Market Data

March 18, 2025

SMU price ranges: HRC and plate steady as tandem products edge higher

Written by Brett Linton

Steel prices were stable to higher this week for the second consecutive week across the sheet and plate products tracked by SMU. Three of our price indices increased from the previous week, while two held firm.

Market sources continue to report steady buying activity and decent demand, though the tariff-induced buying frenzy appears to have slowed.

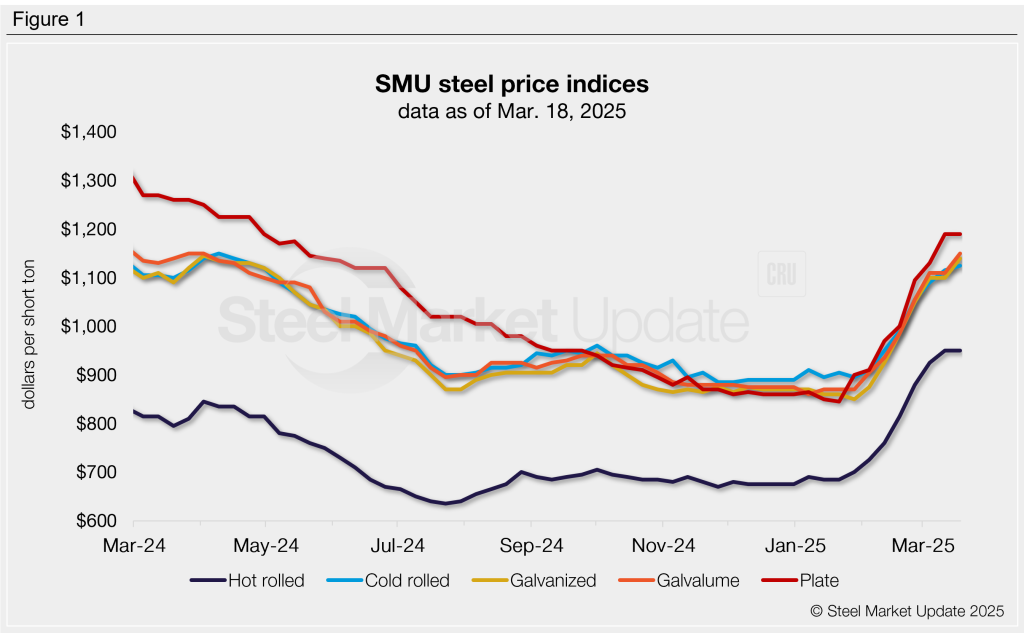

Hot-rolled coil prices held steady this week at a one-year high. Our plate index was also unchanged and remains at a 10-month high.

Meanwhile, cold-rolled coil and coated prices increased by $10-40 per short ton (st) from last week, climbing to levels last seen in April 2024.

SMU’s price momentum indicator remains at higher for all sheet and plate products, indicating we expect prices to increase in the short term.

Refer to Table 1 for the latest SMU steel price indices and how prices have trended in recent weeks.

Hot-rolled coil

The SMU price range is $900-1,000/st, averaging $950/st FOB mill, east of the Rockies. Our entire range is unchanged week over week (w/w). Our price momentum indicator for hot-rolled steel remains at higher, meaning we expect prices to increase over the next 30 days.

Hot rolled lead times range from 4-8 weeks, averaging 5.9 weeks as of our March 5 market survey. We will publish updated lead times on Thursday.

Cold-rolled coil

The SMU price range is $1,050–1,200/st, averaging $1,125/st FOB mill, east of the Rockies. The lower end of our range is unchanged w/w, while the top end is up $20/st w/w. Our overall average is up $10/st w/w. Our price momentum indicator for cold-rolled steel remains at higher, meaning we expect prices to increase over the next 30 days.

Cold rolled lead times range from 6-10 weeks, averaging 7.7 weeks through our latest survey.

Galvanized coil

The SMU price range is $1,080–1,200/st, averaging $1,140/st FOB mill, east of the Rockies. The lower end of our range is up $30/st w/w, while the top end is up $50/st w/w. Our overall average is up $40/st w/w. Our price momentum indicator for galvanized steel remains at higher, meaning we expect prices to increase over the next 30 days.

Galvanized .060” G90 benchmark: SMU price range is $1,177–1,297/st, averaging $1,237/st FOB mill, east of the Rockies.

Galvanized lead times range from 6-10 weeks, averaging 7.9 weeks through our latest survey.

Galvalume coil

The SMU price range is $1,100–1,200/st, averaging $1,150/st FOB mill, east of the Rockies. The lower end of our range is up $30/st w/w, while the top end is up $50/st w/w. Our overall average is up $40/st w/w. Our price momentum indicator for Galvalume steel remains at higher, meaning we expect prices to increase over the next 30 days.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,394–1,494/st, averaging $1,444/st FOB mill, east of the Rockies.

Galvalume lead times range from 6-10 weeks, averaging 8.0 weeks through our latest survey.

Plate

The SMU price range is $1,120–1,260/st, averaging $1,190/st FOB mill. Our entire range is unchanged w/w. Our price momentum indicator for plate remains at higher, meaning we expect prices to increase over the next 30 days.

Plate lead times range from 3-8 weeks, averaging 5.5 weeks through our latest survey.

SMU note: Above is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is also available here on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@steelmarketupdate.com.