Final Thoughts

A tariff on Brazilian pig iron could cause great upheaval in the market.

A tariff on Brazilian pig iron could cause great upheaval in the market.

Steel prices continued to decline this week across all of the sheet and plate products tracked by SMU, pressured by short lead times and the typical summer slowdown.

Galvanized steel prices ping-ponged in the $50/hundredweight range during the month of July, settling in at roughly the same position as in June.

Institute for Supply Management CEO Tom Derry will join SMU for our next Community Chat on Wednesday, July 23, at 11 a.m. ET (10 a.m. CT). You can register here.

SMU’s Mill Order Index (MOI) rebounded in June after declining for three straight months. The gain complemented a modest boost in service center shipments for the month, according to our latest service center inventories data.

Domestic steel mill output edged lower last week, according to the American Iron and Steel Institute (AISI). While down, production remains historically strong since peaking in early June.

Nucor is lowering its list price for spot hot-rolled coil for the first time since May 27.

What to look out for regarding ferrous scrap ahead of Steel Summit.

Drilling activity increased in both the US and Canada for the week ended July 18, according to the latest data from Baker Hughes.

Section 232 tariffs have doubled to 50%. Reciprocal tariffs rates remain uncertain. But while prices have softened on even softer sentiment, tariffs have firmed the floor.

US housing starts recovered slightly in June after reaching a five-year low the month prior, according to figures recently released by the US Census Bureau.

Tariff threats on Brazil aren't just hitting steel products. Aluminum is also feeling the heat.

Cold-rolled (CR) coil prices continued to tick lower in the US this week, with a similar trend seen in offshore markets.

Chinese steel export prices are expected to rise and support prices across most of Asia in the coming month. In Europe, buyers are likely to frontload import orders ahead of CBAM imposition, while new trade agreements are likely to emerge in the US. Steel prices in the APAC are expected to rise, except in India […]

We have a special addition to the agenda of this year's SMU Steel Summit that I’m excited to announce today. U.S. Steel President and CEO David Burritt will speak on the opening day of the Summit about the partnership between the iconic Pittsburgh-based steelmaker and Nippon Steel.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market events.

All districts reported “experiencing modest to pronounced input cost pressures related to tariffs, especially for raw materials used in manufacturing and construction.”

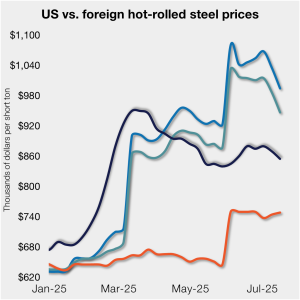

Stateside prices continue to trail imports from Europe, supported by Section 232 steel tariffs that were doubled in early June.

The volume of finished steel entering the US market remained elevated in May, in line with April figures, according to SMU’s analysis of Department of Commerce and American Iron and Steel Institute (AISI) data

Flat rolled = 55.8 shipping days of supply Plate = 59.4 shipping days of supply Flat rolled US service centers’ flat-rolled steel supply edged down in June with a modest boost to shipments month on month (m/m). At the end of June, US service centers carried 55.8 shipping days of flat roll supply, down from […]

Is outer space steel's final frontier?

US sheet and plate prices were flat or lower as reduced import volumes were offset by so-so demand.

Turkish scrap prices were unchanged week over week (w/w), with HMS and Shredded grades assessed at $340 and $355 per metric ton (mt) CFR, respectively.

Nucor is holding its list price for spot hot-rolled coil at $910 per short ton (st), unchanged since June 30.

President Trump’s tariff policies have a lot more in common with a roundabout than you’d think.

A roundup of steel industry news that happened this week, as reported by Steel Market Update.

Both current and future scrap sentiment jumped this month, though survey participants reported responses before key trade news was announced.

Heating and cooling equipment shipments grew from April to May, according to the latest data released by the Air-Conditioning, Heating, and Refrigeration Institute (AHRI).

CRU Principal Analyst Shankhadeep Mukherjee expects a restocking cycle for steel sheet products in most parts of the world due to either low inventories or seasonally stronger demand.

The commercial vehicle sector is showing signs of fatigue, but you wouldn’t know it at first glance of the latest government figures.