Analysis

April 28, 2024

Final thoughts

Written by Laura Miller & Michael Cowden

What a difference a month makes. In late March, it seemed like the US hot-rolled (HR) coil market was poised to cycle upward.

Large buyers had re-entered the market and placed big orders earlier in the month. Several outages were underway or upcoming. And expectations were that lead times would continue to extend.

Cliffs said on March 27 that it would seek at least $900 per short ton (st) for HR, a $60/st increase. Mills were holding the line on higher prices. And service centers were raising prices in tandem with them.

An abrupt shift happened when Nucor on April 8 announced its first weekly HR price: $830/st, $70/ton below Cliffs’ target. Subsequent published prices from the Charlotte, N.C-based steelmaker were $835/st, only $5/st higher.

Service centers were abruptly raising prices. Mills became more willing to negotiate lower prices. And lead times stagnated along with sheet prices.

Last week, following Nucor, Cliffs rolled out a published HR price – $850/st, or $50/st below where the Cleveland-based steelmaker had been a month earlier. Meanwhile, some of those spring outages are concluding.

The result: Our most recent survey paints a sharply different picture the one in late March. Nearly all respondents think the market has already peaked or soon will. They don’t see much upward momentum coming from May scrap prices. And they’re perhaps less enthusiastic than they initially were about mill-published spot HR prices.

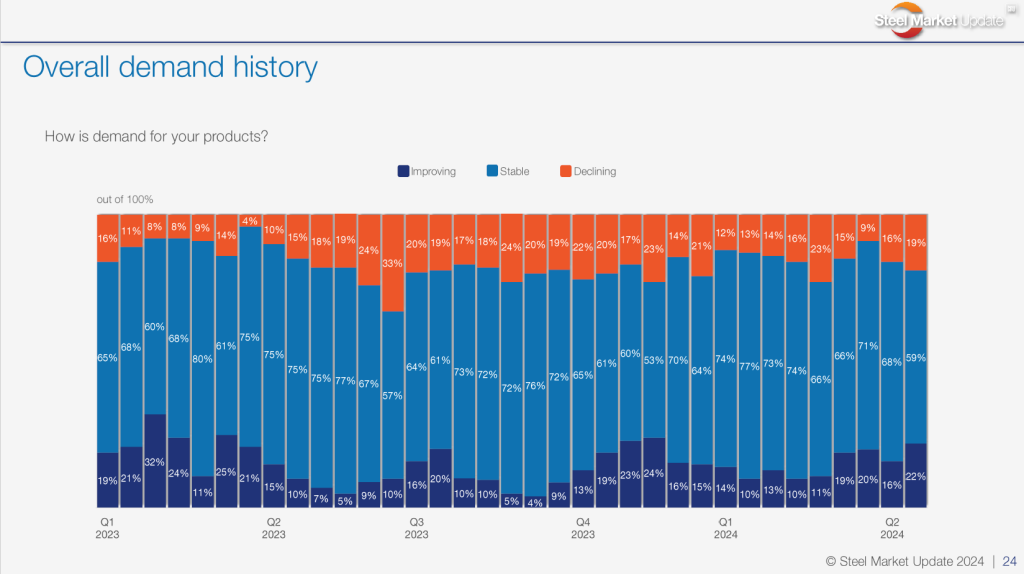

The good news? Roughly 80% of steel buyers we surveyed continue to report stable or improving demand. And that comes despite the upward momentum in sheet prices in late March coming to an abrupt halt in April.

As we look back at April and forward to May, see what our survey respondents have to say in their own words below.

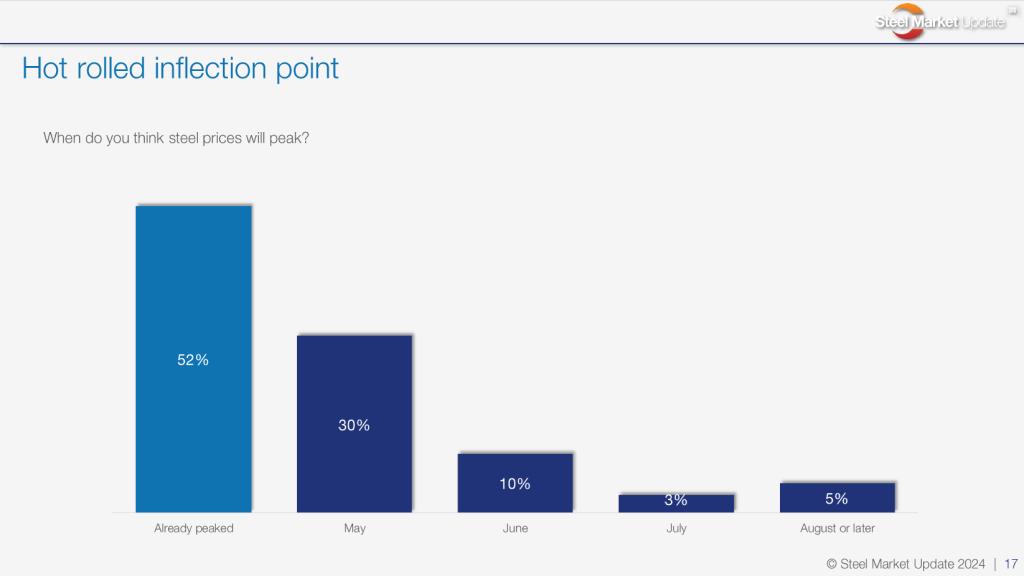

When do you think sheet prices will peak, and why?

Already peaked:

“Demand is not there.”

“Starting to see softening prices.”

“I thought it had more legs, but the Nucor CSP tempered the market.”

“Market is stable.”

“The timing and actual price of Nucor’s new spot HRC price killed any upward momentum. For some reason, market leaders haven’t learned how uncertainty impacts buying behavior.”

“We were bearish on this market even before the Nucor CSP launched, so we remain so.”

“I don’t believe there is enough demand in the market to keep prices elevated.”

“Spring demand will increase and offshore volumes will be reduced short term due to less buying in January.”

May:

“A little life left in the rally. Not much.”

“Maybe a little push from scrap, but that’s it.”

“Seeing more demand from our customers.”

“Time of the year plus some issues with a domestic mill will push the market a little higher into May.”

“Peaking here but probably not for long. Volatility remains. Summer slowdown on the horizon.”

June:

“Supply/demand dynamics are still not in balance. More supply push to come unless Nucor’s CSP continues to flatten price momentum more.”

“Will plateau in about two months at about $880.”

August or later:

“Until Imports slow down or demand picks up, it seems like there may be too much steel in the pipeline.”

“I feel prices will be declining to stable until fall.”

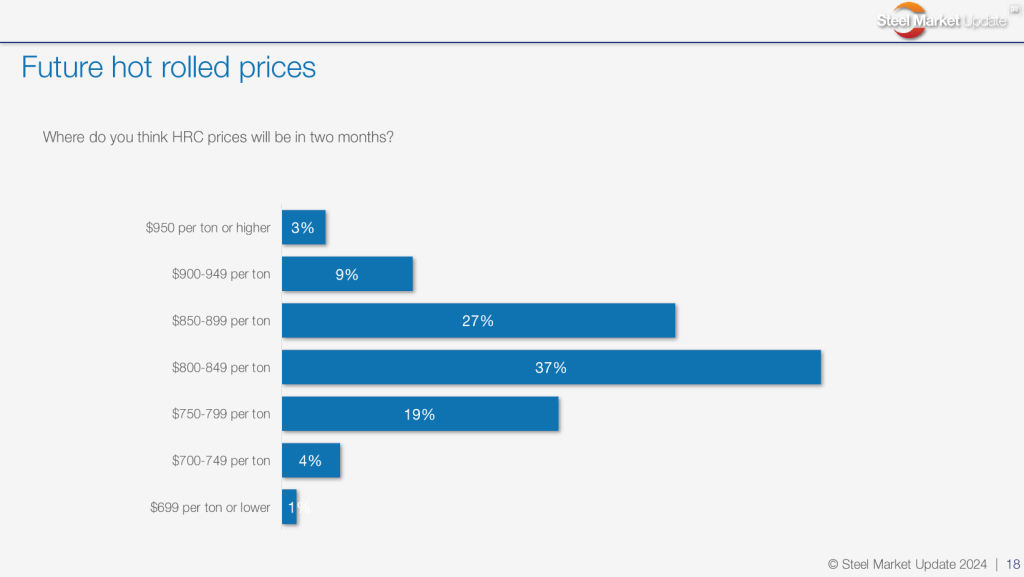

Hot rolled coil prices averaged $845 per short ton in our last market survey. Where will prices be in two months?

$750-799/st:

“Not enough demand to sustain current pricing.”

“Weak order books and tepid demand.”

“It was a tough choice between $750-799 and $700-749. The market seems in balance right now with mill outages happening. Without mill outages and the summer slowdown, I expect some downward pressure from current levels.”

“No reason to think pricing will rebound further. Nucor’s CSP, scrap, imports, summer doldrums — everything is pointing to sub-$800/ton again here soon.”

“Business is soft, more imports coming in.”

$800-849/st;

“Summer slowdown will cool off pricing.”

“Descending or at least leveling to a degree already on hot rolled. Cold rolled and galvanized will stay relatively firm until June.”

“Decent demand, pressure on raw material costs.”

$850-899/st:

“Barring any major disruptions, this appears to be a realistic range.”

“Demand is stronger and lead times are being stretched out.”

$900-949/st:

“We see a trend happening with three steel sources.”

“More momentum is still to come.”

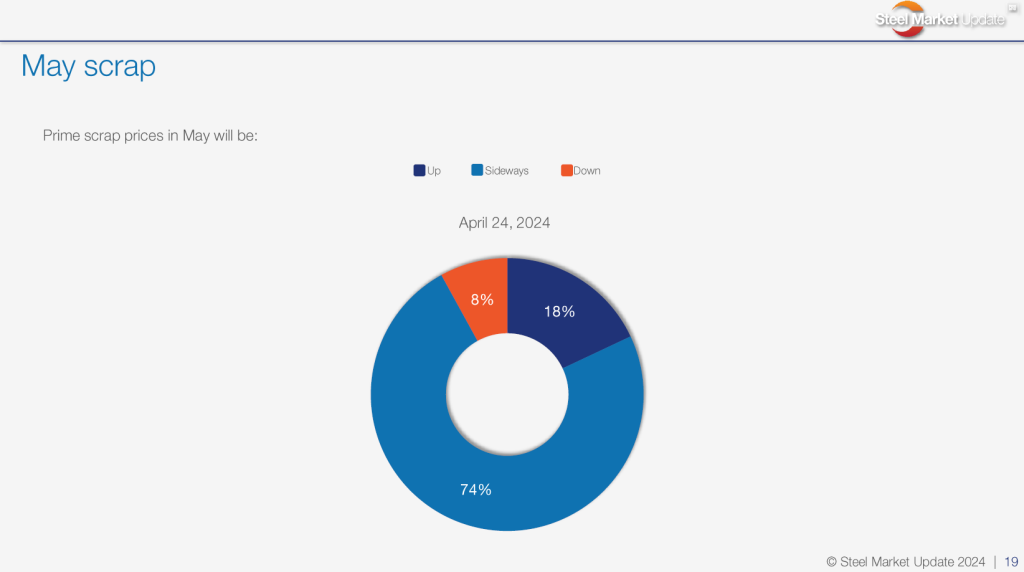

Prime scrap prices in May will be:

Sideways:

“World markets are flattish, and the US seems the same.”

“It seemed like everyone we spoke to last week left ISRI (ReMA) with more questions than answers. ‘Sideways’ seems appropriate for now.”

“Sideways to slightly up in May.”

“Iron ore around $100 and weaker than expected Chinese demand.”

Down:

“Things, in general, just seem slow.”

Up:

“Slightly as flat side capacity returns.”

“Strong sideways; slightly up.”

“While no major moves up, it does appear the markets have room to adjust.”

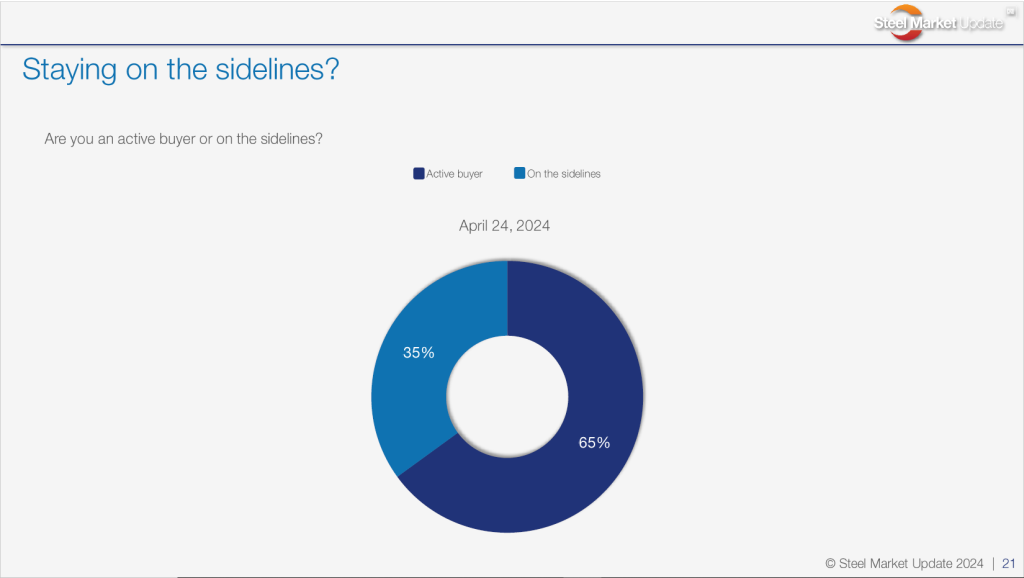

Are you an active buyer or on the sidelines, and why?

Active buyer:

“Looking for import allocations for September arrival.”

“Always buying back-to-back contracts for new orders.”

“Following our demand.”

“Active buyer but at lower levels.”

“Replenishment buying.”

“Climate is still positive.”

“Only to backlog. No extra tons.”

“Pricing is at the bottom and need to secure Q3 demand requirements.”

On the sidelines:

“Not willing to make any commitments…especially for tandem products with longer lead times.”

“Overstocked; also, I don’t believe plate has bottomed yet.”

“We are monitoring steel pricing closely to avoid getting caught with high priced material.”

“We have enough steel.”

“We are working our way through inventory and material that is already on order.”

How is demand for your products?

Declining:

“Spot buying has declined; contract is stable.”

“Import future demand is softer now.”

“March bookings were great. Once Nucor killed HRC momentum our bookings have slid.”

“Ag has taken a hit, with higher interest rates.”

“Soft-stable in H1’24.”

Stable:

“I prefer the term ‘stagnant.’”

Improving:

“Slowly improving every month of 2024 – but still slowly.”

“We are forecasting a strong second half of 2024.”

“Construction start is later than expected.”

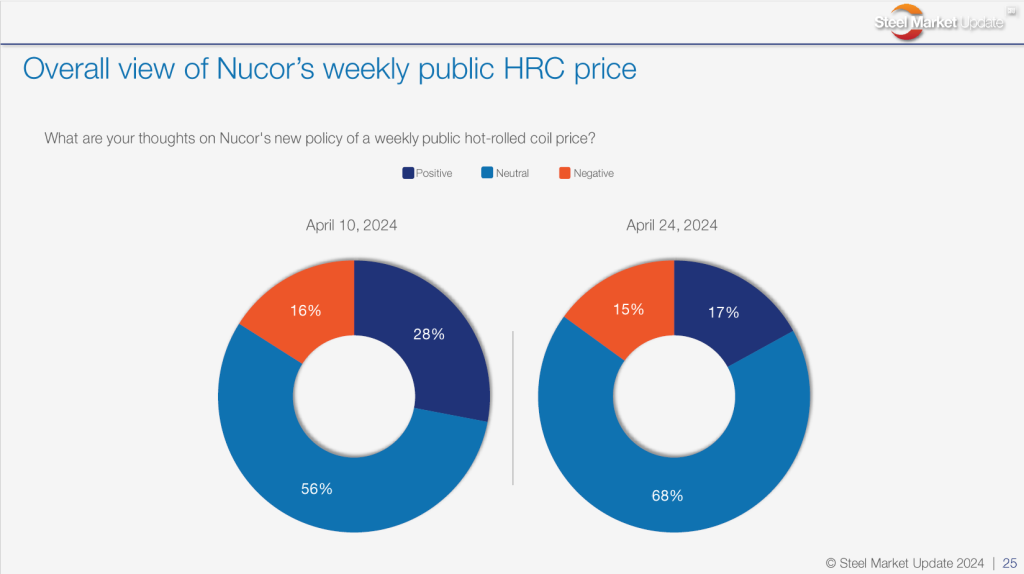

What are your thoughts on Nucor’s new policy of a weekly public HRC price?

Positive:

“I appreciate a relevant price page for HRC similar to what mills have for structural shapes.”

Neutral:

“Still need more time to figure out how the markets/mills will react to this in the long term.”

“I think it is fun to see, but definitely risks putting a cap on the market.”

“The mill can publish a weekly price, but will it hold water in a challenging market? And will the mill be willing to lower their price as the market trends down? Doubtful!”

“It’s interesting – would like to hear Nucor’s comments on why they started now. I understand they do it for long products and this is a natural move.”

“Another voice in the market attempting to set tone and persuade.”

“Wait and see how they manage it. … What other mills do could help or could be more confusing.”

Negative:

“Too much influence on prices in the market.”

“Negative only because it killed the market.”

Now three weeks in, have your thoughts changed on Nucor’s new policy of a weekly public HRC price?

“I like a mill being transparent at their number, but believe it is too low for the overall market.”

“Undecided on how this will work for the long term, definitely interesting.”

“It is positive for the market. However, they don’t have so many spot tons available, so it would be good if another mill (a larger spot player) would publish their pricing.”

“Hopefully, it helps solidify/stabilize the market.”

“Same old things happening with a slightly different package.”

“It is already having a bigger effect than I thought, flattening the market momentum, which is one of their goals. But I didn’t think it would happen this fast.”

“My expectation was that it could potentially hurt any upward momentum in the short term, which was accurate. But then, longer-term, is still wait and see.”

“While Nucor claims this was meant to provide visibility to everyone, it is clear of the underlying reason why they rolled it out.”

“The number published is below the current HRC market and not supported by all Nucor mills.”

“It is a gutsy move, which is fun to see. But it will have a negative impact on index pricing overall.”

“Not sure how impactful it will be. Still, applaud their efforts to have something established. Issue will remain that they will need to establish a discount to their stated weekly spot price.”

“It’s smoke and mirrors.”

Well, there you have it. Nucor’s CSP is still a key topic for chatter within the steel industry. And now Cliffs’ announcement of a monthly spot price should keep us all talking for a while. Grab your popcorn and stay tuned to SMU. It’s an interesting time in the world of HRC! We’ll keep you updated with the latest.

Stay involved with SMU

We have plenty of upcoming opportunities for you to stay active in the SMU community.

Hybar CEO David Stickler will join us for our May 1 Community Chat to talk rebar and more. Then our May 15 Community Chat will feature CRU senior analyst Ryan McKinley where we’ll hear the latest outlook for the flat-rolled steel market.

Nominations are due for the SMU NexGen Leadership Award 2024 by May 24. If you have an impressive emerging leader in your company, nominate them for this prestigious award. The winner will have the opportunity for a mentorship session with a leading industry executive and be recognized on stage at this year’s Steel Summit.

We have an in-person Steel 101 class on June 11-12 in Fort Wayne, Ind. It will include a tour of Steel Dynamics Inc.’s Butler mill – the company’s first steel plant.

Speaking of… the SMU Steel Summit 2024 may still seem a ways out. But August will be here before you know it. Register and book your hotel room early to ensure a spot close to the Georgia International Convention Center. We look forward to seeing you in Atlanta and catching up face-to-face with the greater steel community.

Thank you for your continued interest in and support of SMU!

Laura Miller

Read more from Laura Miller