Prices

December 8, 2013

Flat Rolled Steel Contract Negotiations – The Difference a Month Makes

Written by John Packard

One month ago the domestic steel mills and their manufacturing and service center contract customers were locked in a battle over where pricing would be beginning in January 2014 with many mills firming opposed to the negotiated CRU minus and buckets deal made common over the past couple of years.

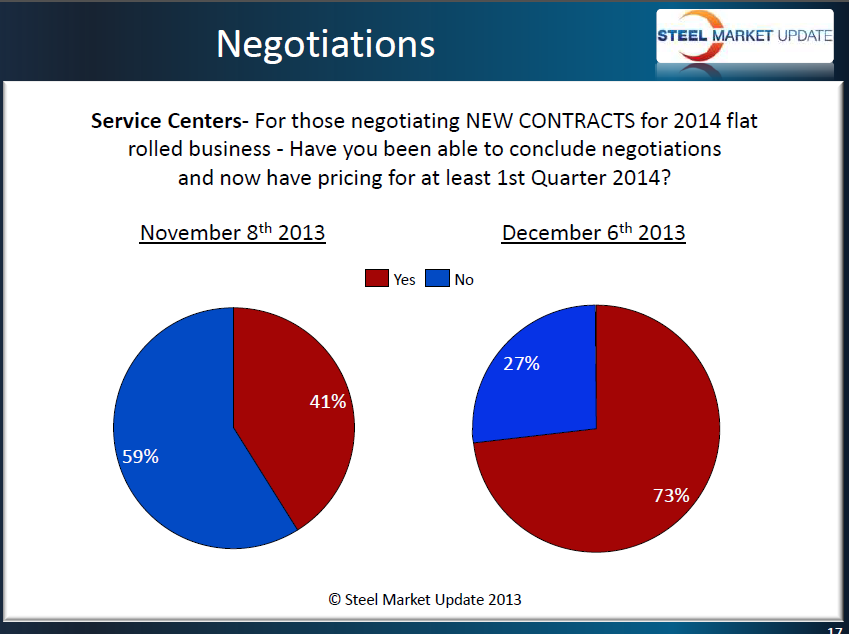

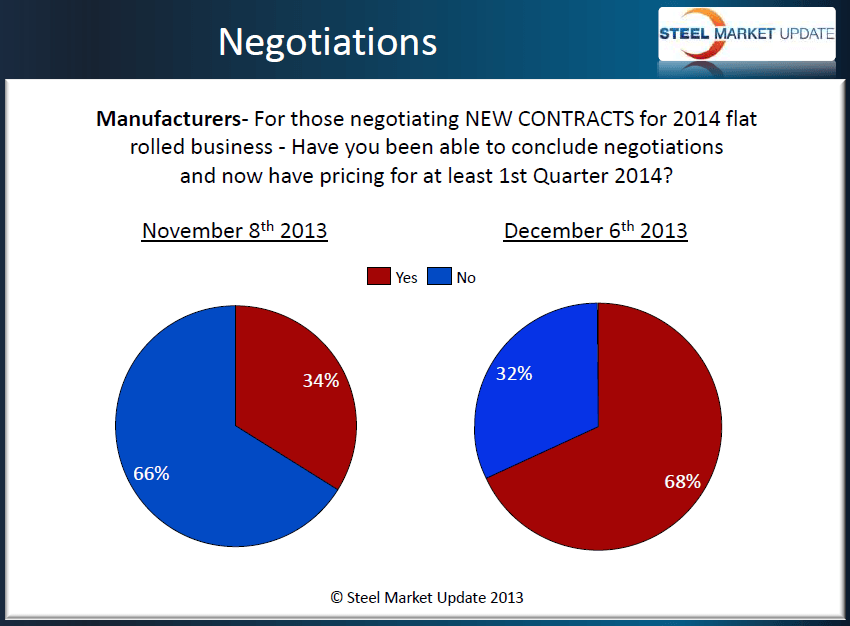

When we polled our respondents in our flat rolled steel market analysis at the beginning of November we found both segments of the industry struggling to get their deals done for 2014. As you can see from the graphics shown as part of this report, 59 percent of the service centers and 66 percent of the manufacturers had not come to conclusion on their contracts in early November. By the time we got to the first week of December our analysis found a total reversal with 73 percent of distributors and 66 percent of manufacturing companies reporting their 2014 contracts as being done.

When we polled our respondents in our flat rolled steel market analysis at the beginning of November we found both segments of the industry struggling to get their deals done for 2014. As you can see from the graphics shown as part of this report, 59 percent of the service centers and 66 percent of the manufacturers had not come to conclusion on their contracts in early November. By the time we got to the first week of December our analysis found a total reversal with 73 percent of distributors and 66 percent of manufacturing companies reporting their 2014 contracts as being done.

We asked the two groups, during both November and December polling, if those who had been unable to conclude negotiations would take their tonnage into the spot markets. The vast majority of both market segments reported yes they would, with 73 percent of manufacturers and 72 percent of service centers responding that way. Both groups increased their odds of moving tonnage into the spot market by approximately ten percent compared to where they were at the beginning of November to now.

The percentage of companies considering using foreign steel to replace a portion of their domestic contract tonnage during the 1st Half 2014 was over 50 percent for both service centers (54 percent) and end users (60 percent).

The percentage of companies considering using foreign steel to replace a portion of their domestic contract tonnage during the 1st Half 2014 was over 50 percent for both service centers (54 percent) and end users (60 percent).

The vast majority of companies appear to have accepted the fact they will be paying more for their steel during 2014. Sixty nine percent of manufacturing companies are resigned to paying more for their steel. Service centers when asked about their end user customers willingness to accept higher prices on their 2014 contracts found 20 percent as reporting their customers as accepting, 29 percent resisting and 51 percent reported it was a mixed bag (some accepting some not).

It will be interesting to see how the extra tons which at one time were locked up in contract will impact the flat rolled steel spot markets and spot pricing.