Prices

July 27, 2014

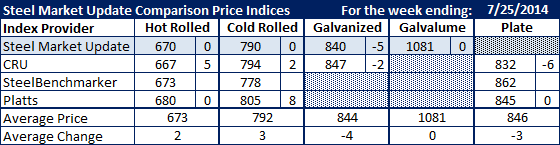

Comparison Price Indices: Ripples

Written by John Packard

Flat rolled steel prices have been essentially trending sideways for the past couple of weeks and this past week was no exception. We saw our hot rolled average increase by $3 per ton to $673 per ton with the CRU having the lowest HRC pricing at $667 per ton and Platts the highest at $680 per ton. CRU was the only index to move hot rolled prices this past week (+$5).

Cold rolled prices also moved up by $2 per ton ($1.75 per ton actually) as Platts moved up to $805 per ton and CRU moved up $2 per ton to $794 per ton.

Galvanized prices moved lower this past week by $4 per ton while Galvalume remained unchanged.

Our plate price average dropped by $6 per ton as CRU moved to $832 and the other indexes remained the same.

Note: SteelBenchmarker did not report new prices this past week. SteelBenchmarker releases prices twice per month.

FOB Points for each index:

SMU: Domestic Mill, East of the Rockies.

CRU: Midwest Mill, East of the Rockies.

SteelBenchmarker: Domestic Mill, East of the Mississippi.

Platts: Northern Indiana Domestic Mill.