US scrap tags increase in December

US ferrous scrap prices have picked up in December, sources told SMU.

US ferrous scrap prices have picked up in December, sources told SMU.

Domestic raw steel production marginally declined last week, according to the latest data released by the American Iron and Steel Institute (AISI).

SMU’s December ferrous scrap market survey results are now available on our website to all premium members.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

Domestic steel shipments dropped in October vs. September, but increased year over year.

Metalforming manufacturers were mixed in their outlook, anticipating business conditions could either worsen or, at best, hold in the near-term, according to PMA's November report.

Sources expect the recent spot market price hikes on domestically produced plate products to be accepted by the market.

The volume of raw steel produced by US mills eased last week, according to the latest figures released by the American Iron and Steel Institute (AISI).

The Chicago Business Barometer tumbled to an 18-month low in November, according to Market News International (MNI) and the Institute for Supply Management (ISM)

The Institute for Supply Management’s (ISM) latest report reflects the dim market conditions reported by US manufacturing executives in November.

SMU’s Current Steel Buyers’ Sentiment Index improved this week as Future Sentiment inched up as well, according to our most recent survey data.

US and Canadian rig counts both declined this week, according to the latest Baker Hughes data released on Wednesday, Nov. 26.

SMU’s latest steel buyers market survey results are now available on our website to all premium members.

Steel mill lead times extended this week on all sheet and plate products tracked, according to responses from SMU’s latest market survey.

All five of SMU’s sheet and plate price indices increased this week for the second week in a row, with all products inching up to new multi-month highs. Prices are now up by $30-70/st compared to those seen four weeks ago.

US steel imports declined considerably in September and October, with trade falling to reduced levels not seen in nearly five years.

German Economy Minister Katherina Reiche expressed frustration with US levies on steel and aluminum products. The US contends the EU is unfairly targeting its big tech firms.

Domestic steel production improved last week, according to the latest figures from the American Iron and Steel Institute (AISI).

Following four consecutive monthly declines, world crude steel output recovered 1% from September to October to an estimated 143.3 million metric tons (mt), according to the World Steel Association (worldsteel).

US and Canadian rig counts both improved this week, according to the latest Baker Hughes data.

Sources say domestic mill lead times and consumer spot prices have increased this week.

In the month since my last column, the tides have started to turn – and as usual it wasn’t the physical market that moved first.

Most steelmaking raw material prices remained stable over the past month. Prices are mixed in comparison to this time last year.

Domestic plate market participants anticipate strong economic growth in the first quarter of 2026, which they say is the perfect reason for spot market price hikes now.

Steel market chatter from our most recent survey.

Architecture firms reported a modest improvement in billings in October, though business conditions remained soft, according to the latest ABI report.

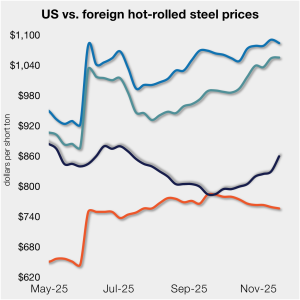

The price gap between stateside hot band and landed offshore product shrank week over week (w/w).

The SMU Steel Demand Index slackened from late October, remaining below expansion territory, according to SMU's mid-November indicators.

SMU’s price indices increased across the board this week, reaching new multi-month highs.

SMU’s Mill Order Index (MOI) surged in October after a notable decline the month prior. The recovery came as service center on order inventory totals picked up, supported by a slight uptick in shipments, according to our latest service center inventories data.