Louisiana procures land for Hyundai's EAF facility

The state of Louisiana has purchased 1,700 acres along the Mississippi River from Germania Plantation Inc. for $91 million for Hyundai Steel's proposed EAF operation.

The state of Louisiana has purchased 1,700 acres along the Mississippi River from Germania Plantation Inc. for $91 million for Hyundai Steel's proposed EAF operation.

Steel sheet and plate prices rose across the board to start the year on limited spot availability at some mills, expectations of higher scrap prices, and hopes of stronger demand in 2026.

Kloeckner Metals Corp. announced that beginning Jan. 1, 2026, the former Bauer Built Manufacturing site in Paton, Iowa, would lead all its commercial, manufacturing, and other operational activities.

Majestic Steel USA announced that Chad Broyles will now be the Executive Vice President for its business operations unit. The Cleveland-headquartered flat-rolled steel distributor and processor expects Broyles to help Majestic align its commercial and operational priorities. As EVP, Broyles will oversee service center operations, according to the company’s Jan. 5 statement. Todd Leebow, president and CEO of Majestic Steel USA, noted that since joining Majestic in 2025 Broyles’ has been a valuable contributor to its […]

Demand for heavy steel plate used in offshore wind farms faces renewed uncertainty after President Trump paused leases for five offshore wind projects.

Members of the United Steelworkers (USW) Local 1123 labor union voted against ratifying a second proposed deal with Metallus on Dec. 18.

Nucor Plate Group notified customers it was aiming to increase all plate product prices by $40 per short ton (st).

An SMU Community Chat with Timna Tanners.

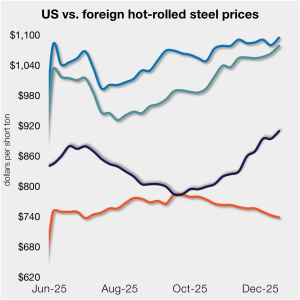

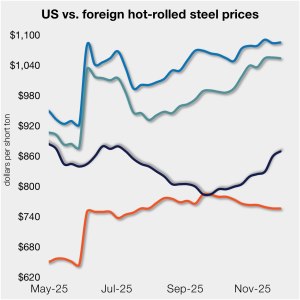

The price gap between stateside hot band and landed offshore product continues to narrow, inching closer toward parity. The premium is now, on average, at its lowest level since July.

SMU and AMU are pleased to announce that Wells Fargo Managing Director Timna Tanners will be joining us for a Community Chat webinar on Wednesday, Dec. 17, at 11 am ET.

Metalforming manufacturers were mixed in their outlook, anticipating business conditions could either worsen or, at best, hold in the near-term, according to PMA's November report.

The price gap between stateside hot band and landed offshore product tightened further this week, as the average price for domestic hot-rolled was $10/st higher w/w.

German Economy Minister Katherina Reiche expressed frustration with US levies on steel and aluminum products. The US contends the EU is unfairly targeting its big tech firms.

The downward trend in Chinese steel export prices continued over the past month, as domestic demand in the country failed to recover following the Golden Week holidays.

Edward Meir will be the featured speaker on an AMU and SMU Community Chat on Thursday, Nov. 20, at 11 am ET to discuss the latest market developments and to share his unique insights.

JSW Steel USA aims to increase steel plate prices by at least $40/short ton.

ArcelorMittal Dofasco and Stelco joined recent moves by US mills to push sheet prices higher.

U.S. Steel has unveiled more details of a multi-year growth plan in partnership with Nippon Steel.

The new Steel Market Update website is officially live.

The Steel Market Update website will be temporarily unavailable on Monday, Nov. 3, from approximately 4:00–8:00 a.m. Eastern Time.

The revamped Steel Market Update website goes live on Monday, Nov. 3, 2025.

Ternium closed the third quarter with steady shipments and improving margins. But trade policy uncertainty and subdued demand in Mexico weighed on the Latin American steelmaker’s results.

Cleveland-Cliffs on Thursday said it had signed a memorandum of understanding (MoU) with POSCO to forge a strategic partnership, one Cliffs bills as "transformative."

India's JSW Steel reported a 307% year-on-year (y/y) jump in net profit to INR16.5 bn ($188 million, €161 million) in fiscal Q2.

Our average HR coil price increased $5/short ton from last week, marking a second consecutive week of modest gains. Market participants generally attributed the increase to...

Cleveland-Cliffs executives pointed to growing automotive demand as the engine driving a turnaround at the company.

US domestic sheet prices have remained rangebound in recent weeks as supply tightness met weak demand. Demand for steel produced in the US increased among some Mexican industrial buyers....

The Department of Commerce received 97 submissions from producers, manufacturers, and groups seeking Section 232 tariff coverage for steel and aluminum derivative products.

As it accelerates an ambitious push to reshore American bicycle manufacturing, Guardian Bikes is seeking special tariff consideration for the bicycle industry.

The World Steel Association (worldsteel) Short Range Outlook for global steel demand predicts that 2025’s steel demand will clock in at the same level as in 2024. In its October report, the Brussels-based association stated that this year’s steel demand will reach ~1,750 million metric tons (mt). The organization forecasts a 1.3% demand rebound in 2026, pushing […]