Market Data

May 5, 2026

SMU Price Ranges: Sheet, plate extend gains as better demand enters the chat

Written by Brett Linton & Michael Cowden

Sheet and plate prices remained on an upward trend as industry sources increasingly asked whether improved demand might be driving the market as much as limited supply.

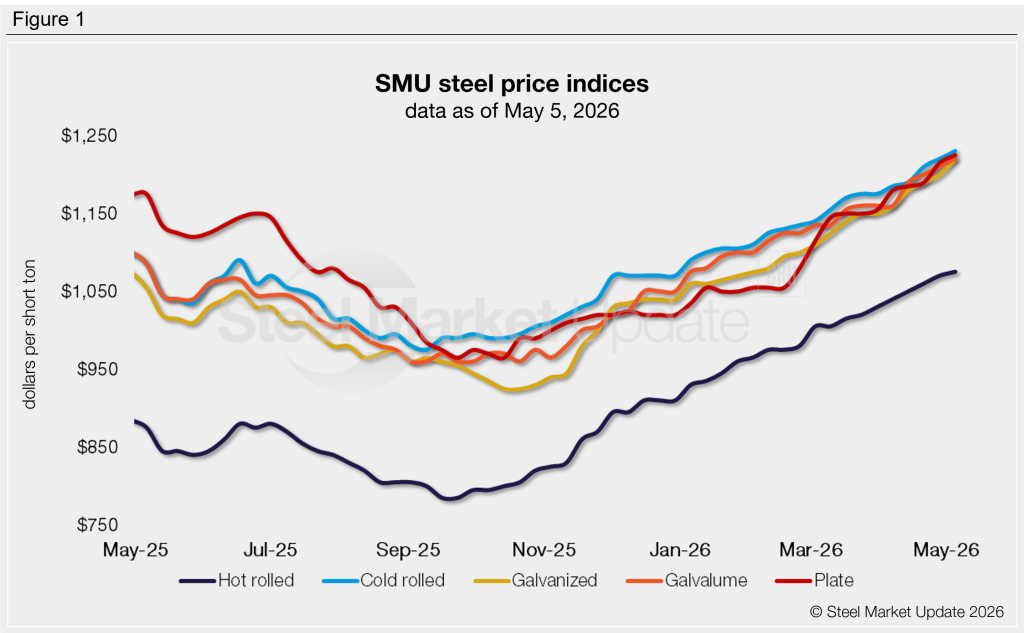

Case in point: SMU’s price assessment for hot-rolled (HR) coil now stands at $1,075 per short ton (st) on average. That’s up $5/st from last week and up $165/st from the beginning of the year. It also marks the highest point for HR prices since May 2023 – three years ago.

On the hunt for elusive spot tons

And with many buyers trying to max out their contract tons, an already tight spot market might be getting even tighter.

“We’re all searching for steel, not a deal,” one Midwest service center source joked of his quest to find spot tons.

The prevailing view earlier this year had been that stronger prices resulted primarily from limited domestic supplies (because of widespread outages, planned or otherwise) and limited imports (because of higher tariffs).

Those factors are still in play. Market participants continue to report delays and production issues across a range of domestic mills. (Lead times at some are as far out as August, nearing parity with import lead times.) And there are few signs of any tariff deals.

“I thought lead times would hit July, and price would begin to drop – but the mills are still trying to play catch up,” the Midwest source said.

Limited supply meets solid demand

Other sources noted that both Nucor and Steel Dynamics Inc. posted record steel shipments in the first quarter – and that crude steel output is high – factors suggesting limited supply alone doesn’t tell the whole story.

They pointed to strength in markets as diverse as data centers, solar, and the border wall – in addition to restocking activity. “It’s not just supply, it’s demand,” one Gulf Coast source said. “We’re busier than busy can be.”

A few questioned how long the rally could last, especially when the combination of high US prices and long domestic lead times reduce the risks associated with imports. But they were also leery of calling the peak of a rally whose duration has smashed most expectations.

“I thought this would peak by the end of March, and I was dead wrong,” a second Midwest service center source said. “And now some people – mostly the mills – are saying this thing will be strong through the balance of the year.”

SMU’s price momentum indicator remains at higher for both sheet and plate products, signaling that we expect prices to increase further in the short term.

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil: $1,050–1,100/st, averaging $1,075/st

The lower end of our range is up $10/st week over week (w/w), while the top end is unchanged. Our overall average is up $5/st w/w.

Hot-rolled lead times range from 5–10 weeks, averaging 6.7 weeks as of our April 30 market survey.

Cold-rolled coil: $1,200–1,260/st, averaging $1,230/st

The lower end of our range is unchanged w/w, while the top end is up $20/st. Our overall average is up $10/st w/w.

Cold-rolled lead times range from 6–10 weeks, averaging 8.0 weeks through our latest survey.

Galvanized coil: $1,180–1,260/st, averaging $1,220/st

Our entire range is up $20/st w/w.

Galvanized .060×48” G90 benchmark: SMU price range is $1,270–1,350/st, averaging $1,310/st FOB mill, east of the Rockies.

Galvanized lead times range from 6–10 weeks, averaging 8.0 weeks through our latest survey.

Galvalume coil: $1,180–1,260/st, averaging $1,220/st

The lower end of our range is unchanged w/w, while the top end is up $20/st. Our overall average is up $10/st w/w.

Galvalume .0142×42” AZ50, grade 80 benchmark: SMU price range is $1,609–1,689/st, averaging $1,649/st FOB mill, east of the Rockies.

Galvalume lead times range from 7–10 weeks, averaging 8.4 weeks through our latest survey.

Plate: $1,190–1,260/st, averaging $1,225/st

The lower end of our range is up $20/st w/w, while the top end is unchanged. Our overall average is up $10/st w/w. Plate lead times range from 6–8 weeks, averaging 7.1 weeks through our latest survey.

Brett Linton

Read more from Brett Linton