Final Thoughts

June 26, 2026

Final Thoughts - Now in its own newsletter

Written by Michael Cowden

We are pleased to present this week’s Final Thoughts, now delivered as its own newsletter and written by SMU editor-in-chief Michael Cowden.

I saw this post pop into my LinkedIn feed today. I assumed it was from a few hours ago. The text seemed OK. But I wanted to figure out how we somehow got the prices wrong.

Then I looked more closely. I realized it was from years ago. And, also, I was the one who’d written it. As Homer Simpson would say: “D’oh!”

The text didn’t initially seem dated because the basic questions about how long lead times might stretch and how long prices might rise are just as relevant now as they were in 2021. Sure, hot-rolled (HR) coil prices aren’t nearly as high now as they were then. (HR was at $1,770 per short ton in late June 2021, according to our pricing archives.) But some of the other data points we track are at their highest point since 2021.

Here are just a few examples: May service center sheet inventories are at 44.7 days of supply, the lowest level since May 2021. HR coil lead times are at 7.7 weeks on average, and as long as 12 weeks. That’s the longest they’ve been since October 2021. (It’s a similar story with CR lead times.) And with certain mills seemingly unable to get back on track, some of you tell me a published lead time in September is more like an October lead time in practice.

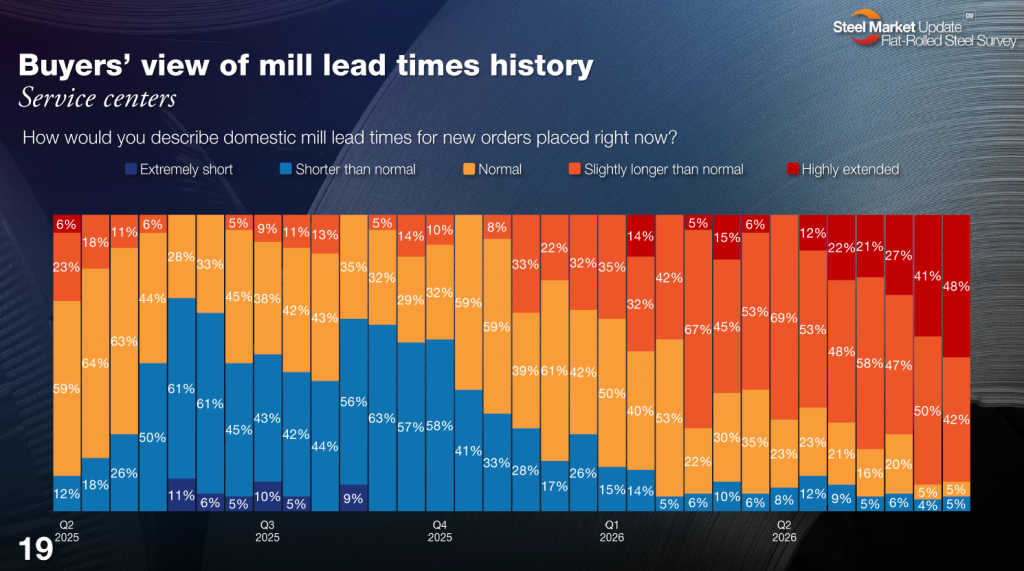

By the way, if you don’t agree with our average lead times, let’s look at them more as a heat map instead. (Editor’s note: The images below come from a Community Chat on Wednesday and from our latest steel market survey, which was released today.)

Forty-eight percent of service center respondents now consider lead times “highly extended.” None considered them to be so at the beginning of Q2.

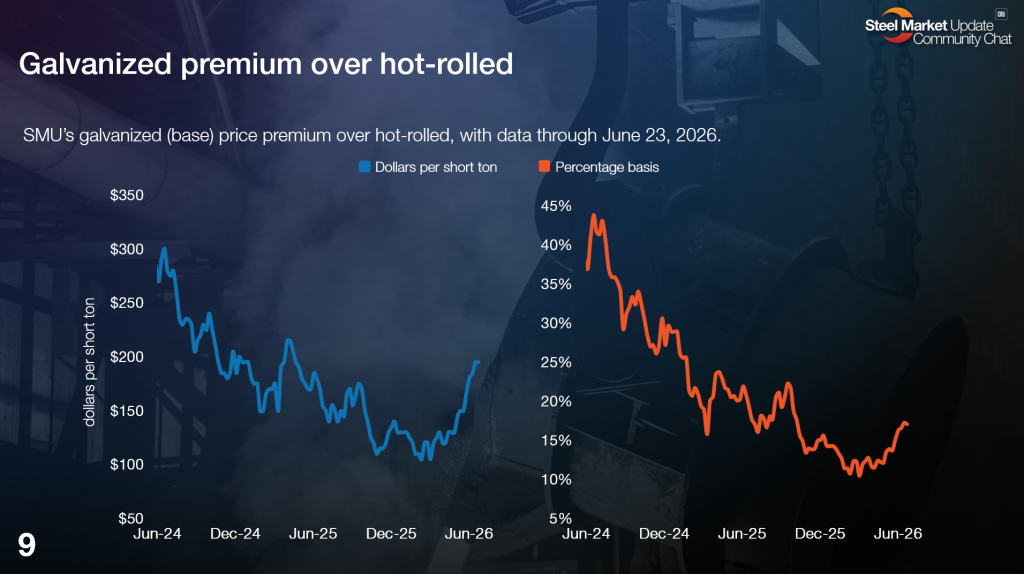

Meanwhile, only 13% of respondents to our latest survey say mills are willing to negotiate lower galvanized prices. That’s the lowest level since 2021, and it’s roughly on par with what we’re seeing in HR. So much for the idea galv is the weaker of the sheet products.

Related to that, no wonder mills have been able to push the spread between HR and galv from approximately $100/st earlier this year to roughly $200/st now.

Fwiw, mills held a roughly $200/st spread between HR and galv base in 2021. But they pushed it to as high as $300/st throughout much of the first half of 2024. Is that where they’re looking to go next?

By the way, I know some of you might laugh at the idea of this elusive thing we call a spot ton of HR when you can’t get a price or a lead time from mills regardless of tonnage. To make matters worse, you might find yourself being held to your contract minimums. And even service centers don’t have tons to spare. If that happens to describe your situation, it’s not just you. Some of the biggest spot buyers and OEMs, we’re told, are struggling to secure tons.

Maybe you can find some spot availability on galv. But you’re probably not finding much in the way of deals. In other words, all data points suggest an extremely tight market right now.

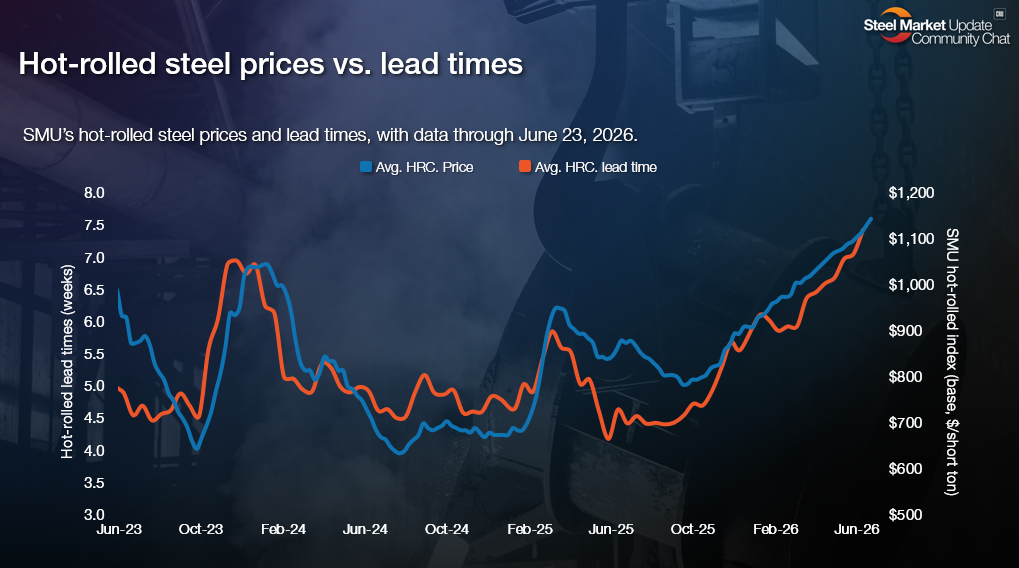

What’s more, prices have been trending upward since mid-October of last year, more than eight months ago. So there has been no dip to buy. We haven’t seen a rally this long since 2021.

What comes next? Do prices plateau and then dip in late Q3/Q4 – which is what we saw in 2021? Or do they continue to rise into 2027?

If you’re looking to get into that topic in depth, I suggest watching the Chat on Wednesday with Timna Tanners, managing director of equities research, at Wells Fargo. She made a good case for a Q3/Q4 peak.

Among some of Timna’s key points: Imports should continue to tick higher, especially with US prices rising while those abroad fall. Domestic production will increase with spring outage season behind us and when U.S. Steel resumes production from a revamped Gary Works No. 14 furnace in August. Also, demand is typically a little softer in the second half of the year.

Not long before the call ended, some of you reached out to me with various counterpoints. Mill maintenance outages, some of which were cut short in the spring, could be longer in the fall. Also, if people think prices might peak in Q3/Q4, they might decrease import buys – which could, somewhat counterintuitively, serve to extend the cycle. And what if labor negotiations between the United Steelworkers union, U.S. Steel, and Cleveland-Cliffs result in a strike or lockout?

We’ll no doubt pick those topics up again in August, when Timna will join Josh Spoores, research principal of steel at CRU, and John Anton, director of pricing and purchasing at S&P Global, on the stage at Steel Summit. (More than 800 people have already registered. You find the latest agenda here and register here.)

In the meantime, this much is certain: sentiment is a lot more bullish now than it was last year. Also, people expect sheet prices to go significantly higher between now and Summit.

Let’s recall where we were last June. A new, 50% 232 had failed to provide an immediate jolt to the market. Mills had announced price targets of $900/st (Nucor) and $950/st (Cleveland-Cliffs). But they were at the same time selling in the $800s/st. By late summer/early fall, they were in the $700s/st. And in our surveys, we were asking when prices might bottom – something we haven’t asked at all in 2026.

While I’ve been saying in recent months people expect prices to continue to grind higher, that might be understating what’s happening now. CR and coated prices have been moving up faster than Nucor’s CSP, which had metered sheet prices for much of the year. And, increasingly, HR seems to be doing so as well.

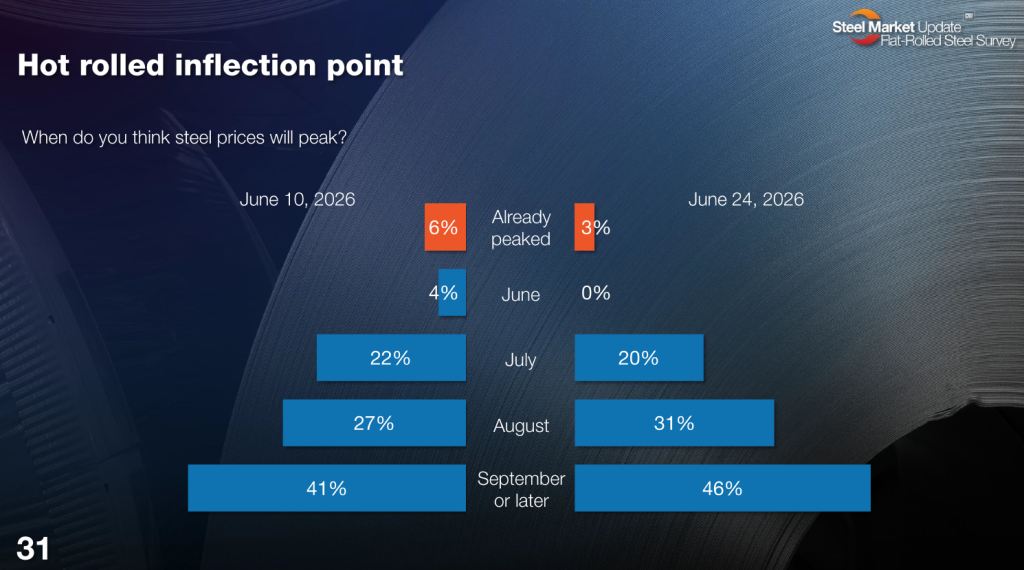

For much of this year, when we asked people when prices would peak, they’d say next month. That’s no longer the case.

The most common response in June has been prices won’t peak until September or later.

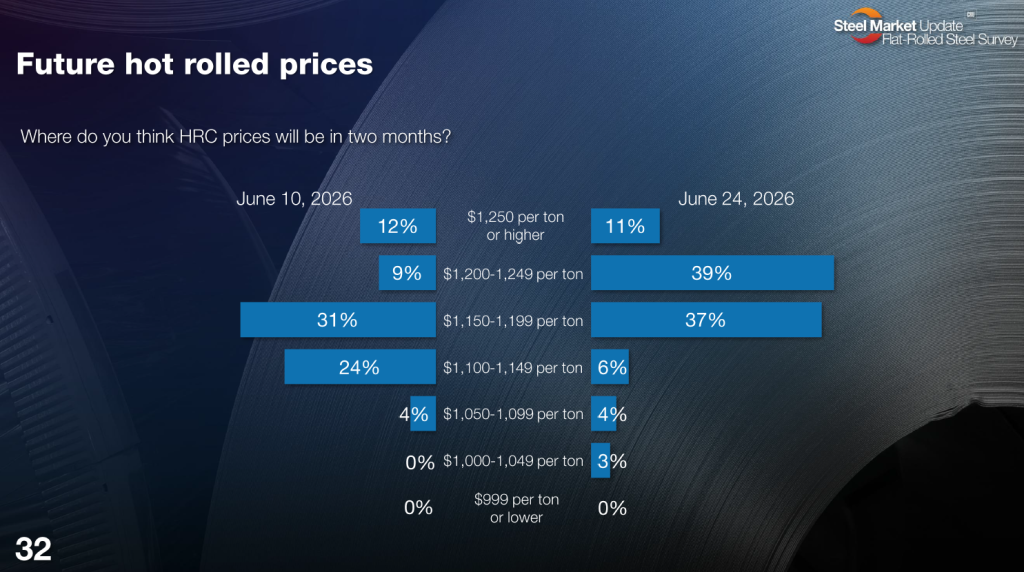

Similarly, for much of this year, people have been telling us HR prices in two months will be roughly where they are now – maybe a little higher.

Expectations now are more bullish. SMU’s HR prices stands at $1,145/st on average. And approximately half of survey respondents think prices will be above $1,200/st in two months, up from just 21% who thought that a mere two weeks ago.

I don’t think we’re close to a peak yet. Like I said at the top, service center inventories are at their lowest point since 2021. And it takes a lot longer than a month to restock, especially with lead times as long as they are.

Rewind to 2021. Service center sheet inventories bottomed out at 40 days of supply in January. They didn’t get above 50 days of supply until July. And HR prices didn’t start falling (from nearly $2,000/st!) until mid-September.

Or, since it’s road-trip season, let’s just say it looks like there’s still gas in the tank when it comes to prices.

That said, a veteran steel industry analyst once told me (during a steep downturn) that the market tends to rebound just when everyone has thrown in the towel. He said the reverse is also true. The market tends to fall when even the most bearish of bears have become bulls. That’s not exactly a data driven way of looking at things. But I always keep it in the back of my mind.