Analysis

May 10, 2026

Final Thoughts: A look at May's scrap market

Written by Ethan Bernard & Stephen Miller

The May scrap market in the US seemed to be just finishing up its settle as of the writing of this column. Luckily, we have our latest ferrous scrap market survey to give us some timely insights.

On the one hand, it remains an uncertain market. We have what remains an unpredictable tariff situation (even if we’ve all grown accustomed to it). And now we have the Iran war added to the mix. The duration of the conflict is unclear, but its impact on shipping and oil prices sure isn’t.

On the other hand, we’ve also seen a rally in US sheet prices that has lasted more than seven months. (See Editor-in-Chief Michael Cowden’s previous Final Thoughts here.)

Looking for something normal? We have the usual spring dynamic of more scrap availability after the winter freeze. The word “sideways” came up a lot among survey respondents. Then again, more than a few were seeing increasing demand as well.

So where does that leave us? Sure, there are a lot of variables at play. But with more than 40 years in the scrap industry, SMU’s Stephen Miller has seen the dynamics of most markets.

Here is his take on our latest scrap survey results and what he’s seen so far in the market.

Miller’s view

After reviewing SMU’s scrap survey results, it looks to me like the trade on both sides of the furnace essentially got things right. The only discrepancy between the two sides was the price of prime scrap – whether sideways, or up (and if up, by how much).

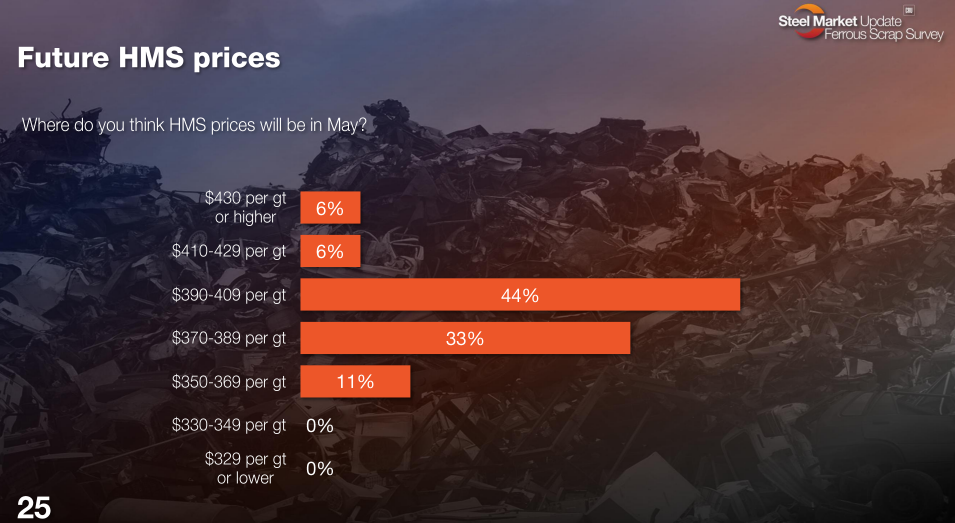

The May settlements are somewhat complete. It’s safe to say the obsolescent grades – including shredded, P&S, and HMS – traded sideways in all regions. That was a result of continued solid demand and firm export prices. Also, dealers faced increased transportation costs and other energy-related sundries. So, they were united in the sideways cause. The run-up in steel prices didn’t hurt things, either.

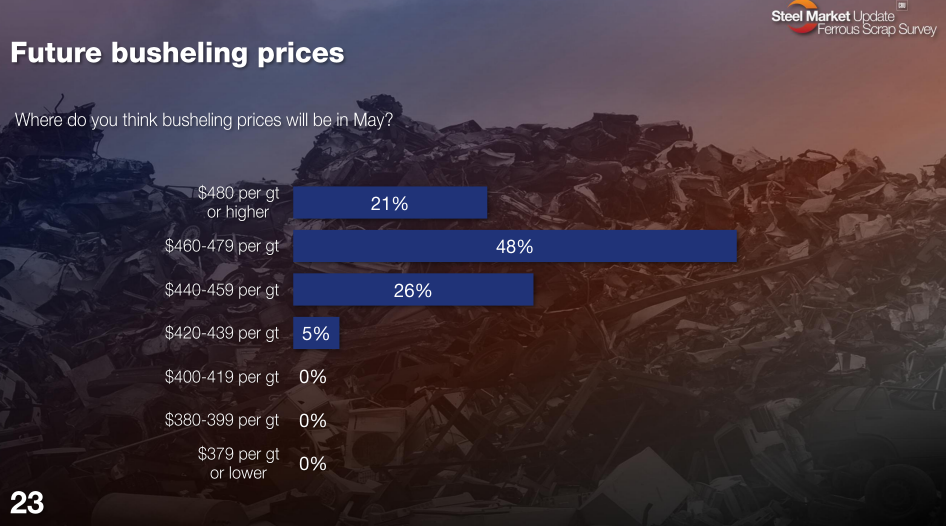

The busheling price was another matter. Several large EAF-based buyers dug in their heels at sideways pricing. At least three steel mill complexes decided to keep prices static. A source told SMU that many independent suppliers sold their tonnages away from these mills in favor of steelmakers paying better numbers.

The largest scrap buyer in the country went up $10 per gross ton (gt) on busheling and is apparently filling in adequately. Other consumers in the Ohio/Pittsburgh districts went up $10-20/gt on prime grades. The Chicago market remains unsettled but is trending toward higher tags for busheling and bundles, according to a source there.

Survey says

Now let’s take a lot at what some of our survey respondents were saying about demand and pricing ahead of the May settle.

Editors’ note: If your company would like to have its voice heard in our scrap surveys, contact david.schollaert@crugroup.com. We’ll always keep your name and your company’s name confidential.

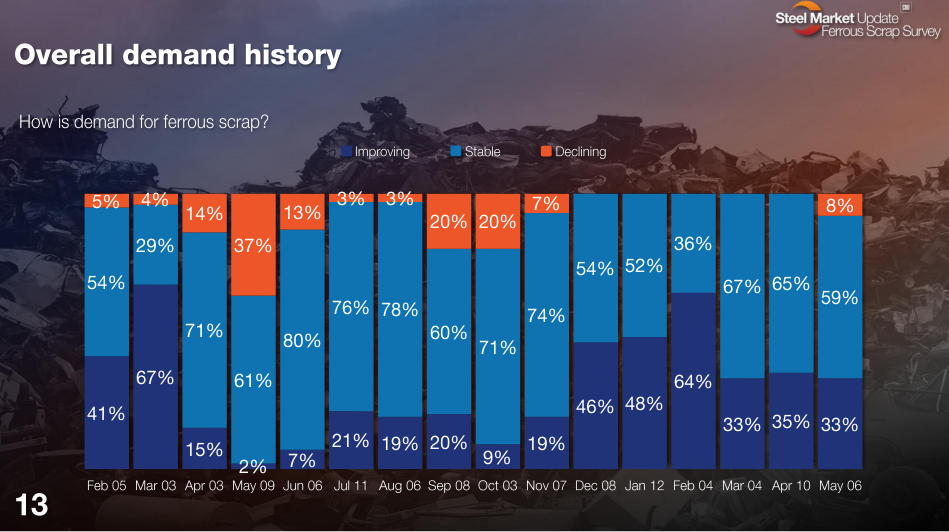

How is demand for ferrous scrap?

“It is hard to tell because of the tightly controlled market, but it seems that scrap demand is actually increasing.”

“Flat-rolled producers are getting busier with HRC prices strong.”

“Current demand is stable due to lead times that are not extending, and supply is still good.”

“Stable to improving in some areas.”

Where will busheling prices be in May?

“Probably (up) $20/gt.”

“Re-establish price spread between primes and obsolete grades.”

“Flow and demand are in balance.”

“Logistics costs are increasing due to Iranian war causing overall costing to be increased.”

“Add $20/gt to April price.”

“Tighter supply and demand growing.”

“Increased demand and static supply.”

“Car industry is not strong.”

Where will shred prices be in May?

“Rumor Control Central say ‘sideways.'”

“Excess supply over demand due to high obsolete flow in spring.”

“Mills still think seasonal downturn is afoot.”

“Demand and supply are stable. Logistics costs increasing may push up overall scrap.”

“Trend is sideways.”

“Shred in certain areas is OK on inventory.”

Where will HMS prices be in May?

“Same rumors, sideways.”

“High supply level.”

“Export has not dragged prices up yet.”

“Demand and supply are stable.”

“Trend is sideways.”

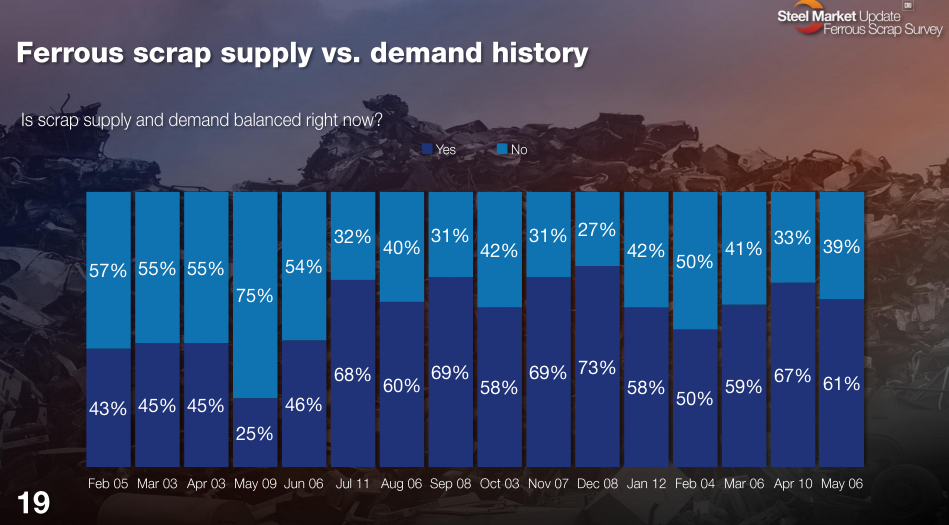

Do you see the scrap market in balance now given supply and demand?

“Demand higher than supply.”

“Slight oversupply on obsolete.”

“Short on prime.”

Time to make plans for SMU Steel Summit!

Spring’s thaw means summer is just right around the corner. And that means it’s time to register for SMU Steel Summit on Aug. 24-26 in Atlanta.

It’s THE summer event for the flat-rolled steel market. We’ll also be featuring plenty of discussions around scrap. It’s the perfect place to network with attendees all along the steel and scrap supply chains. (You can register here.)

Ethan Bernard

Read more from Ethan Bernard