Market Data

June 30, 2026

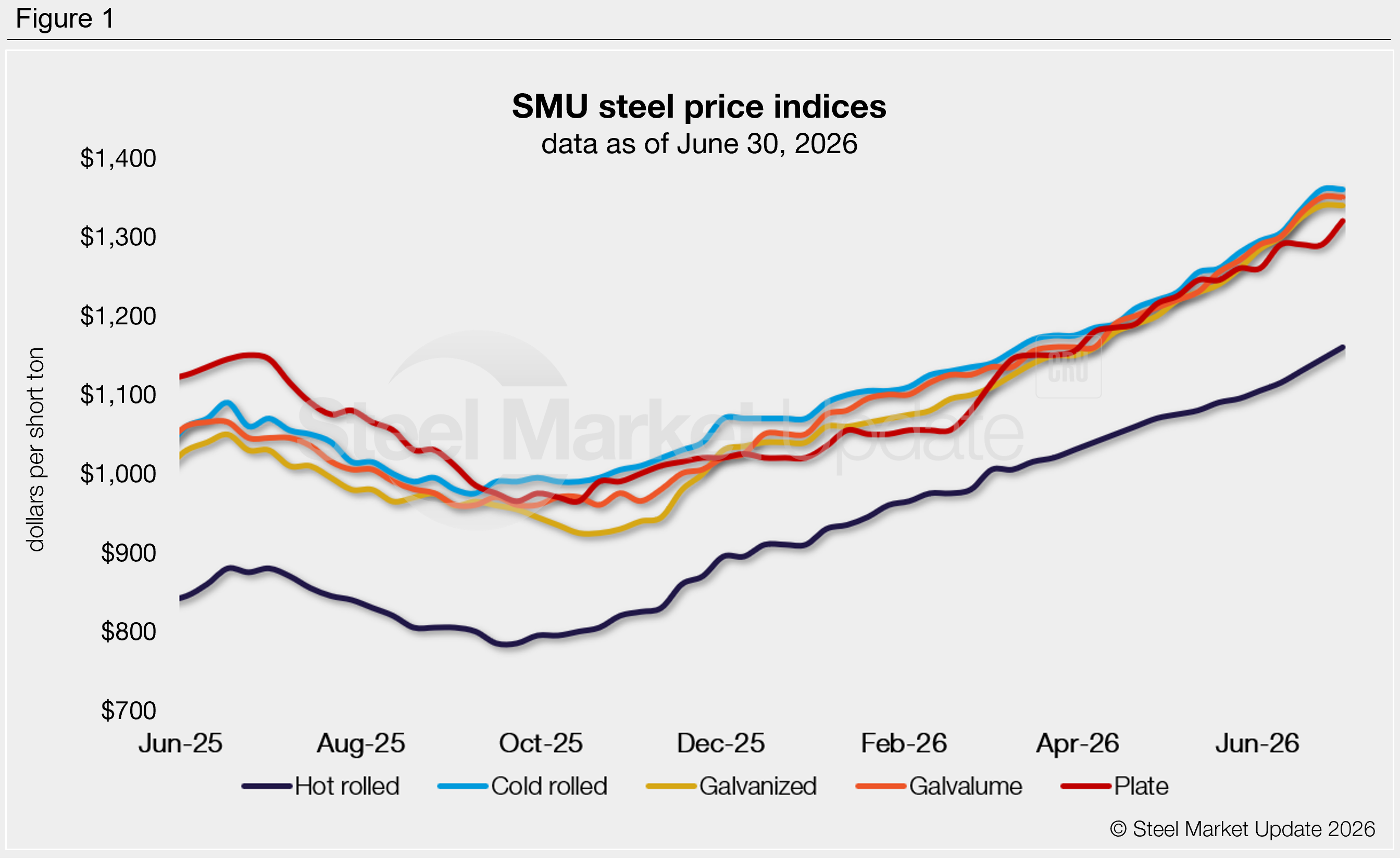

SMU Price Ranges: HR and plate up, CR and coated hold steady

Written by Brett Linton & Michael Cowden

Hot-rolled (HR) coil and plate prices continued to tick higher even as cold-rolled (CR) and coated prices came in unchanged, according to SMU’s latest check of the market.

Nucor keeping its consumer spot price (CSP) for hot-rolled (HR) coil unchanged made waves in futures and equities markets. But physical market participants said they’d seen no change in underlying conditions of tight supplies and stable/good demand. And some said Nucor’s goal might have been to slow price gains out of concern about increased import volumes.

Also notable: Market participants said one large domestic mill has had more spot availability recently. Some said the increased availability might result from typical summertime automotive shutdowns. Others said it could stem from the steelmaker favoring higher priced spot tons over lower, fix-priced contract volumes. (Such fixed-price contracts are typically heavily tilted toward automotive customers.)

All told, SMU’s HR price stands at $1,160 per short ton (st) on average, up $15/st from last week and up $55/st from a month ago. Current HR prices now match the highwater mark recorded in 2023, according to our price archives. Any additional gains would put them in territory not seen since 2022 in the aftermath of Russia’s full-scale invasion of Ukraine.

Cold-rolled, galvanized, and Galvalume base prices, meanwhile, remained unchanged at $1,360/st, $1,340/st, and $1,350/st, respectively.

Plate prices rose $30/st week over week to $1,320/st on average. They’re at their highest level since February 2024.

SMU’s price momentum indicator remains at higher for both sheet and plate products, signaling that we expect prices to increase further in the short term.

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil: $1,120–1,200/st, averaging $1,160/st

The lower end of our range is unchanged week over week (w/w), while the top end is up $30/st. Our overall average is up $15/st w/w.

Hot-rolled lead times range from 6–12 weeks, averaging 7.7 weeks as of our June 25 market survey.

Cold-rolled coil: $1,320–1,400/st, averaging $1,360/st

Our range is unchanged w/w.

Cold-rolled lead times range from 7–12 weeks, averaging 9.3 weeks through our latest survey.

Galvanized coil: $1,300–1,380/st, averaging $1,340/st

Our range is unchanged w/w.

Galvanized .060×48” G90 benchmark: SMU price range is $1,399–1,479/st, averaging $1,439/st FOB mill, east of the Rockies. Note that this spec includes $99/st in mill extras, and extras may vary by mill.

Galvanized lead times range from 7–11 weeks, averaging 9.0 weeks through our latest survey.

Galvalume coil: $1,300–1,400/st, averaging $1,350/st

Our range is unchanged w/w.

Galvalume .0142×42” AZ50, grade 80 benchmark: SMU price range is $1,900–2,000/st, averaging $1,950/st FOB mill, east of the Rockies. Note that this spec includes $600/st in mill extras, and extras may vary by mill.

Galvalume lead times range from 8–11 weeks, averaging 8.5 weeks through our latest survey.

Plate: $1,290–1,350/st, averaging $1,320/st

The lower end of our range is up $50/st w/w, while the top end is up $10/st. Our overall average is up $30/st w/w.

Plate lead times range from 6–12 weeks, averaging 8.0 weeks through our latest survey.

Brett Linton

Read more from Brett Linton