CRU

April 20, 2024

CRU: Sheet prices stable w/w in most areas of the world

Written by Ryan McKinley

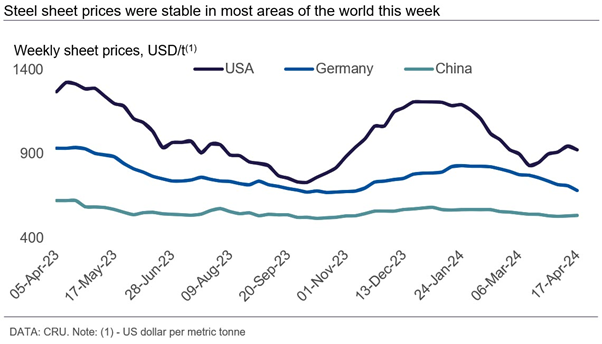

Steel sheet prices in many regions of the world were steady week over week (w/w) in the week ended April 17.

In China, some bullish macroeconomic data prompted increased trading activity and a reduction in inventory levels, although it was not quite enough to lift prices. Trading activity, however, was more subdued in other parts of Asia on persistent demand weakness, and while domestic prices held this week, producers will likely need to cut output in the near term.

US prices were mixed depending on the product, with prices for HR coil falling while downstream product prices rose. Still, recent upward pricing momentum for all products appears to be fading.

The European market was the weakest this past week, with prices falling across the board largely due to competitively priced imports.

USA

US sheet price direction was mixed depending on product in the week ended April 17. HR coil prices were down by $21 per short ton (st) to $839/st, while CR coil and HDG coil (base) prices were up by $29/st and $17/st to $1,184/st and $1,168 st, respectively. The range of price submission for HR coil widened on the low end compared to the prior week, and volumes transacted were somewhat down w/w.

The rise in sheet prices over the last month was reflected in a m/m rise in March service center material on order data collected by Steel Market Update. The increase in orders had allowed sellers to drive up spot prices, although this upward momentum seems to be fading. Indeed, inventory levels combined with material on order suggest that supply overall is not tight. With material set to arrive at service centers over the next month from domestic mills and, in some cases, delayed import arrivals, it is unlikely that prices have much further room to rise as mills return from maintenance outages at the end of April. Market participants report that demand is steady but not strong and that this will also help to keep supply availability in the market elevated.

Europe

European sheet market weakness continued this week, with prices falling by €6–14 (US$6.40-15) w/w across all products. German and Italian spot HR coil were assessed at €644/metric ton and €633/mt, respectively.

Sheet demand in Europe remains subdued, which continues to put downward pressure on prices. However, market participants expect prices to bottom in the near term. Some sellers have said there has been an increase in inquiries and some speculative bids from buyers over the past three weeks as buyers try to time the bottom of the market.

Large stockholders were reportedly also actively fishing for the lowest possible import offers. Vietnamese import offers were heard at €550–560/mt CIF Italy for Q3’24, but few deals were confirmed. This is because a lot of material has already been booked from Vietnam and there is a high chance that Vietnam will have a dedicated quota starting from Q3.

The EU safeguard quota for HR coil imports from other countries has been exhausted again in Q2, surpassing the allocated 923,594 mt within days of opening on April 1. As of April 12, the excess amounted to 4,742 mt, or around 1%. According to market participants, buyers could pay between 2–3% of additional duty to clear this material.

Meanwhile, ThyssenKrupp announced its plans to restructure its steel operations in Duisburg. The company aims to align its production capacities with the current demand level in the market. While jobs cuts are expected, the company intends to avoid redundancies driven entirely by operational needs.

China

Chinese domestic sheet prices remained stable w/w. Better-than-expected March macroeconomic data released during the week brought bullish sentiment to the market and improved steel trading activity, resulting in a w/w fall in sheet inventory and some limited recovery in steel mill profitability. However, there was not much reaction from end-use sectors, with buyers still limiting buys to only what they need immediately.

Meanwhile, steel mills are still not confident about an immediate pick-up in exports after Ramadan ended last week. In addition, price increase announcements in key destination markets in Southeast Asia were not widely accepted as buyers in those countries remain cautious.

Asia

Prices of imported sheet products in Asia were stable this week amid limited purchasing interest as buyers remained cautious.

Following a price increase in the Chinese domestic market, some Chinese exporters tried to raise offers by $5-10/mt for HR coil SAE1006 grade to ~$560-565/mt CFR Vietnam, but this was not well received by buyers. According to some market contacts, these offers would have had to have been $550/mt CFR Vietnam to generate interest.

Formosa Ha Tinh recently announced its HR coil offers for June shipments to customers in Vietnam. The mill kept offers unchanged in VND currency terms, but because of the appreciation of the US dollar, the new offers are ~$5/mt lower from the previous month at $575-591/mt CFR Vietnam, depending on volume.

CRU assessed HR coil at $550/mt CFR Far East, flat w/w. CR coil and HDG coil prices were also unchanged w/w at $680/mt and $700/mt, respectively.

India

Indian domestic sheet prices were unchanged w/w despite a $10/mt drop in HR coil export prices to $560/mt FOB. Market activity is low because purchases are being made on an as-needed basis due to low lead times offered by mills and distributors. Steelmakers announced a INR500–1000/mt (US$6–12) increase in sheet prices for April output, but it was not absorbed by the market. March inventory is being sold at a discount in the spot market, while dealers are reluctant to procure more stock from mills amid weak market conditions and working capital woes.

Indian steelmakers continue to respond to slow domestic buying by offering more volumes to the export market at a competitive price. However, prices from other Asian suppliers have dropped at a sharper pace, lowering the attractiveness of export sales for Indian mills. CRU understands from market sources that unless Asian prices recover in the coming month, several Indian mills are planning to curtail sheet output starting in May.

Learn more about CRU’s services at www.crugroup.com.