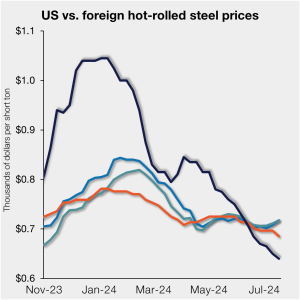

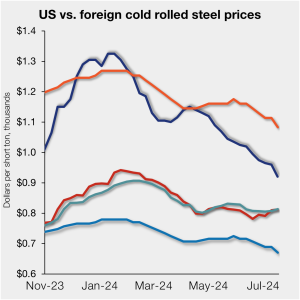

Imported CR still cheaper despite lower US prices

The price gap between US cold-rolled (CR) coil and imported CR has fallen to a 10-month low as domestic tags continue to drift lower. Domestic CR coil prices averaged $920 per short ton (st) in our check of the market on Tuesday, July 16, down $40/st from the week before. CR tags are now down […]