Despite trade chaos, Barry Schneider upbeat on SDI, steel

With 30 years of experience at Steel Dynamics, Barry Schneider reflects on the company and the state of the steel industry.

With 30 years of experience at Steel Dynamics, Barry Schneider reflects on the company and the state of the steel industry.

Algoma Steel applied to Canada’s federal Large Enterprise Tariff Loan (LETL) program for $500 million to support its long-term operations.

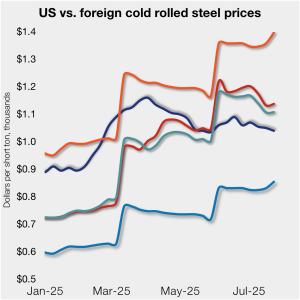

Cold-rolled (CR) coil prices continued to decline in the US this week, while prices in offshore markets ticked higher.

US tariff expansion to stainless material in imported downstream products will not be enough on its own to incentivize capital investment

Is there any clarity to be hoped for on the tariff front?

Steel mill lead times on sheet products contracted across the board this week compared to early July, while plate production times moderately extended, according to steel buyers responding to this week’s market survey.

More than nine out of every ten steel buyers polled by SMU this week reported that mills are negotiable on new order prices. Negotiation rates have increased in each of our last three surveys following the early-June lull, reaching a record high this week.

After a period of backwardation driven by headlines and CRU index anchoring, the CME HRC curve structure has undergone a notable shift.

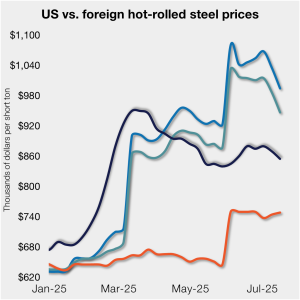

Hot-rolled (HR) coil prices in the US edged lower again this week but have remained in a tight band for roughly four months. Stateside prices continue to trail imports from Europe, supported by Section 232 steel tariffs that were doubled in early June.

The Architecture Billings Index (ABI), a leading indicator for non-residential construction activity, declined for an eighth straight month in June.

Steel Dynamics Inc. (SDI) executives called a 50% tariff on Brazilian pig iron “concerning,” but think tariffs will be a “mainstay” of trade agreements going forward.

Steel prices continued to decline this week across all of the sheet and plate products tracked by SMU, pressured by short lead times and the typical summer slowdown.

Galvanized steel prices ping-ponged in the $50/hundredweight range during the month of July, settling in at roughly the same position as in June.

SDI profits slipped in second quarter amid trade policy volatility.

Cleveland-Cliffs lost more than $400 million for the third consecutive quarter but predicted results would improve in the second half of the year. And shares of the Cleveland-based steelmaker surged after company executives said during its Q2 earnings call on Monday that they could make billions by courting foreign investors or selling assets.

What to look out for regarding ferrous scrap ahead of Steel Summit.

Drilling activity increased in both the US and Canada for the week ended July 18, according to the latest data from Baker Hughes.

The Chinese government has threatened countermeasures on Canada following the Canadian government's announcement on curbing steel imports, according to media reports.

Cold-rolled (CR) coil prices continued to tick lower in the US this week, with a similar trend seen in offshore markets.

Chinese steel export prices are expected to rise and support prices across most of Asia in the coming month. In Europe, buyers are likely to frontload import orders ahead of CBAM imposition, while new trade agreements are likely to emerge in the US. Steel prices in the APAC are expected to rise, except in India […]

Not much to report on from the sleepy HRC futures market in the thick of the summer doldrums with trading volume nearly grinding to a halt.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market events.

Canadian Prime Minister Mark Carney has announced new measures to limit steel imports into the country.

Stateside prices continue to trail imports from Europe, supported by Section 232 steel tariffs that were doubled in early June.

The Canada Border Services Agency has terminated a self-initiated dumping investigation of corrosion-resistant steel sheet (CORE) from Turkey.

Evraz NA and Welded Tube of Canada have lodged an unfair trade complaint against imports of OCTG, including those from USMCA trading partners Mexico and the US.

US sheet and plate prices were flat or lower as reduced import volumes were offset by so-so demand.

US steel exports rose 10% from April to May but remained low compared to recent years. This came just one month after exports fell to the lowest level recorded in nearly five years.

President Trump's threatened tariffs on Brazil, USMCA partners, and Europe could shake up the scrap and pig iron markets in August.

The volume of raw steel produced by US mills inched higher last week, according to the American Iron and Steel Institute (AISI). After steadily increasing in April and May, domestic mill output stabilized in early June and has remained historically strong since.