Product

March 8, 2013

Scrap, Iron Ore & Billets Futures Update

Written by Bradley Clark

Written by: Bradley Clark, Director of Steel Trading, Kataman Metals

U.S. Midwest #1 Busheling Ferrous Scrap (AMM) Firm on Weather Concerns

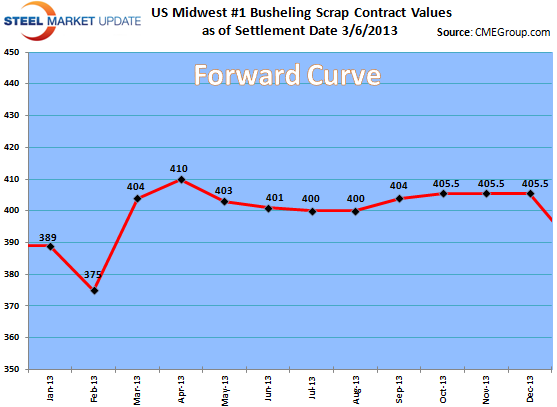

As the beginning of the month progresses the physical scrap market has begun to price higher lending impetus to the futures market to begin trading. After months of stagnant and softer busheling markets, March is shaping up to be up $30-40 per ton. A few buyers jumped in early and paid up $40 in the upper Midwest while other in the South seem to have taken a more wait and see approach and are buying closer to up $30. These increases are mainly attributed to weather related slowing of supply rather than robust demand from mills whose order books remain anemic.

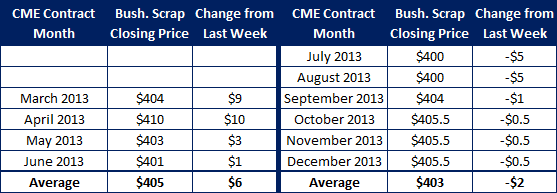

The physical market pricing has spurred a rash of trades on the busheling futures market as offers on March and April periods were lifted on CME’s Globex screen earlier this week at $399, $404 for March and $410 for April all for 100 tons. These levels represent a jump in futures prices of around $10 per ton. The futures market is starting to mirror the physical market in terms of trading days with quiet middle and end of months followed by a flurry of activity at the beginning of the month when information starts to flow from the underlying markets.

CME Busheling Closing Prices as of 3/7/2013 close:

OPEN INTEREST: 220 lots (1 lot = 20 gross tons)

CME Black Sea Billet / TSI Turkish Scrap Prices Tick up Slightly on Low Volumes

After a couple of cargos were booked into Turkey last week up about $10 from last month the market for Turkish scrap and Black Sea Billet has gone quiet. The strengthening of the dollar, weather related problems collecting scrap in the US and a continued softening European steel sector have contributed to this dearth of activity.

The futures market for each contract have experienced no trading the past week as it seems many market participants are uninspired by these low volatility and sluggish nature of the underlying physical markets.

Forward curve TSI Turkish Scrap as of 3/7/2103 close:

March – $403

Q2 – $390

Cal 14 – $390

Forward curve CME Black Sea Billet as of 3/7/2013 close:

March – $535

Q2 – $533

Cal 14 – $530

TSI Iron Ore Prices Plummet as Rebar Prices Collapse

The iron ore market in Asia is continuing to look weak as an abundance of steel inventory is available and growth concerns in China’s property sector are starting to resurface. Others note however that ore stocks are looking historically low, overall the picture is muddled. Though the case could be made for both the bulls and the bears now it does feel like the majority of market participants are expecting the downward trend to continue albeit with some minor rallies on the way down. The story in China as ever is difficult to read with some pundits predicting the boom years over while others continue to beat the drum and chant ‘don’t bet against China’ mantra. Iron ore remains one of the most sensitive commodities to movements from Beijing thus making it a good proxy for those with a view on Chinese economic policy.

The futures market continues to price in this decline as the forward curve remains backwardated through 2015. Volumes on SGX remain robust with millions of tons trading weekly.

TSI Iron ore forward curve as of 3/7/2013:

March – $145

Q2 – $133

Q3 – $126

Cal 14 – $114