SMU's March at a glance

SMU’s Monthly Review provides a summary of our key steel market metrics for the previous month, with the latest data updated through March 31.

SMU’s Monthly Review provides a summary of our key steel market metrics for the previous month, with the latest data updated through March 31.

Raw steel mill output from US mills rebounded last week, according to the American Iron and Steel Institute (AISI). Production is now at the highest weekly rate recorded so far this year.

I’m not sure what I can write today that won’t be old news after April 2. The Trump administration has dubbed Wednesday “Liberation Day.” Since it’s mostly about tariffs, let’s just call it “Tariff Day.” Or maybe we should call it “Tariff Week” – since tariffs typically dominate the news cycle in the first week […]

Anticipation leading up to SMU’s Steel Summit 2025 is already heating up after last year’s record-setting attendance!

The constant flow of information we all receive can be a little overwhelming, but SMU is here to help with a snapshot of the week.

Crowe's Doug Schrock explains how to get up and running with AI at your company.

US rig counts remain slightly above multi-year lows, while Canadian activity is slowing following a seasonal peak.

A personal perspective on Galvalume prices from SMU analyst Brett Linton.

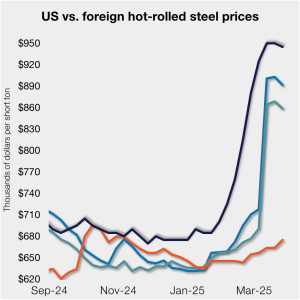

The threat of tariffs over the past two months has been a springboard for US prices. But the Section 232 reinstatement on March 13 narrowed the domestic premium over imports on a landed basis.

This week, SMU polled steel buyers on an array of topics, including market prices, demand, tariff policies, inventories, imports, and emerging market events.

After a March frenzy, are prices nearing a peak in April? Some of you have suggested that they are. Others think it's too early to make any such call.

SMU's steel price indices moved in differing directions this week but remained largely stable as cautious buyers await clarity on pending steel tariffs and trade cases.

After eight weeks of double-digit price increases on hot-rolled (HR) coil, Nucor slowed the price rise this week with an increase of $5 per short ton.

Have we hit a bit of a lull when it comes to the recent price bump? Mills certainly capitalized on the threat of tariffs and the unknown, with much that still could unfold.

Despite the economic and geopolitical upheaval of the last five years, CMC President and CEO Peter Matt points out that the construction market has been an essential element of the way forward.

SMU’s Buyers’ Sentiment Indices showed mixed movements this week but remain strong, reflecting continued confidence among steel buyers.

Are President Trump's tariff policies helping? Steel buyers offer their opinions on the impact of Trump's tariffs.

From the Smoot-Hawley Tariff Act of 1930 to George W. Bush's temporary 30% tariff, SMU takes a look at steel tariffs past.

After a multi-week increase, buyers responding to our market survey this week reported that lead times are stabilizing or marginally declining for each of the sheet and plate products we track.

The majority of the steel buyers responding to our latest market survey continue to report that domestic mills remain firm on pricing, showing little willingness to talk price on new spot orders this week.

In this Premium analysis we explore North American oil and natural gas prices, drilling activity, and crude oil stock levels.

Do recent actions by the EPA on deregulation signal a new course for the agency, and how could it affect steel?

Steel prices were stable to higher this week for the second consecutive week across the sheet and plate products tracked by SMU. Three of our price indices increased from the previous week, while two held firm.

The HRC vs. prime scrap spread increased again in March.

Raw steel mill production remains at one of the higher rates recorded so far this year.

Prices for five of the seven steelmaking raw materials tracked by SMU increased from February to March, according to our latest analysis.

This marks the eighth week of increases

Is a fissure opening up between manufacturers and the mills on President Trump's tariffs?

US rig counts continue to hover slightly above multi-year lows, while Canadian activity is entering a seasonal decline after recently reaching a seven-year high.

A quick way to catch up on what you might have missed.