Miller on Ferroalloys: Tariff confusion

How is the ferroalloys market in the US faring with the new tariffs.

How is the ferroalloys market in the US faring with the new tariffs.

Following eight consecutive weeks of declines, sheet and plate prices saw some upward movement this week in the wake of last Friday’s Section 232 tariff increase announcement. Gains varied by product.

The speed and scale of recent moves are reminders of just how sensitive HRC futures remain to structural shifts and sentiment cues.

Nucor halted a four-week decline in its spot price for hot-rolled coil this week, maintaining its weekly consumer spot price (CSP) at $870/st.

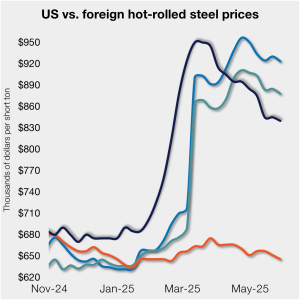

The price premium of galvanized coil over hot-rolled (HR) coil has narrowed over the past two months, resuming the downward trend seen for most of the last year. As of May 27, the spread between these two products is at one of its lowest levels in nearly two years.

CRU analysts discuss how downward pressure on the US premium has persisted due to weakness in key consuming sectors, while concerns over zinc supply have been largely alleviated for the time being.

The evolution of the U.S. HRC futures curve since my last update on April 17 tells a familiar story: fleeting optimism giving way to renewed caution.

Domestic hot-rolled coil prices moved lower again, maintaining the downward move seen in eight of the last 10 weeks.

The US mills have managed to reduce pig iron prices to correspond with the sharp declines in domestic scrap prices in May.

Sheet and plate prices marginally declined again this week for the second consecutive week, pausing the strong downward trend seen from April through early May.

Nucor has lowered its consumer spot price (CSP) for hot-rolled coil by $10 per short ton (st), marking the fourth consecutive weekly decrease.

Which way will the herd move?

Most sheet and plate prices edged lower again this week, albeit at a slower pace compared to the movements seen over the last seven weeks. Buyers remain cautious and hesitant to hold onto much inventory, citing lingering demand concerns, ongoing tariff uncertainty, and a potentially weakening scrap market in June.

Market participants in both the US and Europe noted that most buyers are patiently waiting for prices to reduce as they have enough inventory at hand.

All of SMU’s sheet and plate steel price indices declined this week, easing by $30-40 per short ton (st) on average since early May. Prices continue to slide lower as buyers remain on the sidelines, wary of holding much excess inventory and expecting further declines.

The price spread between hot-rolled coil (HRC) and prime scrap narrowed again in May, according to SMU’s most recent pricing data.

Since the US ferrous scrap settlements for May have been finalized, steelmakers are turning their attention to continued pig iron flows with the wind behind their backs.

Nucor lowered its weekly spot price for hot-rolled (HR) coil for a second straight week, down $10 per short ton (st), after keeping it in a holding pattern for most of April.

Despite the hand-wringing and head-scratching about the impact of President Trump’s tariff policy, the HRC futures market has been relatively subdued since our last writing of this article.

Steel buyers said Nucor’s price decrease was a public acknowledgement of what most of the market had already known - that sheet prices were moving lower in a more significant way. The question now is whether mills and service centers will manage the decline or whether prices might fall rapidly, they said.

Please take a moment to complete our short survey and share your views on how our prices, methodologies, and definitions can better support your work. Your feedback plays a key role in how we continue to serve you and the wider steel market.

After holding its weekly spot price for hot-rolled (HR) coil steady for three weeks at $930 per short ton (st), Nucor lowered the price this week by $20/st.

US cold-rolled (CR) coil prices edged lower again this week, slipping four weeks in a row now. Most offshore markets mirrored the move, ticking down marginally as well.

Most sheet and plate steel prices declined yet again this week, with four of SMU’s five indices moving lower.

Nucor’s weekly consumer spot price (CSP) for hot-rolled (HR) coil remained unchanged this week.

Chinese export prices for longs were almost steady this week, while those for flats generally declined as producers cut prices to secure deals.

The CME Midwest HRC futures market’s response to Trump’s election and subsequent comments about blanket 25% tariffs on Canada and Mexico was surprisingly counterintuitive.

SMU’s flat-rolled steel prices were flat or lower as tariff-related uncertainty continued to drag on the market.

The pig iron markets have been quiet for the last several weeks, as tariff implementation on imports into the US became a reality. There has been debate on which party will have to pay the tariff. A recent transaction could provide the answer to that question.

The market appears to be pausing after a turbulent run. But tension remains just beneath the surface. With net long positioning still elevated, sentiment-driven selling could quickly reignite volatility. Still, supply constraints and limited imports are laying the groundwork for a resilient physical market. This moment of calm feels more like a crossroads than a conclusion.