Prices

September 4, 2013

August Raw Steel Production & Capacity Utilization Rates

Written by Brett Linton

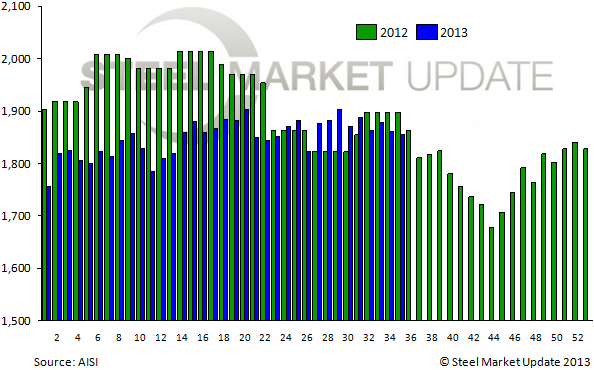

The American Iron & Steel Institute (AISI) reported estimated raw steel production at 1,871,000 net tons for the week ending July 27, 2013. With outages and maintenance issues, production declined through August to a high of 1,888,000 net tons of raw steel in the week ending August 3, and dropping down to 1,856,000 net tons in the final week of the month, ending on August 31.

Capacity utilization declined from 78.8 percent at the beginning of August to 77.5 percent in the week ending August 31.

Capacity utilization declined from 78.8 percent at the beginning of August to 77.5 percent in the week ending August 31.

Year to date production at the beginning of August was at 57,252,000 net tons, down 4.7 percent from the same period in 2012. As of the week ending August 31, YTD production was at 64,709,000 net tons, down 4.3 from the same period in 2012. Average capacity utilization for the year so far is estimated at 77.2 percent down from 77.8 percent YTD 2012. (Note: last year’s comparison includes now defunct RG steel tonnage capacity in the mix, skewing results.)