Analysis

March 17, 2024

Final thoughts

Written by Laura Miller

Are we still looking for a bottom on sheet prices? In what direction are steel and scrap prices headed? How’s demand holding up at the moment?

Steel buyers shared their thoughts on these questions and more in SMU’s March 11-13 flat rolled market trends survey.

In your own words, with minimal editing, here’s what some of you in the SMU community shared with us this past week. We’ve also included some of the slides from our steel buyers’ survey.

These slides and comments only touch on a portion of the information you share with us in our weekly surveys. The survey results are available to Premium subscribers and data providers. If you’re interested in upgrading to a Premium subscription, reach out to luis.corona@crugroup.com for more information. To participate in the survey and become a data provider, you can contact david@steelmarketupdate.com.

Thank you to everyone who participates in our surveys, chats with us each week, and is an active member of the SMU community!

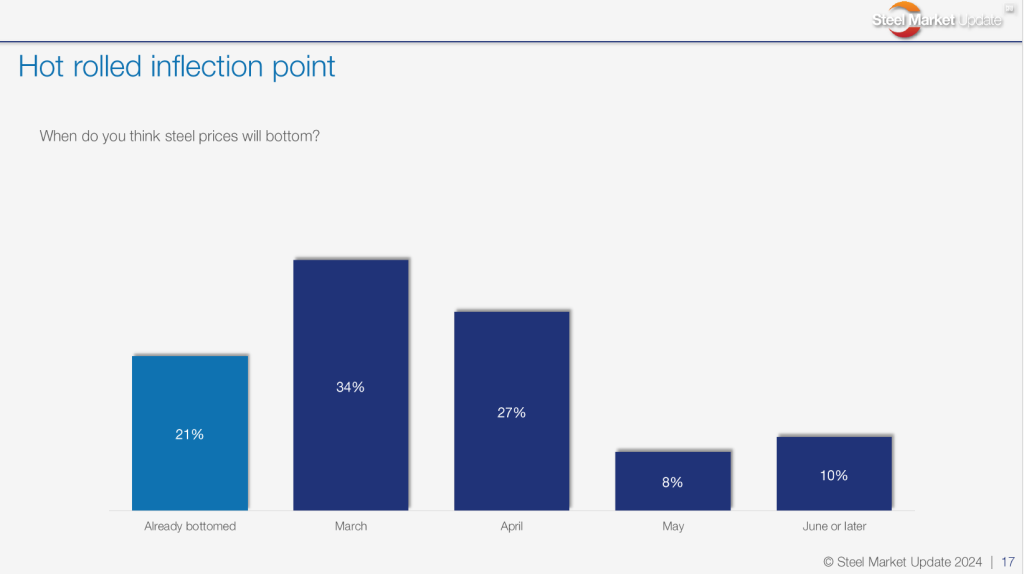

When do you think sheet prices will bottom, and why?

Already bottomed:

“HR futures moved massively ahead of the published mill increases.”

“Difficult question at this point. Mills will fight further softening, but can they fight the market? We’re in a period of increased activity as some customers feel we have hit a bottom.”

“For now but feel there will be another downturn for the summer slowdown.”

March:

“Inventories need to be replenished and buyers are realizing Q2 will see supply weakened by mill maintenance outages and fewer imports arriving in May and June.”

“Close to a temporary bottom for now, at least for HRC. Inventories are on the lower side and people need to buy so mills will get orders and lead times move out. Watch to see if any larger tubers make spot speculation buys or not. This might signal a floor.”

“April domestic mill outages.”

“Prices already rising.”

April:

“Demand is still correcting.”

“Still some room to move.”

“These latest increases will only ‘pause’ the market dip; not enough demand to stop them from getting down to $680/ton.”

“Scrap is lower, plenty of imports, service center inventory okay, mills’ lead times are short.”

“We are factoring a bottom in late March or early April. We don’t believe the recent hikes will really stop the slide.”

“Construction will pick up, and automotive will increase.”

May:

“Low demand leading into automotive model year changeovers.”

“Imports are coming in April and May.”

June or later:

“Uncertain demand.”

“Dead cat bounce.”

Hot-rolled coil prices averaged $815 per short ton (st) in our last market survey. Where will prices be in two months?

$900-949/st:

“Demand will be higher, supply will be lower, and mills will have momentum (and then take pricing too high again).”

$850-899/st:

“High end likely around $880-910 per ton.”

“After bottoming out, they will increase.”

$800-849/st:

“With some of the planned outages and better automotive numbers, we could get a contained bounce before summer. That would take HR a notch higher.”

“Prices will begin to climb back up through April/May, peak in June before another decline.”

“Mills trying to stop the bleeding but don’t see a run.”

“I think the rise and then fall again for the summer slowdown.”

“With the recent announcements, I think we are close to the bottom.”

$750-799/st:

“Buyers have revenge in mind.”

“Demand is softening, service centers have restocked, and mills are begging for spot orders.”

“Pricing should bottom in early Q2, but I don’t think it’ll spike up anytime soon.”

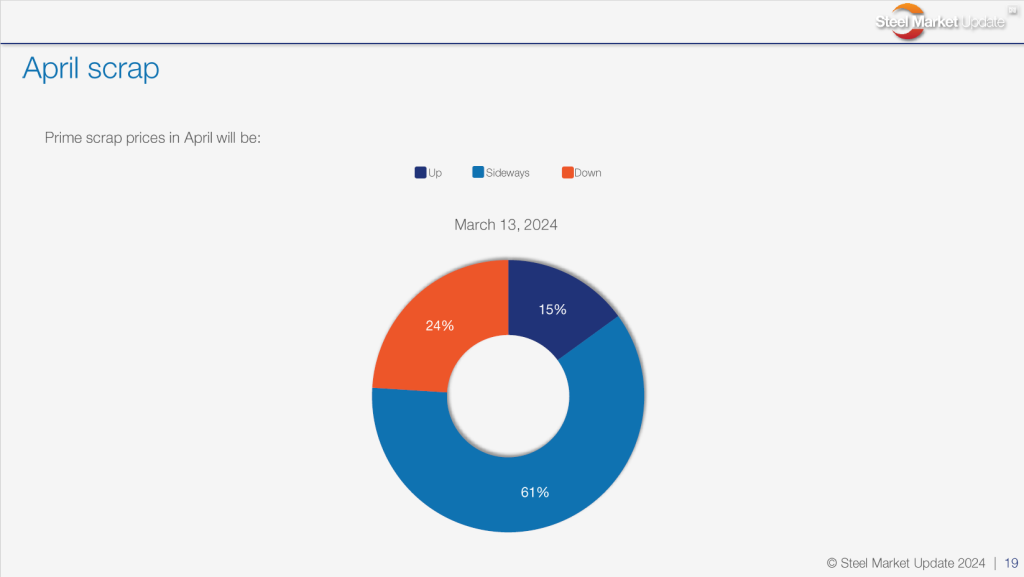

Prime scrap prices in April will be:

Down:

“Down another $20 with idling inevitable.”

“Short-term trend is down.”

“Following the HRC market.”

Sideways:

“We’ll say the usual ‘soft sideways’ here, but I don’t think there is a ton of clarity out there right now.”

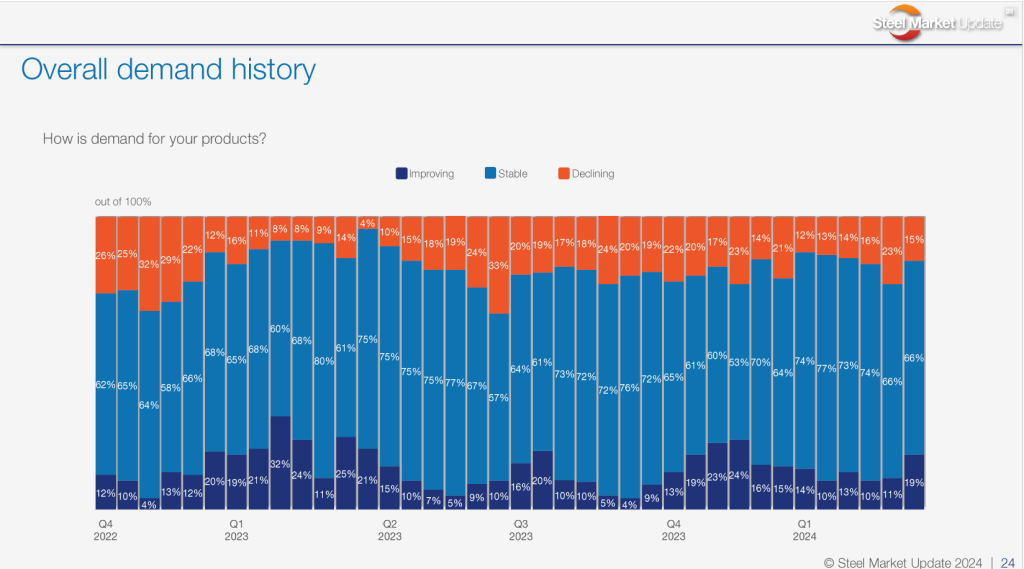

How is demand for your products?

Declining:

“Caution from our customers.”

“Demand for coated is softer.”

Stable:

“Demand hasn’t changed much, just price fluctuations in the sell price.”

Improving:

“Spot has become active vs. nothing the previous two months.”

“Could be very short term.”

“Power grid and electric vehicle charging infrastructure growth is continuing.”

“Strong automotive is overcoming shortcomings.”

Upcoming SMU Community Chat

We’ll touch on some of these topics and much more in our next Community Chat with Barry Zekelman, CEO of Zekelman Industries, one of the largest steel buyers in North America, on March 20. Don’t miss the conversation; you can register here.

As always, thank you for your continued support of SMU!