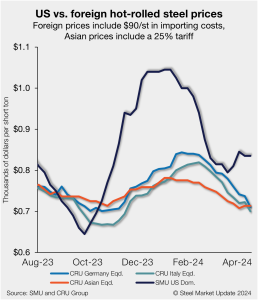

Final thoughts

I’ve gotten some questions lately about whether the huge gap between domestic hot-rolled coil (HR) prices and those for cold-rolled (CR) and coated is sustainable. I remember being asked similar questions about the wide spread between HR and plate that developed in early 2022. I thought at the time that there was no way that spread could hold. Turned out, I was wrong. That was humbling. And so I’m not going to make any bold predictions this time.