SDI forecasts marked decline in Q2 earnings

Steel Dynamics Inc. guided to significantly reduced second-quarter earnings as its steel operations have taken a hit from lower prices.

Steel Dynamics Inc. guided to significantly reduced second-quarter earnings as its steel operations have taken a hit from lower prices.

U.S. Steel has guided to lower second-quarter earnings both sequentially and on-year in "dynamic" spot price market.

Nucor priced its weekly hot-rolled (HR) coil consumer spot price (CSP) at $715 per short ton (st) this week, down $5/st from last week.

The conventional wisdom is that sheet prices will trend down for the next few weeks (maybe the next two months) before rising again in August – around when lead times stretch into the busier fall months. We see that reflected in our survey results and in market chatter. And there are plenty of data points to choose from if you want to support of that position.

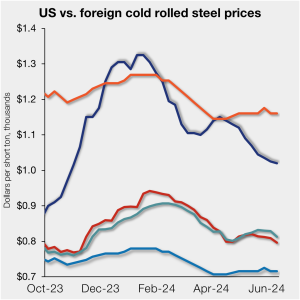

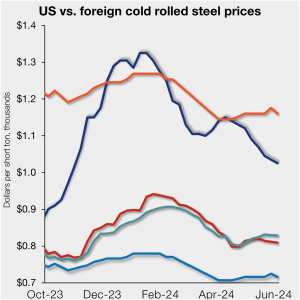

Offshore cold-rolled (CR) coil prices have changed little, but they are still notably cheaper than domestic product. That remains the case even as US CR coil prices ticked lower this week.

As the scrap market for June settles at lowered levels, let’s look at the situation for exports of ferrous scrap from the US East and Gulf coasts. Despite declines in the North American ferrous markets over the last two months, export prices have remained range-bound within a tight trading window. After a brief decline last […]

Pig iron prices have been trending higher in all key markets besides Europe. Limited exports from Brazil and Ukraine are contributing to higher prices in the USA, though soft demand cushioned a sharp price upswing. In the US, pig iron prices increased by $15 per metric ton (mt) m/m to $485/mt CFR NOLA. Buying activity […]

Nucor Corp. has guided to much lower second-quarter earnings, as profitability in its steel mills segment suffers due to lower prices and volumes.

The spread between hot-rolled coil (HRC) and prime scrap prices has narrowed for the second consecutive month, according to SMU’s most recent pricing data.

We’ve been writing a lot about sheet prices, and those for hot-rolled (HR) in particular, coming down. Here's one thing that hasn't dropped: The wide spread between HR and cold-rolled (CR) prices. That's what's in a chart below. And I'm using it as a rough proxy for galv and G'lume base prices as well

SMU’s monthly at-a-glance articles summarize important steel market metrics for the prior month. This May report contains data updated through June 7. Steel prices for sheet and plate products continued to edge lower throughout May. The SMU Price Momentum Indicator was adjusted from neutral to lower at the beginning of the month. We saw a […]

Crude oil prices are forecast to ease slightly through the remainder of the year, while natural gas prices are expected to move higher following recent lows

Domestic scrap prices have fallen in June for all grades tracked by SMU, with prime scrap sinking $30 per gross ton (gt) from May, according to scrap sources.

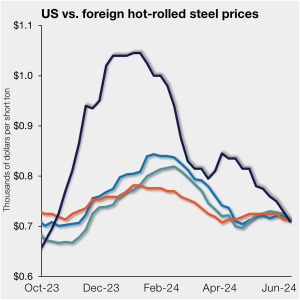

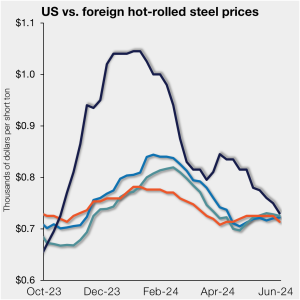

US hot-rolled (HR) coil prices fell further this past week, bringing them even with offshore hot band prices on a landed basis.

Friedman Industries reported lower earnings in its fiscal fourth quarter, and the company expects first-quarter margins to be lower than Q4 margins due to declining HRC prices.

US light-vehicle (LV) sales rose to an unadjusted 1.43 million units in May, up 4.8% vs. year-ago levels, the US Bureau of Economic Analysis (BEA) reported. The year-on-year (y/y) growth in domestic LV sales came in with a 7.6% month-on-month (m/m) boost.

Steel Market Update’s Steel Demand Index moved up 2.5 points last week, though it remains in contraction territory and at one of the lowest readings in nearly a year, according to our latest survey data.

On Monday and Tuesday of this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market events.

US sheet prices continued to tick down this week as supply seems to outweigh demand, and deep discounts are not only for large-ton buys.

Nucor said on Monday that it would lower its weekly hot-rolled (HR) coil price effective immediately. In a letter to customers, the company said its consumer spot price (CSP) for the week of June 10 would be $720 per short ton (st), a $60/st cut vs. the prior week. This is not the first big […]

Where do sheet prices go from here? How is the state of steel demand? And is the dip in prices we've seen just a case of the summer doldrums, or is it something more significant?

Let’s start by asking this: Were the proclamations that Nucor’s published index prices would drift lower with the reality of a bear market for flat rolled ultimately a bit premature with the benefit of hindsight?

Offshore cold-rolled (CR) coil prices remain notably cheaper than domestic product. That remains the case even as US CR coil prices continue to tick lower.

The latest SMU market survey results are now available on our website to all premium members. After logging in at steelmarketupdate.com, visit the pricing and analysis tab and look under the “survey results” section for “latest survey results.” Historical survey results are also available under that selection. If you need help accessing the survey results, or if your company would like to have your voice heard in our future surveys, contact info@steelmarketupdate.com.

Sufficient inventories resulting in softer demand continued to drag down US longs prices this month. Furthermore, lower scrap prices in May added to the downward pressure and expectations for June scrap are turning increasingly bearish. Import interest was also limited, particularly as competition among domestic producers rose.

It feels like the summer doldrums arrived a little earlier than usual this year. I know there had been rumors of a price hike. The prospect of a sharply lower June scrap trade probably didn't help the chances of that actually happening.

SMU’s Steel Buyers’ Sentiment Indices both rebounded sharply this week, according to our most recent survey data.

US hot-rolled (HR) coil prices ticked down again this past week, nearly reaching parity with offshore hot band prices on a landed basis. This week, domestic HR coil tags were $730 per short ton (st) on average based on SMU’s latest check of the market on Tuesday, June 4. Domestic HR coil prices are now […]

Steel buyers found mills more willing to negotiate spot pricing this week on all products SMU tracks with the exception of Galvalume, according to our most recent survey data.

The suspense about the drop in ferrous scrap pricing for June has ended with Delta, Ohio-based North Star BlueScope entering the market at significantly lower numbers than most predicted.