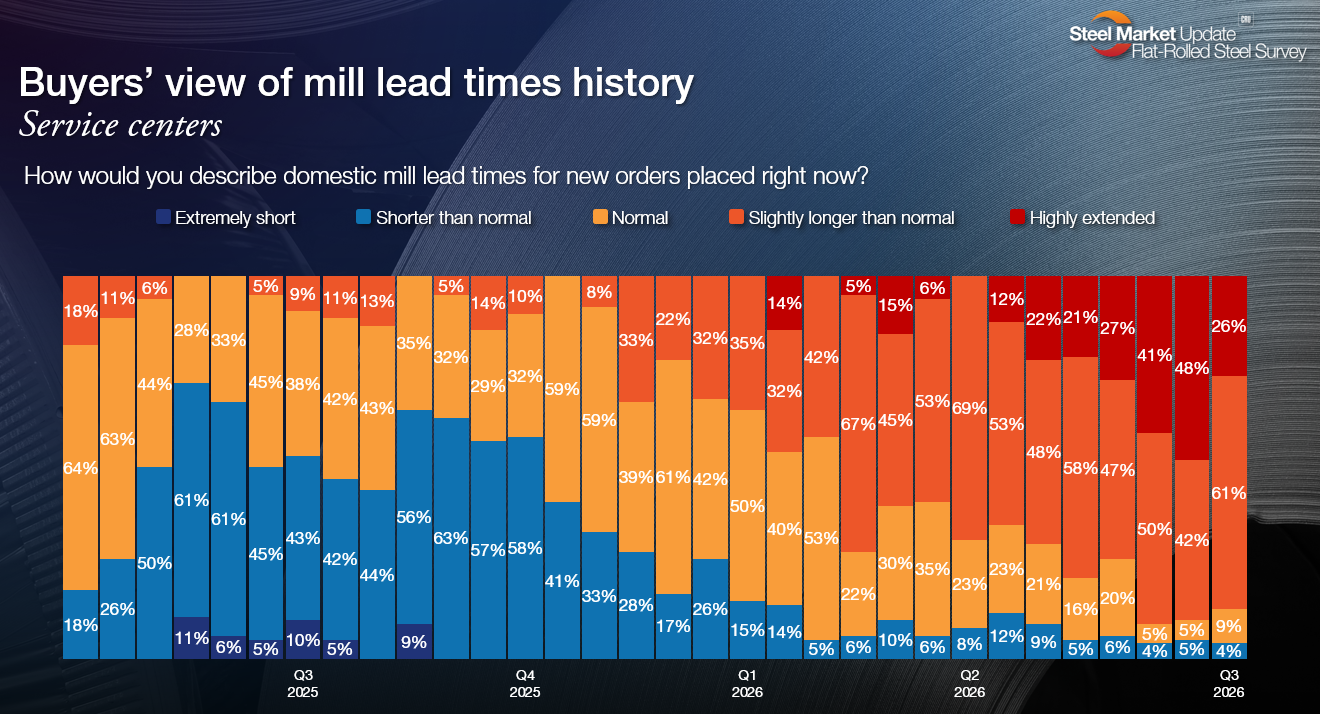

Let’s start with lead times

Our HR lead time stands at 7.3 weeks on average, down from 7.7 weeks in our prior survey. Sure, we’re still at the highest point we’ve been since October 2021 (8.1 weeks), according to our lead time records. But we’ve seen lead times increasing every survey since mid-March. So a dip, even a small one, is something we haven’t seen for a while.

And I can see the case for things potentially plateauing around historically high levels. Sure, just about everyone (87% in our last survey) agreed lead times were long. But fewer (26%) see them as highly extended than in prior surveys, when ~40-50% characterized lead times as such.

Another thing worth pointing out: A lot of imports have been ordered, and not just from buyers on the coasts who typically swing between domestic and offshore material.

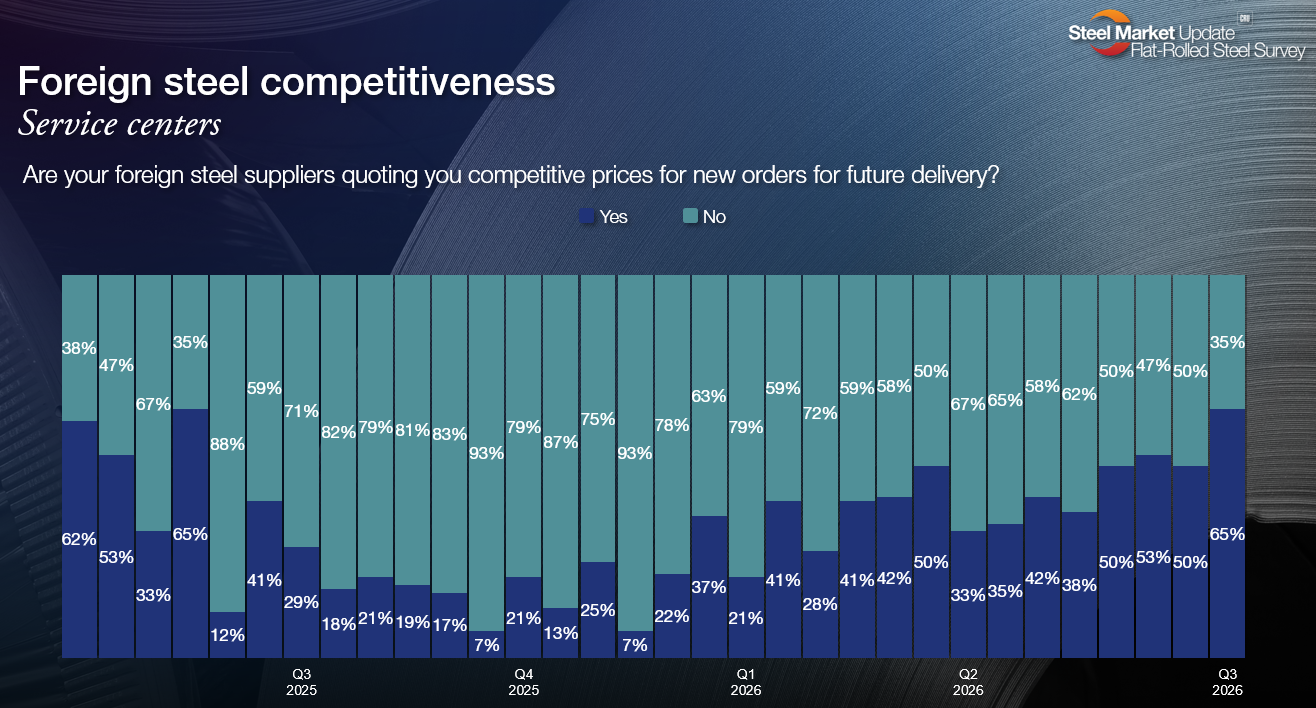

Here come the (import) tons?

I say that because another notable change in trends is how many service centers now say foreign steel prices are competitive. At the outset of Q2, only 33% of service center respondents said imports were competitive. Now, at the beginning of Q3, that figure stands at 65%.

One buyer in the Houston area told me earlier this year, when imports were at historic lows, that even H-Town had become a domestic steel town. Maybe that script has flipped. Anecdotally, I know some buyers in the Midwest who usually buy domestic but who have bought significant quantities of imports, a fair amount of it from Vietnam. And it was ordered in some cases not because those Midwest buyers were itching to buy imports but because they couldn’t get steel from US suppliers at what they felt was a reasonable price (or in some cases at any price) or lead time.

You can see some of those volumes in government data. The US imported 547,300 metric tons (mt) of flat-rolled steel in June, according to license figures. That’s up 3.4% from 529,400 mt in May and up 46% from a 2026 low of 375,800 mt in February.

Vietnam and Algeria trump Canada on HR?!

And there are some interesting tidbits below those headline figures on hot rolled.

The US imported more than 25,000 metric tons (mt) of hot-rolled sheets from Vietnam in June, according to license data from the US Commerce Department. That’s more than double the approximately 9,500 metric tons that arrived in May. It’s also more than any other single country shipped to the US last month. The June figure also represents the highest volume Vietnam has sent to the US since at least July 2020.

It’s not just Vietnam that sent more tons than usual. Algeria shipped nearly 15,000 metric tons of HR to the US in June, up from zero recorded shipments in at least the past six years.

Sidenote: It’s still crazy to see Canada, which had long been the top HR import supplier to the US, relegated to a bit role with only 11,600 metric tons in June. What a difference a 50% Section 232 tariff makes!

And I’m told to expect more imported HR at least through September, or roughly where our current average lead time for hot-rolled (HR) coil is now (~7.5 weeks on average).

There are some questions about whether the trend of higher imports will continue into the fall. For example, I spoke with one service center executive who said his company – which has bought imports from Vietnam throughout much of the year – passed on the latest round of Vietnamese HR offers (~$1,050/st delivered into the Chicago area) on expectations that domestic pricing and availability would improve in Q4 and that prices might ease.

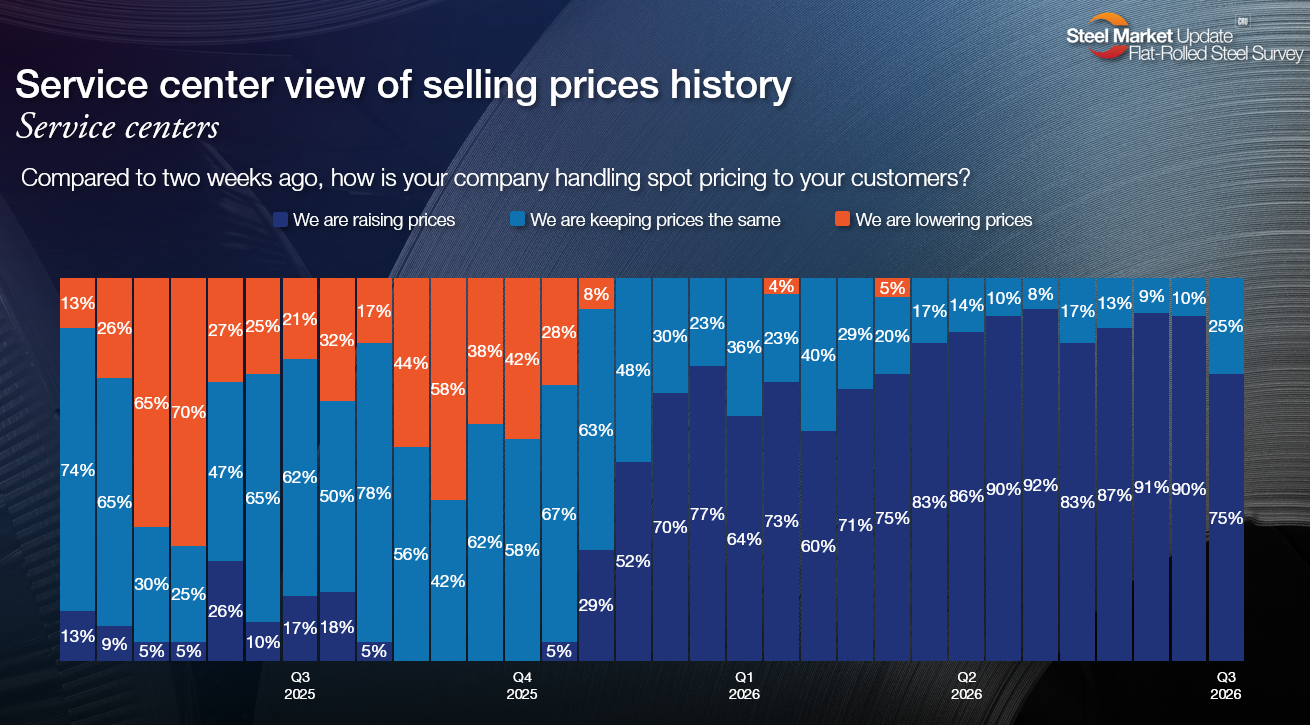

A shift in service center pricing?

Another thing that’s worth noting from our last survey: Only 75% of service center respondents reported raising prices to their customers. I say that partly in jest. Because 75% would be an extremely bullish number in almost any prior pricing upcycle outside of 2021. But it’s down a little bit from the 85-90% we saw throughout Q2.

The trend of (slightly) fewer service centers raising prices dovetails with Nucor keeping its consumer spot price (CSP) flat for consecutive weeks for the first time since Jan. 5. SMU, meanwhile, kept its HR price at $1,160 per short ton (st) this past week, unchanged from the week prior. We hadn’t kept prices flat for consecutive weeks since early March, per our interactive pricing tool.

Not everyone is thrilled with CSP being flat. The market consensus seems to be that Nucor doesn’t want HR prices to get too high and attract even more imports, which makes sense. But it doesn’t sit well with other mills who think there is no reason to cap prices if supplies are still tight. And I know some buyers are frustrated that few tons seem to be available at CSP (and even fewer at the advertised three to five week lead time).

SMU’s average price is $30/st higher than CSP in no small part because other mills don’t appear to feel constrained by CSP anymore. (There is a reason why the high end of our HR price range is $1,200/st.) And I’ve heard that prices from service centers for domestic material can go into the $1,400s/st – something you don’t see in a weak market.

I think you could make a case that Nucor is taking the long-term view and others a more short-term view. Neither is wrong.

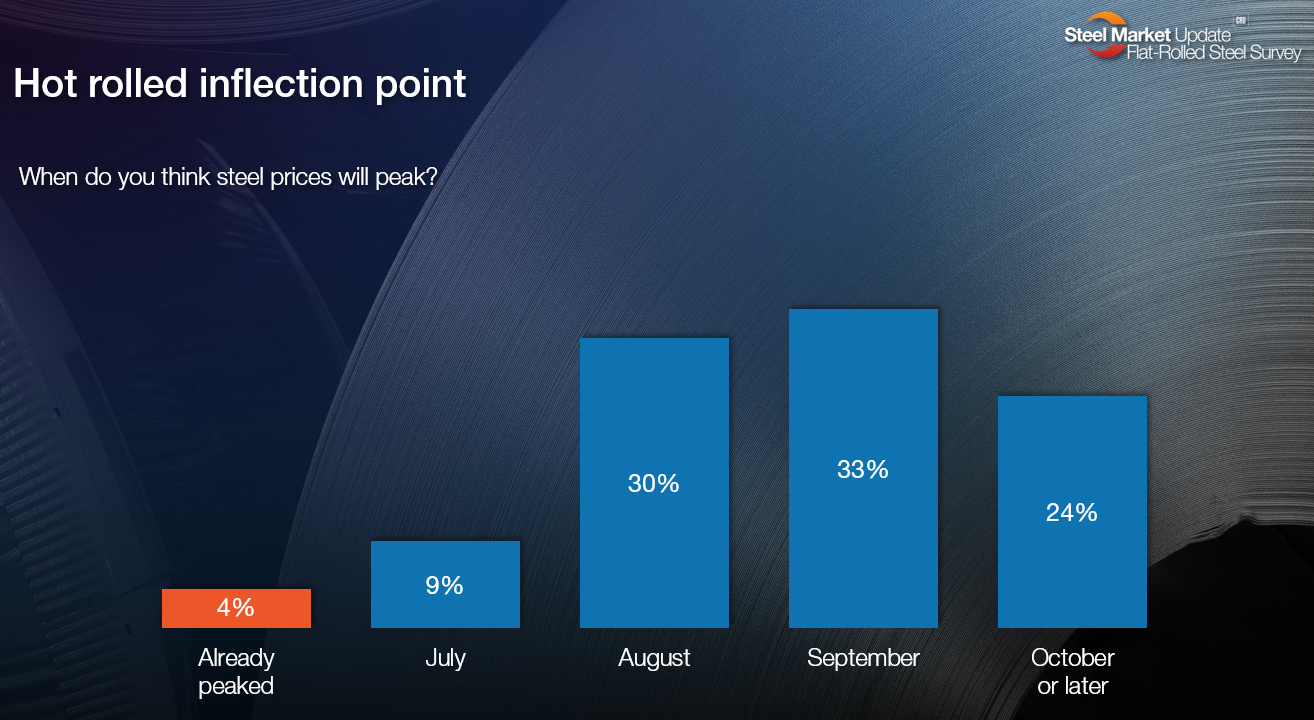

And like I said, the market, especially for hot-rolled coil, remains very, very tight for the time being. And most steel buyers (57%) think HR prices will be at or above $1,200/st by early September – which is hardly a bearish signal.

It’s what comes after September that’s a little less clear.

Very few people (13%) think prices have already peaked or will peak later this month. But significant numbers think sheet prices will peak in August (30%) or September (33%) – even if a solid minority (24%) think they’ll keep rising into October or later.

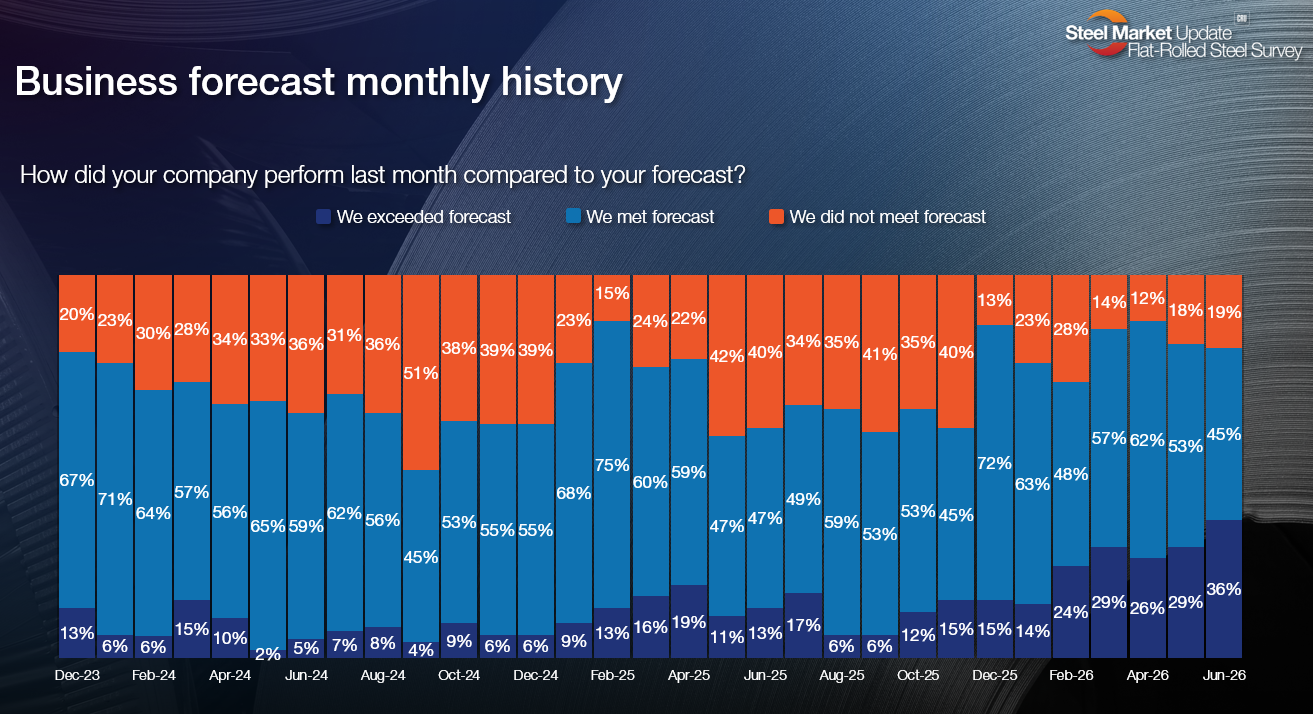

What’s the good news?

Check out the chart below. Thirty-six percent of survey respondents tell us that they beat forecast last month, up from 29% two weeks prior – and following a steady upward trend since the beginning of the year. We haven’t seen this many people reporting beating forecast for a long time.

So might we be past the peak of the supply squeeze that stretched lead times to their highest point since 2021? Maybe.

But is it still a pretty good steel market? Absolutely.