Analysis

June 14, 2026

Final Thoughts: What summer doldrums?

Written by Michael Cowden

Summer doldrums? Not this year! SMU’s latest steel market survey indicates that an increasing number of steel buyers think prices will continue to rise along with the mercury.

What’s more, more survey respondents now think prices will remain on an upswing even as temperatures begin to cool in the fall. That’s a significant change compared to our last survey at the end of May.

Before we dive into things, a few quick notes: SMU surveys the steel market every other week. Below are highlights from our last survey. Premium subscribers can find our full survey results here.

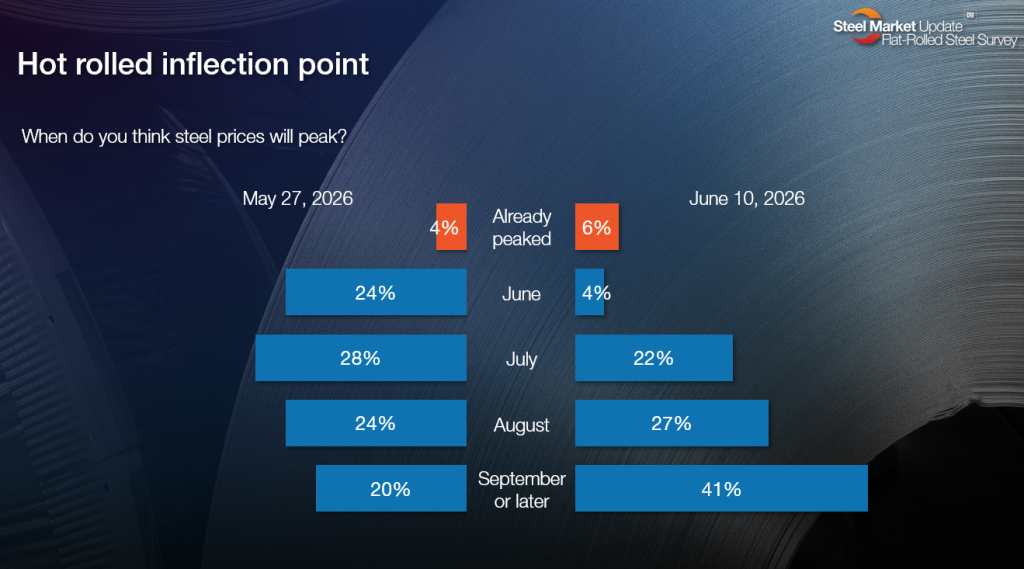

With that, let’s get started with a question on when people think flat-rolled steel prices will peak:

What a difference two weeks make! Now, 41% of respondents think prices will rise into September or later. That’s up from just 20% in our prior survey. And only 4% think prices will peak this month, down from 24% two weeks ago.

Here is what they had to say, in their own words. The bears didn’t elaborate on why they think prices have already peaked or are about to. The “September or later” folks had a lot to say.

June/already peaked

“Steel has a history of decreasing in the summer.”

July

“Demand is lowering slightly, and data center demand is running out.”

“Seeing some signs of overheating, and it could stop the price rally sooner rather than later.”

“Demand is stable. But tariffs and energy pricing are pushing up prices overall.”

“A price increase each week should eclipse demand next month.”

“Shrug emoji”

August

“I’ve been saying that prices would peak next month for many months in a row now. Logic tells me that domestic prices are high enough that foreign steel will start coming into the US soon to keep domestic prices in check. But I’ve been wrong for so many months in a row, now I’m saying prices will peak in 2 months:)”

“Imports remain low. Summer slowdown either nonexistent or masked by low inventory. Also, union negotiations.”

“Imports won’t arrive until mid-Q3.”

“Moving the estimated peak out until conditions (war, tariffs) change.”

“Market demand remains improved for several months.”

September or later

“Why would the mills stop raising prices now? They are in control.”

“Fall outages and contract negotiations will keep numbers up.”

“Supply is tight, and demand is strong. Low imports in the market. More exports to Mexico?”

“Mill outages will be completed, and imports will be arriving more robustly—HR, CR and HDG.”

“Steady demand and low inventories will allow prices to continue increasing.”

“Depends on when imports come in.”

“Due to the U.S. Steel Gary Works #14 scheduled outage through August and rolling maintenance in the last quarter, I feel that it will be early fourth quarter before any price decreases.”

“The domestic steel market has very good demand and is more insulated now from imports.”

“I believe sheet prices could peak around September. By then, the impact of tariffs and supply restrictions should be fully reflected in the market, while demand may begin to soften due to seasonality and buyer resistance to higher prices.”

“Steel sheet prices still have room to increase. This is a market unlike any previous: 50% import tariff and other AD/CVD trade cases are creating a very closed market. US domestics cannot fully supply it. But it will peak sometime—and then get ready for that wild ride.”

“Supply constrictions will continue.”

“Nothing to stop prices continuing to increase.”

What a change from this time last year, when a summer swoon sent hot-rolled (HR) coil tumbling into the $700s per short ton (st) in the fall. Prices fell even more sharply for large spot buyers. That happened despite newly announced 50% Section 232 tariffs and splashy mill price-hike announcements.

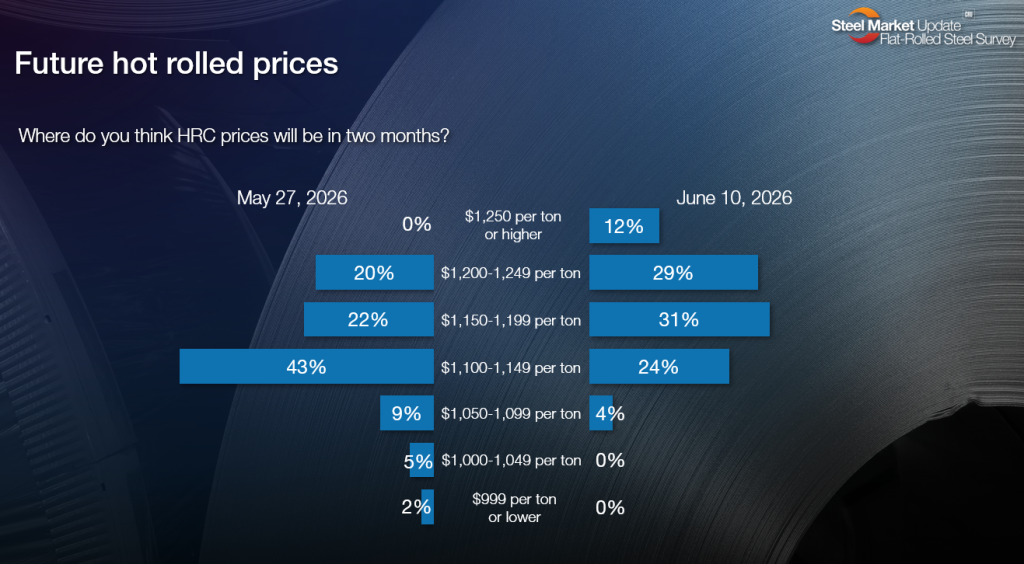

Speaking of HR prices, where do people think they will be in two months – just before we gather for SMU Steel Summit? Look at the chart below.

Here, too, there has been a big change over the last two weeks. In late May, only 20% of survey respondents thought HR prices would go above $1,200/st. Now that number stands at 41%.

In other words, two weeks ago, most people expected prices to level out around current levels this summer. Now, the consensus is that prices will continue to rise. And literally no one thinks they will fall below $1,000/st again anytime soon.

Here is what survey respondents had to say. And, once again, the more bearish among you didn’t elaborate. (Maybe next time?)

$1,250 or higher

“Strong demand and limited supply.”

“Supply constrictions will continue.”

“Tight supply.”

$1,200-1,249

“Nothing to stop the rise. Mills are making a killing. And they will continue to push prices higher due to protectionism.”

“Demand is improving while supply is maxed out.”

“Imports pricing is too attractive at levels higher than $1,250.”

“Over the last six months, we have only seen slight upticks in pricing. Nothing indicates that this will change. Slow and steady.”

“We are seeing a steady increase of $40-60 per ton each month. Until supply catches up with demand this slow rise will continue.”

“No sign of slowing down at the mills. They’re still pushing out orders.”

“Still some room, but reaching a peak.”

$1,150-1,199

“Imports will start to put some downward pressure on pricing. But, apparently, this rally/pricing still has some more room to climb.”

“Lack of imports. Demand staying ahead of supply until more suppliers come back from outages.”

“I think that the mills are cognizant of import being brought in when pricing goes over a certain point.”

“Steady $5-10 ton increase every week with no relief in sight.”

“I don’t know what to think. It does seem like prices will continue to rise.”

“Summer slowdown and imported tons will hit – and a new USMCA agreement.”

“Seems like there is lots of upward pressure on the supply side.”

“Steady ~$7/week increases.”

“Increases should slow down as backlogs are satisfied.”

$1,100-1,149

“Very slow increases over the next several weeks will continue.”

“Supply-demand balance, and a lack of imports.”

“Energy pricing is going up and will keep prices elevated due to higher logistics costs.”

“Scrap is low. Demand is low. War is the only thing keeping fuel high.”

“No imported steel.”

“Optimistic for the Iran war to end and for foreign competition to pick up.”

You’ll notice a couple of themes in the comments above. Namely, prices should remain high in the short term because of tight supply. And, also, that prices could reverse course should supply, driven in part by increased import volumes, catch up to demand.

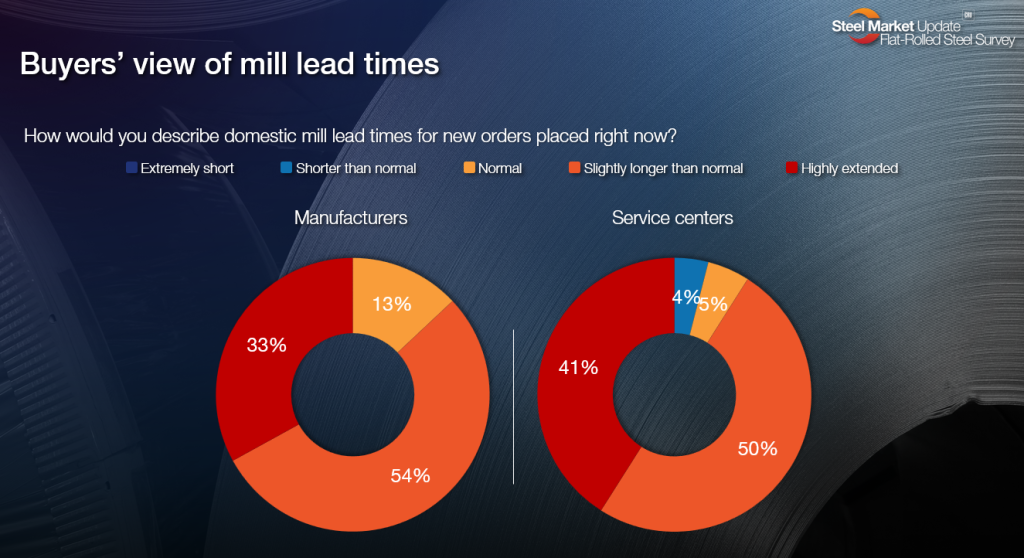

Let’s take the question of supply first. Lead times remain long, as we reported in our Thursday issue. You might quibble with the averages noted there, depending on which mill you’re ordering from. Some producers are catching up to demand. Others appear to be slipping even further behind. (HR lead times at certain producers are into September – which is longer than some import lead times.)

On balance, however, it’s clear that many steel buyers continue to perceive lead times as “highly extended.”

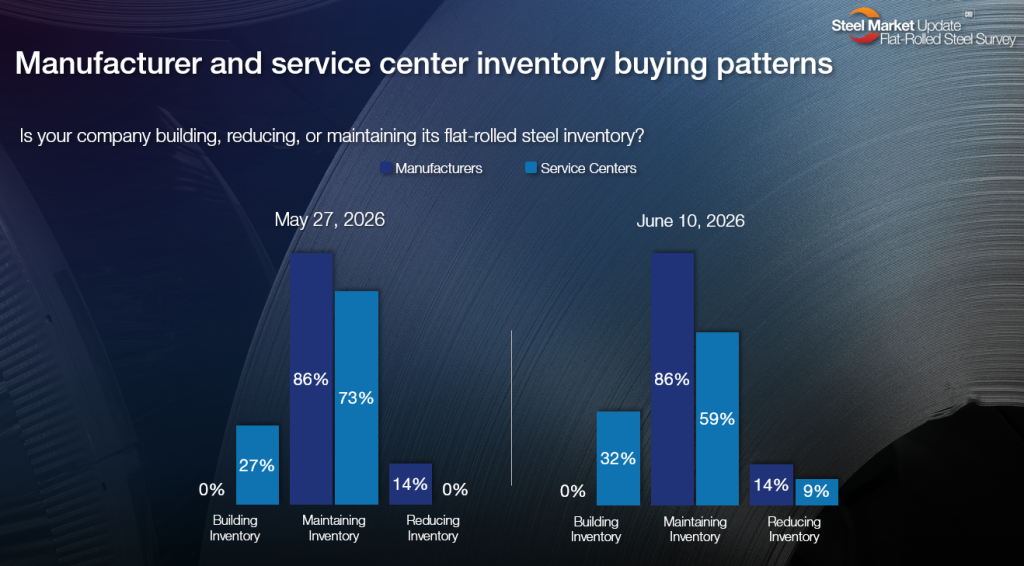

We’ll release May service center inventories to our premium subscribers this week. (That data moves markets. It’s a good reason to upgrade from executive to premium. If you’d like to, let us know at smu@crugroup.com.) More service centers tell us they are trying to build inventories, as you can see in the chart below.

But with lead times long, and some buyers telling us they’re having trouble getting tons at any price, not everyone can build stocks. And so I wouldn’t be surprised if we see inventories tick lower yet again – which supports the idea of a continued supply squeeze, one where availability continues to trump price.

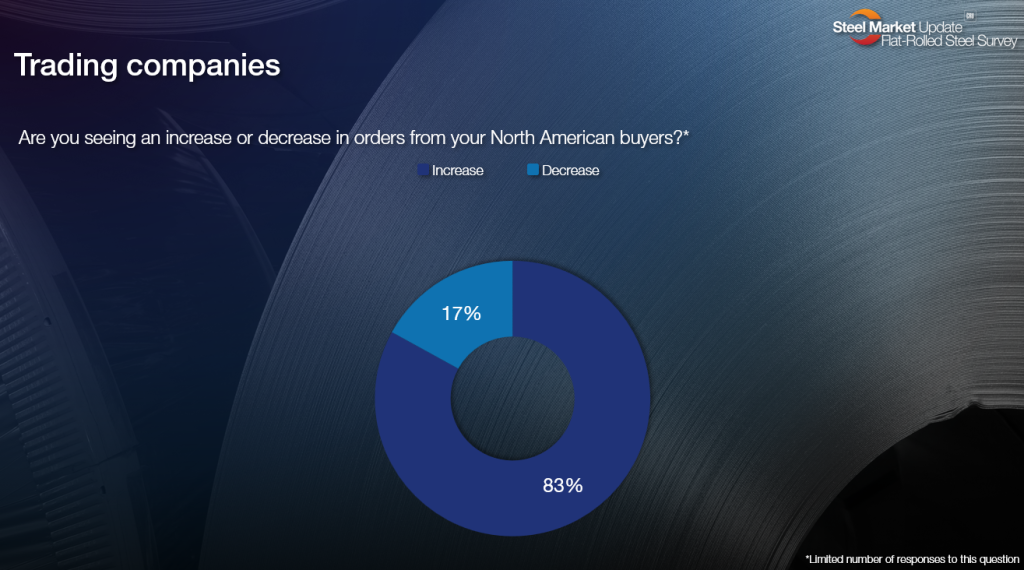

That said, traders for months now have been telling us that they’re seeing more interest from US buyers. And that remains the case:

In the past, that result hasn’t squared with service centers telling us they didn’t see imports as attractively priced.

That’s no longer the case:

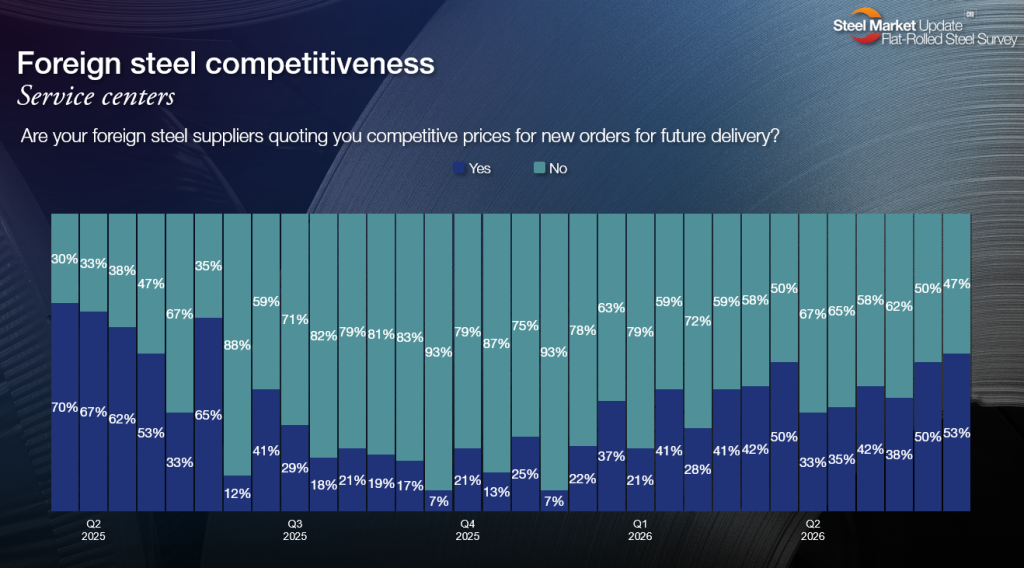

In our most recent survey, we saw the number of service centers saying imports are attractively priced inch above 50% for the first time since Q2’2025. (In 2025, that figure hit 65% before dropping precipitously after President Trump increased Section 232 tariffs to 50%.) The result above tracks with government data, which indicates import volumes have bottomed out and started to move higher.

It also squares with what we’re hearing anecdotally. Namely, that some service centers along the Great Lakes and inland rivers are buying imports in a more significant way than usual. In the Great Lakes, those imports might have come from Canada in the past. But with Canada still subject to Section 232 tariffs, foreign steel is sometimes coming in from as far away as East or Southeast Asia – and that’s despite the delays and higher freight costs stemming from the Iran war.

Let’s say that imported material arrives in August/September. I could see a situation where domestic sheet prices rise until then before levelling out and potentially drifting lower in the fall.

But that’s assuming current trends hold. And a lot can (and no doubt will) change between now and September. USMCA negotiations are underway. Will there be a deal or not? Will we see Section 232 tariffs reduced or removed from Canada and Mexico, or not?

Much also hinges on what happens with labor contract negotiations between U.S. Steel and the United Steelworkers (USW) union, as well as those between Cleveland-Cliffs and the USW – especially with lead times at some producers already past the Sept. 1 deadline for a new contract.

And let’s not forget that whatever happens in the Middle East will have knock-on effects in North America, especially when it comes to fuel prices, freight costs, inflation, and interest rates.

SMU Steel Summit – sign up today!

All of which is to say we’ll have a lot to talk about when we gather for SMU Steel Summit (and AMU Aluminum Summit) on Aug. 24-26 at the Georgia International Convention Center in Atlanta. There will be much to learn from leading industry executives, analysts, and economists – as well as from your industry peers. Hundreds of people have already registered. You can add your company’s name to that list by registering here.