Manufacturing in New York state improves again in August

Business activity in New York state improved modestly in August. It was just the second positive reading for the general business conditions index in six months.

Business activity in New York state improved modestly in August. It was just the second positive reading for the general business conditions index in six months.

While boarding Airforce One on Friday, US President Donald Trump stated that he would be setting more steel tariffs and putting ~100% tariffs on semiconductors and chips.

The CRUmpi rose by 0.8% month over month (m/m) to 286.1 in August, following four consecutive months of decline. Scrap prices showed mixed trends across major regions, largely influenced by local supply-and-demand dynamics, government policies, and the relative strength of finished steel markets. US prices were stable while Europe and Asia saw price increases, but […]

Hardly a day goes by without someone writing about the expected rise in US electricity demand. This demand is largely driven by data center and AI’s appetite for power.

In July, US service centers’ flat-rolled steel supply increased month on month, following the seasonal summer trend of inventory build with slowing shipments.

Market participants said they have high hopes that the stable hot-rolled spot market will improve as the year rolls on.

On Monday and Tuesday of this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

All five of SMU's steel sheet and plate price indices declined this week, falling to lows last seen in February.

The amount of finished steel coming into the US market increased 3% from May to June, climbing to one of the highest rates seen in recent years, according to SMU’s analysis of Department of Commerce and American Iron and Steel Institute (AISI) data

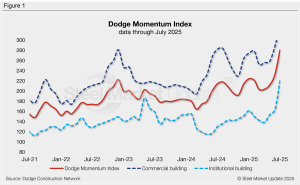

The Dodge Momentum Index (DMI) jumped 20.8% in July and is now up 27% year-to-date, according to the latest data released by Dodge Construction Network.

This week’s SMU survey reveals that a growing number of steel market participants are weary of tariffs and are awaiting evidence of progress reshoring. At the start of 2025, now-second-term President, Donald Trump, pronounced that his plan to implement tariffs would result in increased revenue for the US.

Both SMU Sentiment Indices continue to show that buyers remain optimistic for their company’s chances of success, though far less confident than they felt earlier in the year.

SMU’s Aug. 8, 2025, steel buyers market survey results are now available on our website to all premium members.

SMU’s Monthly Review provides a summary of our key steel market metrics for the previous month, with the latest data updated through July 31.

Mill production times for sheet products are holding just above multi-year lows, while plate lead times remain elevated.

Most steel buyers continue to report that mills are open to negotiating spot prices. Negotiation rates have remained high for most of the past three months.

Current and future scrap sentiment indices declined this month, according to SMU’s latest ferrous scrap survey data.

SMU’s August ferrous scrap market survey results are now available on our website to all premium members.

Sheet and plate prices were either flat or modestly lower this week on softer demand and increasing domestic capacity.

Truchas works in Lazaro Cadenas, Michoacan, western Mexico. Repairs may take up to six months.

US manufacturing activity slowed again in July to a 10-month low

While US construction markets are far from uniform, recent indicators from June and July paint an unusually fragmented picture.

Several EU member states have published a ‘non-paper’ that puts forward proposals for a post-safeguard trade measure.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

The Steel Demand Index now stands at 42, up from 38.5 in early July, but off from a four-year high of 65.0 in late February.

Sheet prices slipped again this week amid discounting from certain mills and ongoing concerns about demand.

Chief executive of the Institute for Supply Management (ISM), Tom Derry highlighted how reactive buying behavior has shifted the market into a quiet demand period. Derry presented ISM data during the weekly SMU community chat.

SMU’s Steel Buyers’ Sentiment Indices eased this week, both approaching multi-year lows.

SMU’s latest steel buyers market survey results are now available on our website to all premium members.

US tariff expansion to stainless material in imported downstream products will not be enough on its own to incentivize capital investment