Analysis

June 26, 2026

HSS consolidation enters its next chapter

Written by Laura Miller

Consolidation continues in the HSS (hollow structural sections) sector, with two big deals announced just this month.

At the beginning of June, Zekelman Industries reported that its Atlas Tube subsidiary had agreed to form a joint venture with Maruichi USA. Details of the agreement have yet to be revealed, except to say the JV will combine the operations of Atlas Tube and Maruichi USA under Atlas Tube’s management. (Could it look like Zekelman’s joint venture with Maverick Pipe, announced in 2024? Zekelman Industries declined to comment further on the JV at this time.)

The second deal came mid-month, when Bull Moose Tube Co. revealed it had agreed to acquire Hanna Steel Corp. When the deal is finalized, it will add to its portfolio structural and mechanical tubing operations in Tuscaloosa, Ala., and Pekin, Ill., and a coating facility in Fairfield, Ala.

Both deals involve private, independent companies; therefore, financial figures have not been disclosed.

Bull Moose Tube did not respond to a request for comment.

History of consolidation in HSS

Neither Zekelman, Bull Moose, nor the larger HSS sector is a stranger to consolidation.

Zekelman and Atlas’s history is one of mergers. Zekelman’s roots date back to 1877, when the John Maneely Co. was founded as a pipe distribution company. Atlas Tube was formed by Harry Zekelman in 1984 and merged with John Maneely Co. in 2006. The Zekelman family then took full control of the JMC Steel Group in 2011 and, in 2016, unified all its operating divisions under the name Zekelman Industries. Zekelman added to Atlas’s portfolio with the acquisitions of American Tube in 2017 and EXLTUBE in 2022, and with a new ERW mill in Blytheville, Ark., in 2022. Today, Atlas Tube rolls more than 1.2 million tons per year at six facilities in the US and one in Ontario, Canada.

Bull Moose Tube was founded in 1962 and, four years later, was acquired by the London-based Caparo Group, of which it remains a part today. Last year, the company acquired Ferrous 85” Co., a toll processor whose assets included a major operation located on the campus of Steel Dynamics Inc.’s Sinton, Texas, sheet mill and adjacent to Bull Moose’s 350,000-ton-per-year HSS and sprinkler pipe mill, which started operations in 2023. Today, Bull Moose operates seven manufacturing locations in the US, not including Hanna Steel.

This latest round of consolidation follows another pre-pandemic one.

In 2016, Nucor Tubular Products upped its game in HSS with two big acquisitions. It acquired four facilities with an annual production capacity of 600,000 tons from Independence Tube for $435 million, and 240,000 tons of capacity from Southland Tube for $130 million.

In 2008, Japan’s Maruichi Steel Tube acquired Leavitt Tube, creating Maruichi Leavitt, which today operates out of Chicago with an annual production capacity of 250,000 tons.

As for other independent HSS producers, a few remain: Alliance Tubular Products, an Alliance Steel company, headquartered in Chicago; HW Metals of Tualatin, Ore.; James Steel, based in Madison Heights, Mich.; Searing Industries out of Rancho Cucamonga, Calif.; and Vest LLC, a subsidiary of JFE Shoji Trade America based in Vernon, Calif.

What’s the import/export story?

What do the HSS import and export markets look like at present?

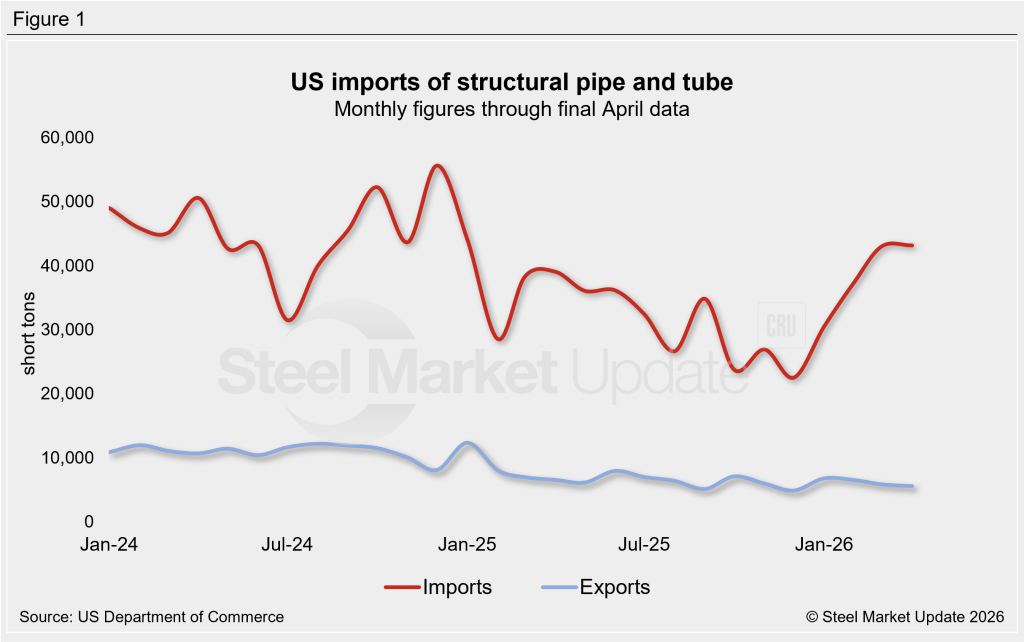

Structural pipe and tube imports had been trending downward throughout 2024 and 2025, according to US Department of Commerce data. Across 2024, structural P&T imports averaged 45,404 short tons (st) per month. In 2025, that figure dropped to 32,444 st. However, the trend reversed at the start of 2026, with imports picking up again, averaging 39,015 st in the first five months of the year (counting final figures through April and May license figures).

Canada is the largest supplier of US structural P&T imports. In 2025, its average monthly shipments fell 25.8% to 17,636 st. Through May licenses, however, its shipments have picked up again, rising 29.5% to a monthly average of 22,831 st.

Mexico has fallen to third place as a supplier of foreign structural tube. Its monthly shipments fell by a third in 2025 and are down another 34% so far this year.

Meanwhile, shipments from South Korea are trending higher this year. Last year, they fell 15% y/y to a monthly average of 4,195 st. So far this year, they’ve averaged 7,492 st each month, an increase of 78.6% from last year.

Interestingly, US exports of structural P&T have been on the decline since early 2025.

In 2024, exports averaged 11,011 st per month. They fell 36% in 2025 to a monthly average of 7,066 st. And through April, the latest month for which figures are available, they’re down another 12% to 6,206 st per month on average.