Ferrous export market seeks direction

The export market is looking for direction based upon the latest scrap purchases from Northern Europe by Turkish steelmakers. The sentiment was looking bearish, but sellers may see it differently.

The export market is looking for direction based upon the latest scrap purchases from Northern Europe by Turkish steelmakers. The sentiment was looking bearish, but sellers may see it differently.

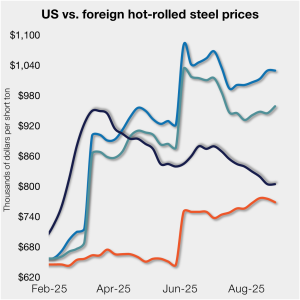

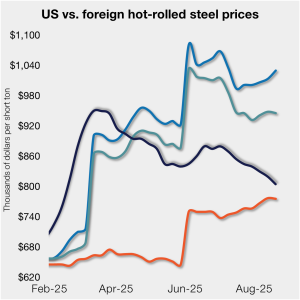

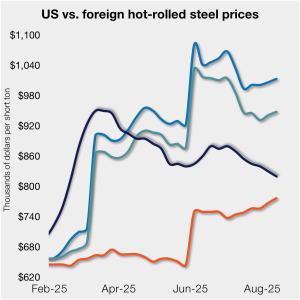

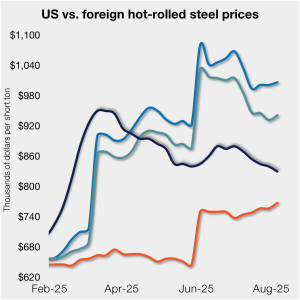

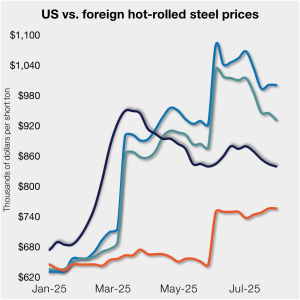

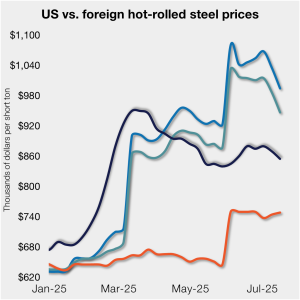

Domestic hot-rolled (HR) coil prices were flat this week, while offshore prices varied week over week (w/w). The price margin between stateside and foreign product was little changed as a result.

On Thursday, the U.S. and EU agreed to more concrete terms to their handshake deal of last month.

Domestic sheet prices in the US remained under pressure, limiting interest in imports, while domestic prices for longs products continued to rise.

HRC prices in the US eroded further last week, while offshore prices varied week over week (w/w), widening the price margin between stateside and foreign product.

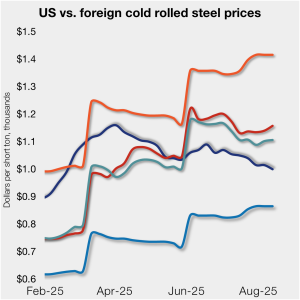

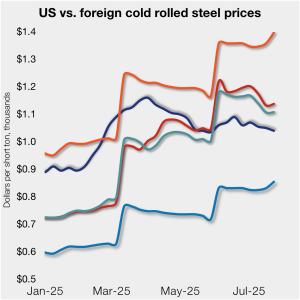

Cold-rolled (CR) coil prices continued to decline in the US this week, while prices in offshore markets diverged and ticked higher.

The CRUmpi rose by 0.8% month over month (m/m) to 286.1 in August, following four consecutive months of decline. Scrap prices showed mixed trends across major regions, largely influenced by local supply-and-demand dynamics, government policies, and the relative strength of finished steel markets. US prices were stable while Europe and Asia saw price increases, but […]

The US scrap export market has traded sideways or slightly less for about 60 days, with no real firmness in sight.

Hot-rolled (HR) coil prices in the US declined again last week, while offshore prices ticked higher again week over week (w/w).

The administration continues to negotiate deals with US trading partners, and the reciprocal tariff program appears poised for further modification. This week, we focus on other important developments that may have received less media attention.

Hot-rolled (HR) coil prices in the US declined again last week, while offshore prices increased week over week (w/w).

This week’s SMU survey reveals that a growing number of steel market participants are weary of tariffs and are awaiting evidence of progress reshoring. At the start of 2025, now-second-term President, Donald Trump, pronounced that his plan to implement tariffs would result in increased revenue for the US.

What the word "sideways" means can depend on where you sit on the procurement spectrum.

The ferrous scrap export market off the US East Coat and Gulf Coast has remained basically sideways over the last month. This mirrors the lack of movement in the US domestic market.

Several EU member states have published a ‘non-paper’ that puts forward proposals for a post-safeguard trade measure.

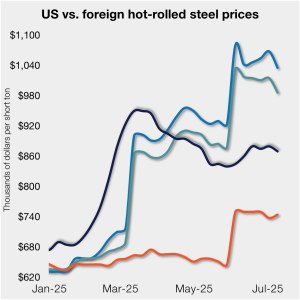

Hot-rolled (HR) coil prices in the US edged lower again this week, while offshore price were little changed. Stateside prices continue to trail imports from Europe, supported by Section 232 steel tariffs.

US and European steel trade groups were at odds over their reaction to the recent trade deal President Trump brokered with the EU.

GrafTech International attributed its second-quarter net loss to a non-cash tax expense and lower weighted average realized prices.

As the president’s August 1 tariff deadline approaches, the “Let’s Make a Deal” game show returns to primetime (the Monty Hall version, of course). As the administration begins rolling out trade deals, we are starting to see what’s behind door number one and who is getting a “zonk.”

With 30 years of experience at Steel Dynamics, Barry Schneider reflects on the company and the state of the steel industry.

Cold-rolled (CR) coil prices continued to decline in the US this week, while prices in offshore markets ticked higher.

Is there any clarity to be hoped for on the tariff front?

Hot-rolled (HR) coil prices in the US edged lower again this week but have remained in a tight band for roughly four months. Stateside prices continue to trail imports from Europe, supported by Section 232 steel tariffs that were doubled in early June.

Cold-rolled (CR) coil prices continued to tick lower in the US this week, with a similar trend seen in offshore markets.

Chinese steel export prices are expected to rise and support prices across most of Asia in the coming month. In Europe, buyers are likely to frontload import orders ahead of CBAM imposition, while new trade agreements are likely to emerge in the US. Steel prices in the APAC are expected to rise, except in India […]

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market events.

Stateside prices continue to trail imports from Europe, supported by Section 232 steel tariffs that were doubled in early June.

President Trump's threatened tariffs on Brazil, USMCA partners, and Europe could shake up the scrap and pig iron markets in August.

CRU Principal Analyst Shankhadeep Mukherjee expects a restocking cycle for steel sheet products in most parts of the world due to either low inventories or seasonally stronger demand.

Hot-rolled (HR) coil prices in the US ticked down this week but have fluctuated little over the past month. Stateside tags continue to trail imports from Europe, supported by Section 232 steel tariffs that were doubled in early June.