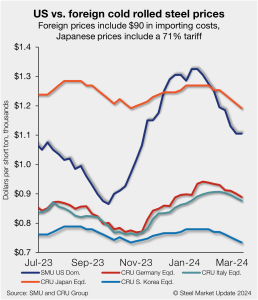

US CR tags still nearly 30% more than imports

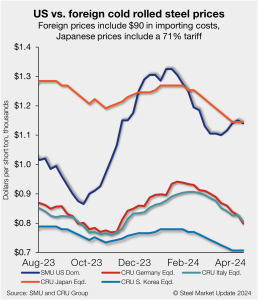

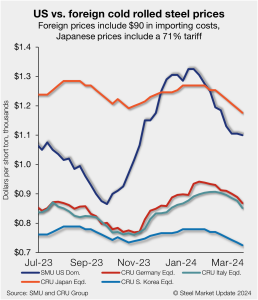

Foreign cold-rolled (CR) coil remains much less expensive than domestic product, according to SMU’s latest check of the market.

Foreign cold-rolled (CR) coil remains much less expensive than domestic product, according to SMU’s latest check of the market.

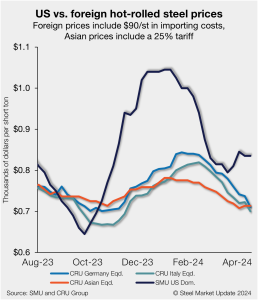

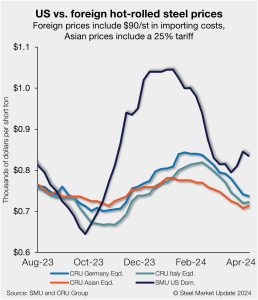

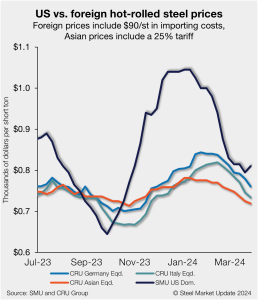

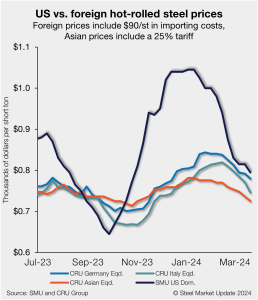

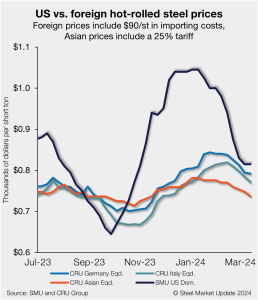

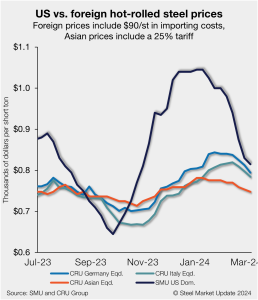

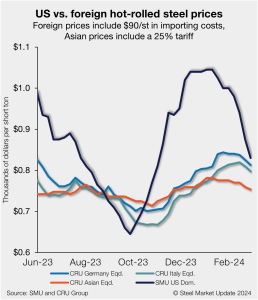

US hot-rolled (HR) coil remains more expensive than offshore hot band, though with a tighter premium as prices stateside and abroad have ticked lower in recent weeks.

Steel Dynamics Inc.'s (SDI's) earnings fell in the first quarter of 2024 as the company cited steel order volatility early in the quarter and lower scrap prices.

Cleveland-Cliffs’ chief Lourenco Goncalves and US Secretary of Energy Jennifer Granholm stressed the importance of the US steel industry and domestic manufacturing at Cliffs' Butler Works in Pennsylvania on Monday.

Foreign cold-rolled (CR) coil remains less expensive than domestic product, according to SMU’s latest check of the market.

Here’s a roundup of the latest news in the global aluminum market from our colleagues at CRU. Biden calls for tripling of Chinese steel and aluminum tariffs President Joe Biden is calling on the US Trade Representative (USTR) to consider increasing the existing section 301 import duty on Chinese steel and aluminum three-fold. The current […]

US hot-rolled (HR) coil has become gradually more expensive than offshore hot band in recent weeks, as stateside prices have stabilized while imports moved lower.

The Biden administration on Wednesday announced measures to support the domestic steel industry.

The steel market appears to be finding a new, higher normal with the shocks of the pandemic and the Ukraine in the rearview mirror. The good news: a more profitable and consolidated post-Covid US steel industry has been able to invest in operations. That includes efforts to decarbonize. The bad news: That “new normal” could be tested. Because it’s not just domestic sheet prices that have been volatile. Geopolitics are too.

The Department of Commerce (DOC) has issued new rules to combat evolving "unfair" trade practice — including the unfair trade of steel products. They go into effect on Wednesday, April 24.

U.S. Steel Corp.’s impending sale to Japan’s Nippon Steel Corp. (NSC) has cleared one hurdle: USS stockholders voted overwhelmingly in favor of the nearly $15 billion merger.

US hot-rolled (HR) coil has become increasingly more expensive than offshore hot band as stateside prices have moved higher at a sharper pace vs. imports.

The apparent supply of steel in the US fell 6% from January to February, according to data compiled from the Department of Commerce and the American Iron and Steel Institute (AISI).

They say all’s fair in love and war. But that doesn’t seem to be the case in steel. Being deemed “unfair” could get you slapped with shiny new Section 232 tariffs these days. Then again, “unfair” implies a judge. And people on opposing sides seldom agree with the judgment. Such seems to be the current case between the US and Mexico.

Cleveland-Cliffs’ Lourenco Goncalves said the company is still interested in acquiring U.S. Steel, though no bid is currently on the table, according to a local report.

US hot-rolled coil and offshore hot band moved further away from parity this week as stateside prices have begun to move higher in response to mill increases.

I can’t really define “Bidenomics” because it is so filled with contradictions. It seems to aim to increase manufacturing output in the United States. But not all increases are created equal.

There’s that concept from Adam Smith we all learn about in our Econ 101 classes: The Invisible Hand. A simple Google search will provide a refresh, but if memory serves I would classify it as something akin to “the market is magic” or “the market’s gonna market.” Today, obviously, we live in a mixed environment. There are a lot of hands out there, and they’re not too difficult to see. In this election year of 2024, one of the most visible hands out there probably belongs to the federal government.

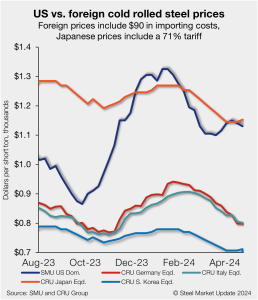

Foreign cold-rolled (CR) coil remains notably less expensive than domestic product even with repeated tag declines across all regions, according to SMU’s latest check of the market.

APAC steel prices are likely to bottom out in the near term as seasonally higher demand coupled with production cuts may support prices. In the EU, prices are likely to remain under pressure, while fresh price increases are expected in the US. APAC steel prices are likely to bottom out in the near term In […]

With Earth Day almost a month away, the world’s attention often turns to the manufacturing sector with calls for greener production processes.

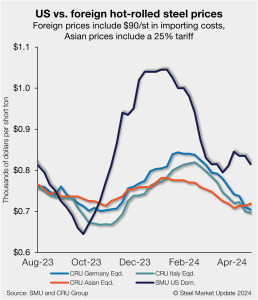

US hot-rolled coil (HRC) remains more expensive than offshore hot band but continues to move closer to parity as prices decline further. The premium domestic product had over imports for roughly five months now remains near parity as tags abroad and stateside inch down.

Foreign cold-rolled coil (CR) remains significantly less expensive than domestic product even as US tags continue to decline in a hurry, according to SMU’s latest check of the market.

US hot-rolled coil (HRC) remains more expensive than offshore hot band, even as domestic prices remain under pressure. The premium domestic product had over imports for roughly five months now remains near parity as tags abroad and stateside inch down.

The apparent supply of steel in the US increased in January, rising to a five-month high, according to data compiled from the US Department of Commerce and the American Iron and Steel Institute (AISI).

AM/NS Calvert CEO Chuck Greene has announced his retirement as CEO, effective March 15.

US steel mill shipments increased in January vs. December but fell from a year earlier,

US hot-rolled coil (HRC) is now just about 5% more expensive than offshore hot band. The premium domestic product had over imports for roughly five months is all but gone, and nearing parity.

The failure of the trade remedy actions against imported steel tin mill products (TMPs) continues to resonate. Cleveland-Cliffs and the United Steel Workers Union (USW) lost the case at the International Trade Commission (ITC) last month. A few days ago, the ITC released its final report explaining the decision against imposing antidumping and countervailing duties […]

The premium US hot-rolled coil (HRC) held over offshore product for roughly five months has nearly vanished. Domestic hot band prices continue to run downhill at a high rate, erasing a $300/st gap they had over imported HRC just two months ago.