October scrap market still up for grabs

The ferrous scrap market is still searching for clues about the direction of the October market.

The ferrous scrap market is still searching for clues about the direction of the October market.

Worthington Steel saw a strong first quarter to kick off its fiscal 2026 as both profits and sales notched increases.

August marked the second-lowest monthly production rate this year, down 13% from the two-year high of 166.6 million mt in March.

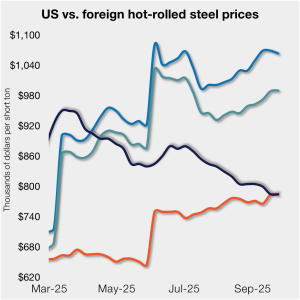

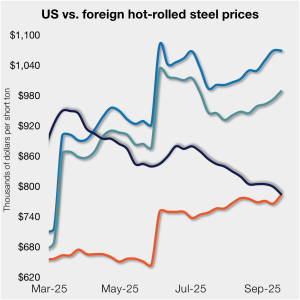

SMU’s average price for domestic hot-rolled (HR) coil held at $785 per short ton (st) this week, unchanged week on week (w/w). A similar dynamic was seen in offshore markets last week as well.

Are you ready to share what you'd like to see happen with the USCMA agreement when it comes up for joint review?

Sheet and plate prices were flat or lower this week as less discounting from domestic mills was offset by few signs of an anticipated rebound in demand.

US nonresidential building starts fell 5.4% in August, to a seasonally adjusted annual rate of $431 billion, according to the latest data released by Dodge Construction Network.

The analysis below was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com. One-in-three companies have paused or delayed stainless steel orders because of disruption caused by the wave of import duties imposed worldwide this year, according to a survey conducted for Outokumpu of Finland. Other responses include more […]

A compromise has been reached in the pig iron market, sources told SMU. Recall we reported US buyers were bidding $390 per metric ton (mt) FOB or less while sellers were holding sideways at about $400/mt.

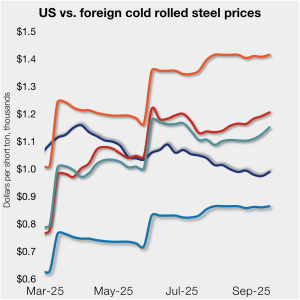

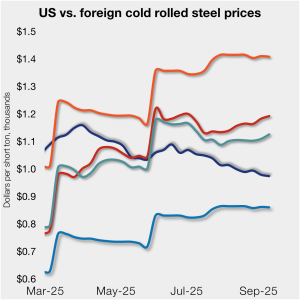

Cold-rolled (CR) coil prices ticked up in the US this week, matching a similar trend seen in offshore markets as well.

For the next month, CRU forecasts that global demand for steelmaking raw materials will increase month on month (m/m).

US rig counts continue to hover just above historic lows, while Canadian figures remain comparatively healthy.

SMU’s Steel Buyers’ Sentiment Indices diverged this week. The Current Steel Buyers’ Sentiment Index continued its recovery from the five-year low seen one month ago. Meanwhile, Future Buyers’ Sentiment gave back some of the ground gained in recent surveys.

With only a modest decline in US prices, HR imports, on a landed basis, remain much more expensive than domestic hot band.

Sheet times ticked higher but remain within days of multi-year lows, territory they have been in since May. Plate lead times have shifted lower in the past month but remain about a week longer than they were at this time last year.

Housing starts slowed in the US in August as affordability challenges and cautious builder sentiment weighed on new construction activity.

Sheet and plate buyers say mills remain open to negotiating spot prices this week, though less so than in recent weeks, according to SMU’s latest market survey.

The US Department of Commerce announced that its second window for submitting applications for the inclusion of derivative steel and aluminum products in Section 232 tariffs is now open, according to the US Federal Register. September’s Inclusion Window Sept. 15 through Sept. 29, applicants can email requests for inclusions to the Defense Industrial Base Programs. The first […]

SMU’s price ranges were mixed again this week as the market continues to seek a floor amid industry hopes for a Q4 rebound.

There have been developments in the ferrous scrap export market in the Atlantic Basin over the past week that point to weakness in the near future.

Steel Dynamics Inc. is bullish heading into the close of the third quarter, with all three of its operating segments tracking higher.

AHMSA is opening its doors to potential buyers to tour its steel plant and mining operations in northern Mexico in preparation for the next stage of its bankruptcy process: the auction of its assets.

Will a US-UK meeting next week prove a harbinger of tariff deals to come, or will it be just another case of having the rug pulled from under us?

Cold-rolled (CR) coil prices ticked lower in the US this week, while prices in offshore markets mostly diverged and ticked higher.

The pig iron market in Brazil is currently in flux and there have been few, if any, confirmed cargoes transacted for the US.

A recap of this week's steel industry news...

Rising Midwest and European premiums are giving Canadian aluminum producers a rare boost, restoring pricing power just ahead of key 2026 negotiations.

Sheet prices are expected to increase in the coming weeks in most markets. However, rising domestic capacity in the US, subdued demand in Europe, and high inventory levels in China and India will limit price near-term uptrend.

Active rig counts increased in both the US and Canada last week, according to figures released by Baker Hughes. Although rising, US counts continue to hover just above historic lows. Canadian figures remain comparatively healthy, rising to a six-month high this week. Total US rig counts climbed by two week over week (w/w) to 539. […]

International trade law and policy remain a hot topic in Washington and beyond this week. We are paying special attention to the ongoing litigation of the president’s tariff policies and the administration’s efforts to heighten trade enforcement.