Prices

August 24, 2014

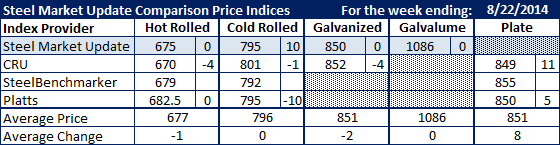

Comparison Price Indices: Sideways to Slipping Lower

Written by John Packard

The spreads between the various steel price indexes watched on a weekly basis by Steel Market Update have been shrinking. With the exception of plate (which had price increase announcements during the week) and SMU cold rolled, all of the other flat rolled steel price indices either moved sideways or moved lower this past week.

Our average on hot rolled dropped by $2 per ton to $677 per ton. The spread from low to high is now $12.50 per ton with CRU being at the low end and Platts at the upper end of the range.

Cold rolled average actually increased as Steel Market Update moved our CR index to $795 per ton (up $10 per ton). The spread between the low set by SteelBenchmarker (who did not produce new numbers this week) and the high by Platts is now $13 per ton. Taking SteelBenchmarker out of the equation the spread is only $10 per ton.

Galvanized average dropped to $851 per ton for .060” G90. We will make our adjustment for the changing extras by early next week as we believe most of the laggards will announce their extras this week for October production.

Galvalume was unchanged and plate price average moved up to $851 per ton (+$12 per ton).

FOB Points for each index:

SMU: Domestic Mill, East of the Rockies.

CRU: Midwest Mill, East of the Rockies.

SteelBenchmarker: Domestic Mill, East of the Mississippi.

Platts: Northern Indiana Domestic Mill.