SMU Survey: Most buyers say mills are willing to talk price

Most steel buyers continue to report that mills are open to negotiating spot prices. Negotiation rates have remained high for most of the past three months.

Most steel buyers continue to report that mills are open to negotiating spot prices. Negotiation rates have remained high for most of the past three months.

Current and future scrap sentiment indices declined this month, according to SMU’s latest ferrous scrap survey data.

Sheet and plate prices were either flat or modestly lower this week on softer demand and increasing domestic capacity.

A recent conversation with Tanners shows that many of us in this industry often end up here by accident but end up staying.

The ferrous scrap market for August appears to be settling sideways as the threats posed to the market in July have not materialized.

Truchas works in Lazaro Cadenas, Michoacan, western Mexico. Repairs may take up to six months.

We’re in the dog days of summer, and the question is whether the market will improve as lead times stretch into September. Your answer to that question might depend on where you are in the supply chain. And producers, it seems to me, are a lot more optimistic than consumers at the moment.

Prices for four of the seven steelmaking raw materials we track were unchanged from late June through the end of July, while two increased and one declined. Collectively, these material prices rose 1% month over month (m/m), but are down 3% compared to three months ago.

Drilling activity slowed in the US and Canada last week, according to the latest oil and gas rig count data released by Baker Hughes.

The ferrous scrap export market off the US East Coat and Gulf Coast has remained basically sideways over the last month. This mirrors the lack of movement in the US domestic market.

US manufacturing activity slowed again in July to a 10-month low

Several EU member states have published a ‘non-paper’ that puts forward proposals for a post-safeguard trade measure.

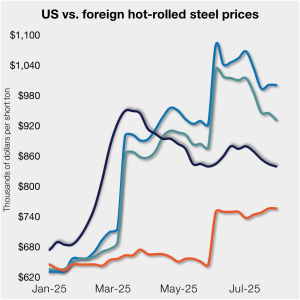

Hot-rolled (HR) coil prices in the US edged lower again this week, while offshore price were little changed. Stateside prices continue to trail imports from Europe, supported by Section 232 steel tariffs.

The cautious neutrality and summertime blues we discussed just a few weeks ago have evolved into something decidedly more bearish.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

ArcelorMittal expects less demand growth across most of the markets it operates in, including the US, because of President Donald Trump’s tariffs. But the Luxembourg-based steelmaker also thinks it stands to benefit from an increasingly regionalized world thanks to investments like the new EAF at its mill in Calvert, Ala.

Latin American steel producer Ternium delivered a solid performance in the second quarter of 2025. Performance was driven primarily by higher realized steel prices in Mexico, even as shipment volumes declined slightly across its regional portfolio.

The Trump administration has exempted Brazilian pig iron and iron ore from an aggressive "reciprocal" tariff ahead of the Aug. 1 deadline.

North American auto assemblies declined in June, down 10.6% vs. May. And, according to GlobalData, assemblies were 3.1% down year on year (y/y).

Sheet prices slipped again this week amid discounting from certain mills and ongoing concerns about demand.

US and European steel trade groups were at odds over their reaction to the recent trade deal President Trump brokered with the EU.

GrafTech International attributed its second-quarter net loss to a non-cash tax expense and lower weighted average realized prices.

Attorneys representing domestic petitioners and foreign respondent companies have been busy filing case briefings and making rebuttals as the corrosion-resistant steel unfair trade investigations begin to wind down.

The Brazilian pig iron community is playing defense ahead of the Aug. 1 deadline for a 50% US tariff on imports from the South American country. The moves indicate the Brazilian producers do expect the tariff to go into effect.

Is this just a severe case of the summer doldrums? Will demand improve in the fall, as it often does? Or has uncertainty around tariffs and the economy created a more lasting impact?

As the president’s August 1 tariff deadline approaches, the “Let’s Make a Deal” game show returns to primetime (the Monty Hall version, of course). As the administration begins rolling out trade deals, we are starting to see what’s behind door number one and who is getting a “zonk.”

Chief executive of the Institute for Supply Management (ISM), Tom Derry highlighted how reactive buying behavior has shifted the market into a quiet demand period. Derry presented ISM data during the weekly SMU community chat.

Drilling activity slowed in the US and increased in Canada last week, according to the latest oil and gas rig count data released by Baker Hughes.

SMU’s Steel Buyers’ Sentiment Indices eased this week, both approaching multi-year lows.

President Trump said a negotiated deal with Canada might not occur, and all existing tariffs, along with those set to take effect soon, will stay in place, according to media reports.